Integrated Tax Notifications (Rate)

IGST Notification rate 08/2017

| Title | To notify the rates for supply of services under IGST Act |

| Number | 08/2017 |

| Date | 28-06-2017 |

| Download | |

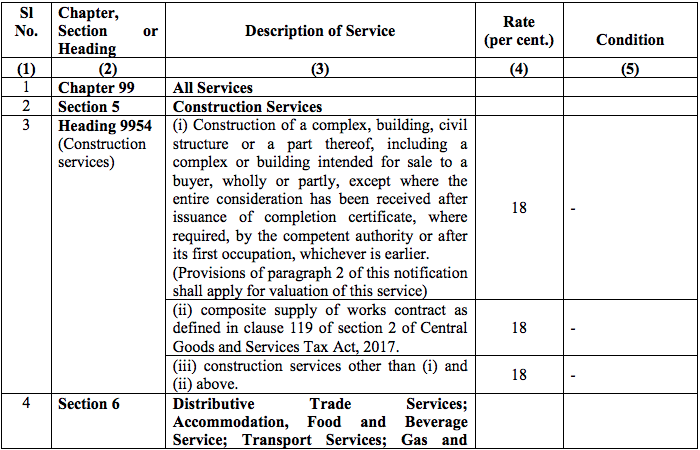

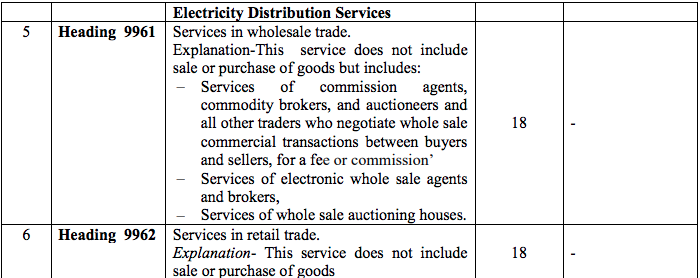

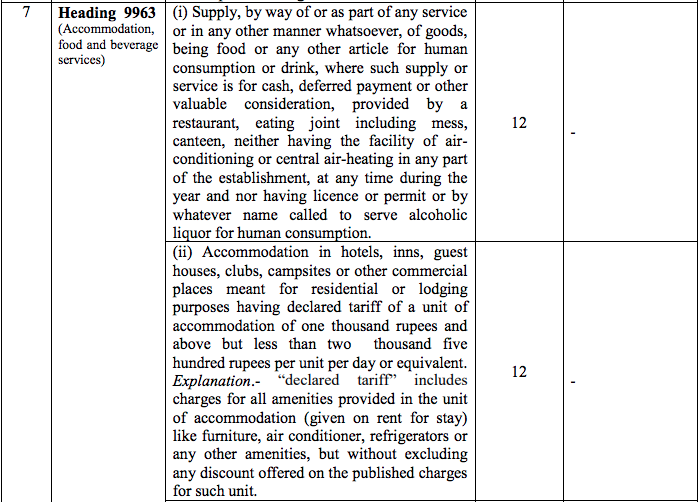

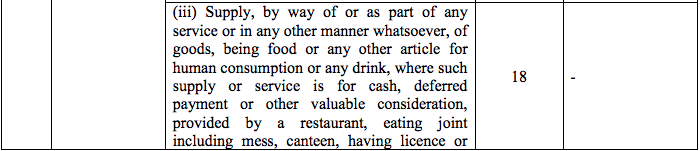

1) In exercise of the powers conferred by sub-section (1) of section 5, subsection (1) of section 6 and clause (iii) and clause (iv) of section 20 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017) read with sub-section (5) of section 15 and sub-section (1) of section 16 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, and on being satisfied that it is necessary in the public interest so to do, hereby notifies that the integrated tax, on the inter-State supply of services of description as specified in column (3) of the Table below, falling under Chapter, Section or Heading of scheme of classification of services as specified in column (2), shall be levied at the rate as specified in the corresponding entry in column (4), subject to the conditions as specified in the corresponding entry in column (5) of the said Table:-

