CGST Circular 179/2022

| Title | Clarification regarding GST rates & classification (goods) based on the recommendations of the GST Council in its 47th meeting held on 28th – 29th June, 2022 at Chandigarh |

| Number | 179/2022 |

| Date | 03-08-2022 |

| Download |

Based on the recommendations of the GST Council in its 47th meeting held on 28th-29th June at Chandigarh, clarifications, with reference to GST levy, related to the following are being issued through this circular:

2.Electric vehicles whether or not fitted with a battery pack, attract GST rate of 5%:

2.1. Representations have been received seeking clarification regarding the applicable rate of GST on electrically operated vehicle without any battery fitted to it.

2.2. The explanation of ‘Electrically operated vehicles’ in entry 242A of Schedule I of notification No. 1/2017-Central Tax (Rate) reads as: ‘Electrically operated vehicles which run solely on electrical energy derived from an external source or from one or more electrical batteries fitted to such road vehicles and shall include E-bicycles.’

2.3. As is evident from the explanation above, electrically operated vehicle including three wheeled electric vehicle means vehicle that runs solely on electrical energy derived from an external source or from electrical batteries. Therefore, the fitting of batteries cannot be considered as a concomitant factor for defining a vehicle as an electrically operated electric vehicle.

2.4. It is also pertinent to state that the WCO’s HSN Explanatory notes have also not considered batteries to be a component, whose absence changes the essential character of an incomplete, unfinished or unassembled vehicle.

2.5. Also, the HSN explanatory notes for Chapter 87 have clearly stated that Motor Chassis fitted with cabs i.e. the chassis fitted with cabin body falls under 87.02 to 87.04 and not in heading 87.06.

5.1. Representations have been received seeking clarification regarding the applicable GST rate on treated sewage water. Treated sewage water was not meant to be construed as falling under “purified” water for the purpose of levy of GST.

5.2. In general, Water, falling under heading 2201, with certain specified exclusions, is exempt from GST vide entry at S. No. 99 of notification No. 2/2017-Central Tax (Rate), dated the 28th June, 2017.

5.3. Accordingly, it is hereby clarified that supply of treated sewage water, falling under heading 2201, is exempt under GST. Further, to clarify the issue, the word ‘purified’ is being omitted from the above-mentioned entry vide notification No. 7/2022-Central Tax (Rate), dated the 13th July, 2022.

6.Nicotine Polacrilex Gum attracts a GST rate of 18%:

6.1. Representations have been received seeking clarification regarding the classification and applicable GST rate on Nicotine Polacrilex gum.

6.2. The WCO 2022 HS Codes has inter alia introduced a new entry 2404 91 00 comprising of products for oral application containing nicotine and intended to assist tobacco use cessation with effect from 01.01.2022. Accordingly, a technical change, without any consequential rate change, has been made vide notification No. 18/2021 – Central Tax (Rate), dated the 28th December, 2021, wherein S. No. 26B in Schedule III of notification no. 1/2017-Central Tax (Rate), dated the 28th June, 2017, has been inserted to include products for oral application containing nicotine and intended to assist in cessation of use of tobacco, and falling under tariff item 2404 91 00. The same is supplemented by the HS Explanatory notes 2022 which states that heading 2404 includes nicotine containing products for recreational use, as well as nicotine replacement therapy (NRT) products intended to assist tobacco use cessation, which are taken as part of a nicotine intake reduction programme in order to lessen the human body’s dependence on this substance.

6.3. Accordingly, it is hereby clarified that the Nicotine Polacrilex gum which is commonly applied orally and is intended to assist tobacco use cessation is appropriately classifiable under tariff item 2404 91 00 with applicable GST rate of 18% [Sl. No. 26B in Schedule III of notification no. 1/2017-Central Tax (Rate), dated the 28th June, 2017].

7. Fly ash bricks and aggregate – condition of 90% fly ash content applied only to fly ash aggregate, and not fly ash bricks:

7.1. Representations have been received seeking clarification regarding the applicable rate on the fly ash bricks and fly ash aggregates.

7.2. Hitherto, as per entry at S. No. 176B of the Schedule II the items of description “Fly ash bricks or fly ash aggregate with 90 per cent. or more fly ash content; Fly ash blocks” attracts a GST rate of 12%. Confusion has arisen about the applicability of 90 per cent. condition on fly ash aggregates and fly ash bricks. As per the recommendations of the GST Council in the 23rd Meeting, the condition of 90% or more fly ash content was applicable only for fly ash aggregate.

7.3. Therefore, it is clarified that the condition of 90 per cent. or more fly ash content applied only to Fly Ash Aggregates and not to fly ash bricks and fly ash blocks. Further, with effect from 18th July, 2022 the condition is omitted from the description.

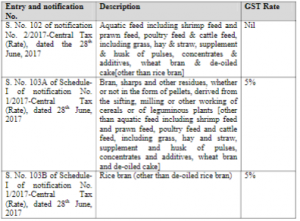

8.4. The dispute in applicable GST rate revolves around the central argument as to whether the above-mentioned by-products are meant for direct consumption as cattle feed and therefore attract exemption under S. No. 102 of notification No. 2/2017-Central Tax (Rate) dated 28th June, 2017 or are otherwise not meant for direct consumption and thus covered under S. No. 103A of notification No. 1/2017- Central Tax (Rate) dated 28thJune, 2017 attracting a GST rate of 5%.

8.5. While milling of pulses/ dal, a wide range of by-products such as chilka, khanda, churi, among others, are obtained which are preferred as cattle feed by dairy industry for better palatability and higher nutritive value. The mentioned by-products are required to go