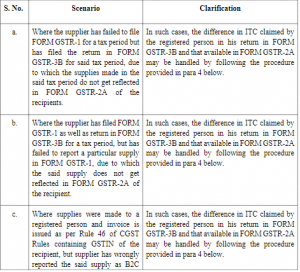

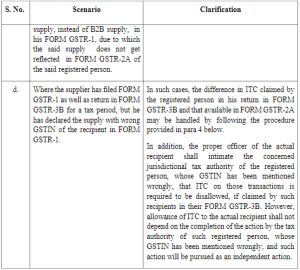

Section 16 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “CGST Act”) provides for eligibility and conditions for availing Input Tax Credit (ITC). During the initial period of implementation of GST, during the financial years 2017-18 and 2018-19, in many cases, the suppliers have failed to furnish the correct details of outward supplies in their FORM GSTR-1, which has led to certain deficiencies or discrepancies in FORM GSTR-2A of their recipients. However, the concerned recipients may have availed input tax credit on the said supplies in their returns in FORM GSTR-3B. The discrepancies between the amount of ITC availed by the registered persons in their returns in FORM GSTR-3B and the amount as available in their FORM GSTR-2A are being noticed by the tax officers during proceedings such as scrutiny/ audit/ investigation etc. due to such credit not flowing to FORM GSTR-2A of the said registered persons. Such discrepancies are considered by the tax officers as representing ineligible ITC availed by the registered persons, and are being flagged seeking explanation from the registered persons for such discrepancies and/or for reversal of such ineligible ITC.

2. It is mentioned that FORM GSTR-2A could not be made available to the taxpayers on the common portal during the initial stages of implementation of GST. Further, restrictions regarding availment of ITC by the registered persons up to certain specified limit beyond the

ITC available as per FORM GSTR-2A were provided under rule 36(4) of Central Goods and Services Tax Rules, 2017 (hereinafter referred to as “CGST Rules”)only with effect from 9thOctober 2019. However, the availability of ITC was subjected to restrictions and conditions specified in Section 16 of CGST Act from 1stJuly, 2017 itself. In view of this, various representations have been received from the trade as well as the tax authorities, seeking clarification regarding the manner of dealing with such discrepancies between the amount of ITC availed by the registered persons in their FORM GSTR-3B and the amount as available in their FORM GSTR-2A during FY 2017-18 and FY 2018-19.

3. In order to ensure uniformity in the implementation of the provisions of the law across the field formations, the Board, in exercise of its powers conferred under section 168(1) of the CGST Act, hereby clarifies as follows:

4. The proper officer shall first seek the details from the registered person regarding all the invoices on which ITC has been availed by the registered person in his FORM GSTR 3B but which are not reflecting in his FORM GSTR 2A. He shall then ascertain fulfillment of the following conditions of Section 16 of CGST Act in respect of the input tax credit availed on such invoices by the said registered person.

i) that he is in possession of a tax invoice or debit note issued by the supplier or such other tax paying documents;

ii) that he has received the goods or services or both;

iii) that he has made payment for the amount towards the value of supply, along with tax payable thereon, to the supplier.

Besides, the proper officer shall also check whether any reversal of input tax credit is required to be made in accordance with section 17 or section 18 of CGST Act and also whether the said input tax credit has been availed within the time period specified under sub-section (4) of section 16 of CGST Act.

4.1 In order to verify the condition of clause (c) of sub-section (2) of Section 16 of CGST Act that tax on the said supply has been paid by the supplier, the following action may be taken by the proper officer:

4.1.1 In case, where difference between the ITC claimed in FORM GSTR-3B and that available in FORM GSTR 2A of the registered person in respect of a supplier for the said financial year exceeds Rs 5 lakh, the proper officer shall ask the registered person to produce a certificate for the concerned supplier from the Chartered Accountant (CA) or the Cost Accountant (CMA), certifying that supplies in respect of the said invoices of supplier have actually been made by the supplier to the said registered person and the tax on such supplies has been paid by the said supplier in his return in FORM GSTR 3B. Certificate issued by CA or CMA shall contain UDIN. UDIN of the certificate issued by CAs can be verified from ICAI website https://udin.icai.org/search-udin and that issued by CMAs can be verified from ICMAI website https://eicmai.in/udin/VerifyUDIN.aspx.

4.1.2 In cases, where difference between the ITC claimed in FORM GSTR-3B and that available in FORMGSTR 2A of the registered person in respect of a supplier for the said financial year is up to Rs 5 lakh, the proper officer shall ask the claimant to produce a certificate from the concerned supplier to the effect that said supplies have actually been made by him to the said registered person and the tax on said supplies has been paid by the said supplier in his return in FORM GSTR 3B.

4.2 However, it may be noted that for the period FY 2017-18, as per proviso to section 16(4)of CGST Act, the aforesaid relaxations shall not be applicable to the claim of ITC made in the FORM GSTR-3B return filed after the due date of furnishing return for the month of September,2018 till the due date of furnishing return for March,2019, if supplier had not furnished details of the said supply in his FORM GSTR-1 till the due date of furnishing FORM GSTR 1 for the month of March,2019.

5. It may also be noted that the clarifications given hereunder are case specific and are applicable to the bonafide errors committed in reporting during FY 2017-18 and 2018-19. Further, these guidelines are clarificatory in nature and may be applied as per the actual

facts and circumstances of each case and shall not be used in the interpretation of the provisions of law.

6. These instructions will apply only to the ongoing proceedings in scrutiny/audit/ investigation, etc. for FY 2017-18 and 2018-19 and not to the completed proceedings. However, these instructions will apply in those cases for FY 2017-18 and 2018-19 where any adjudication or appeal proceedings are still pending.

7. Difficulty, if any, in the implementation of the above instructions may please be brought to the notice of the Board. Hindi version would follow.