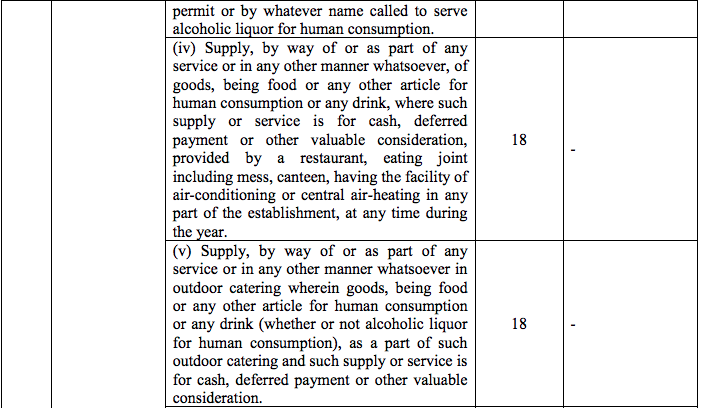

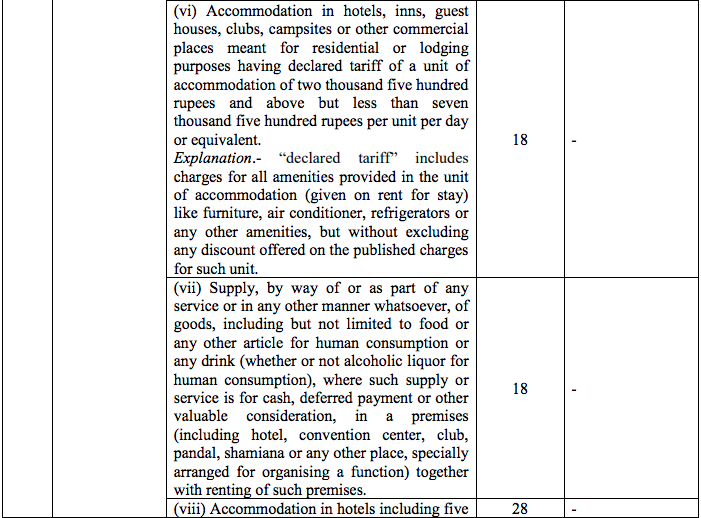

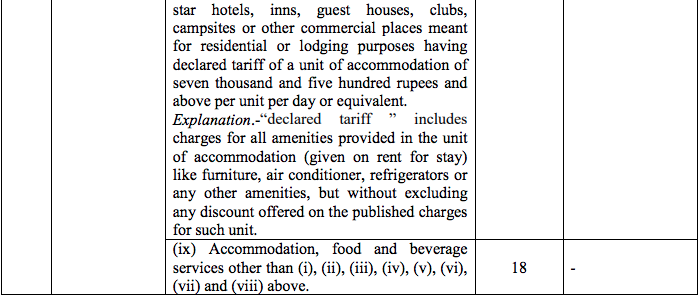

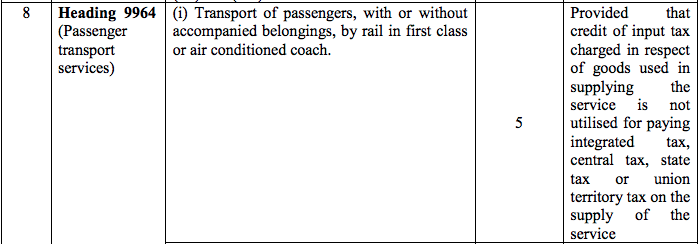

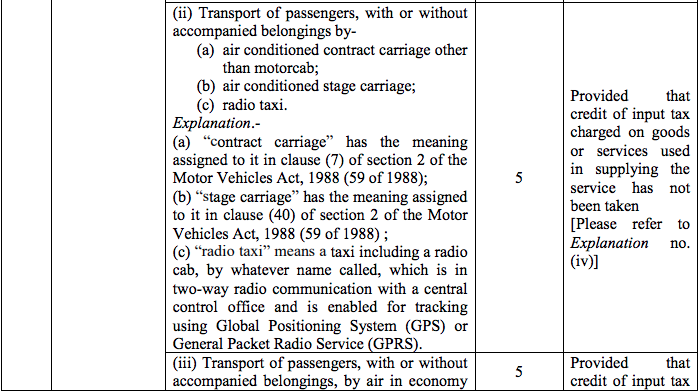

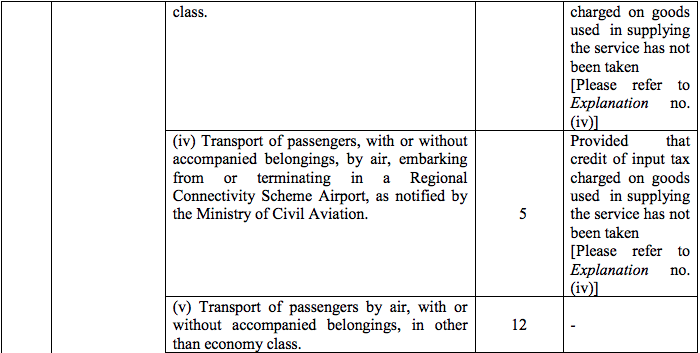

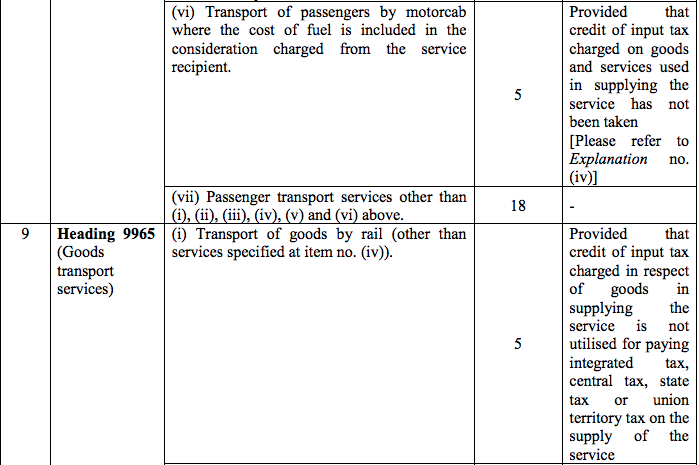

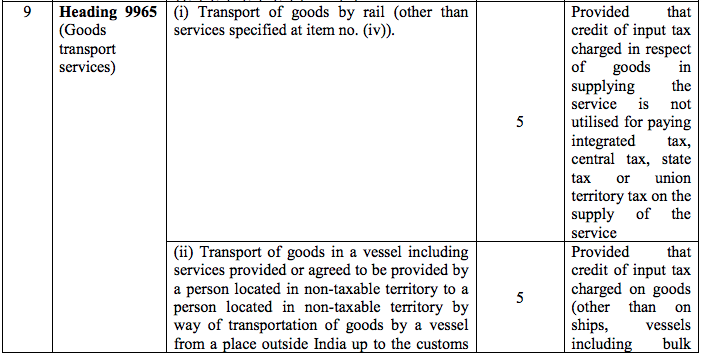

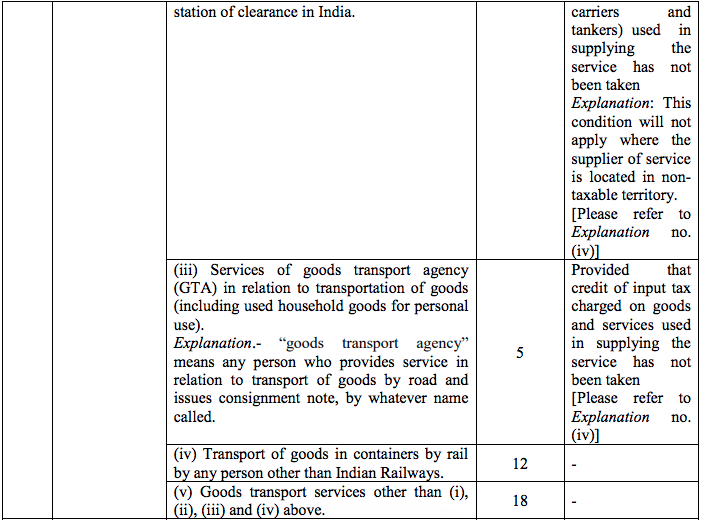

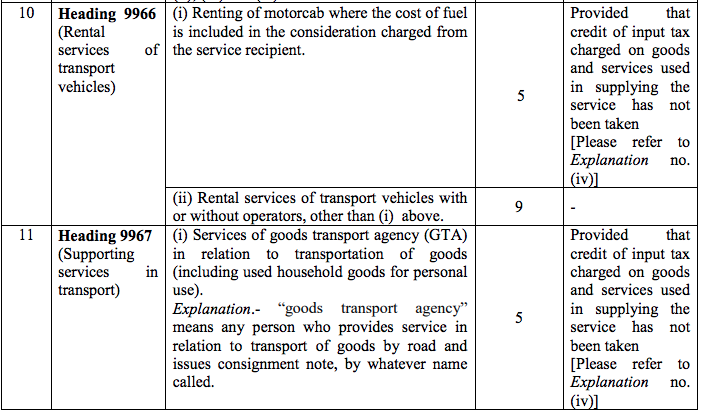

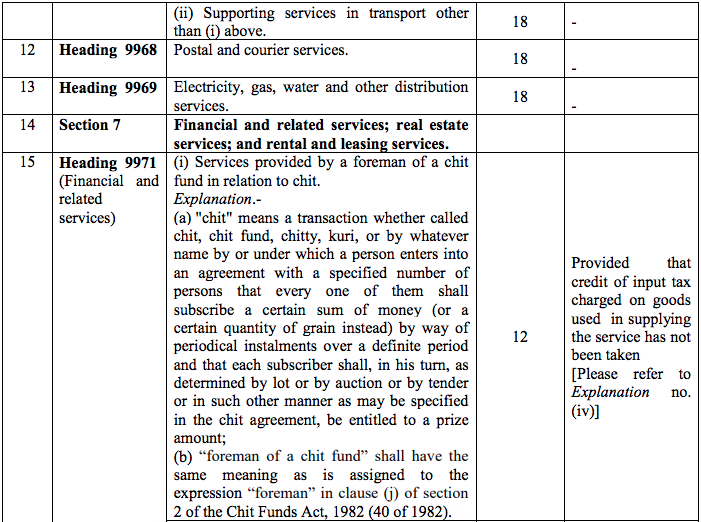

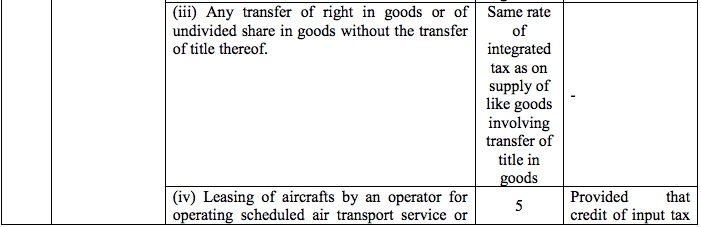

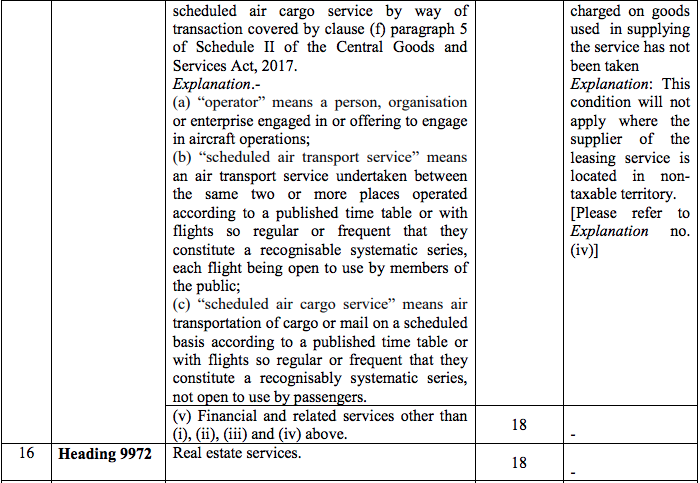

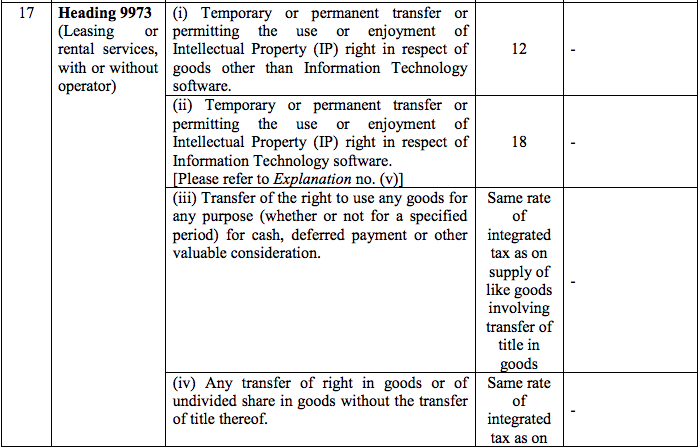

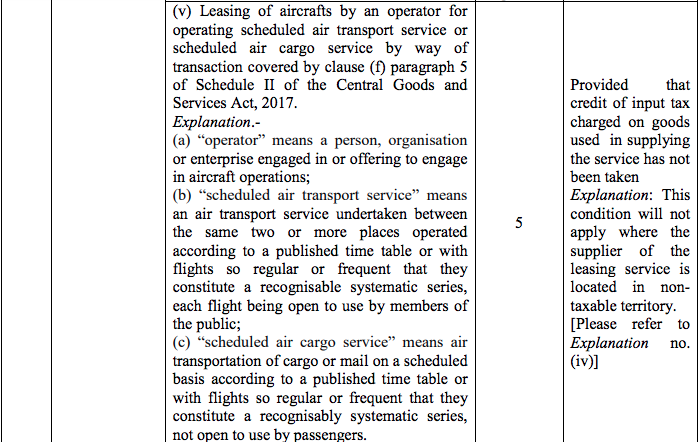

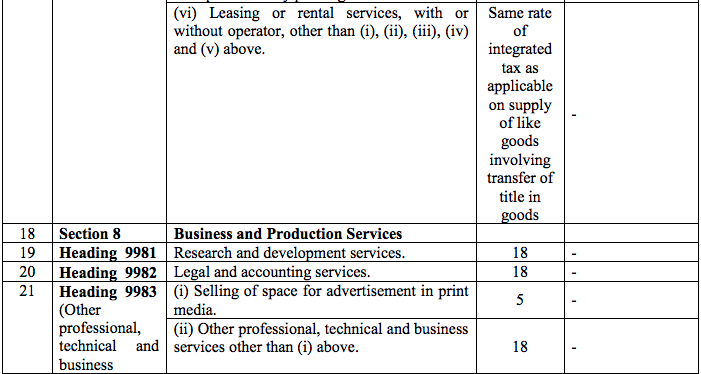

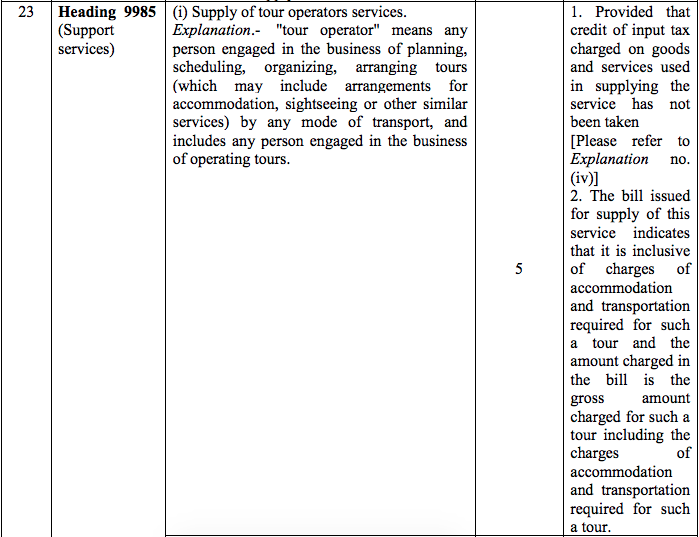

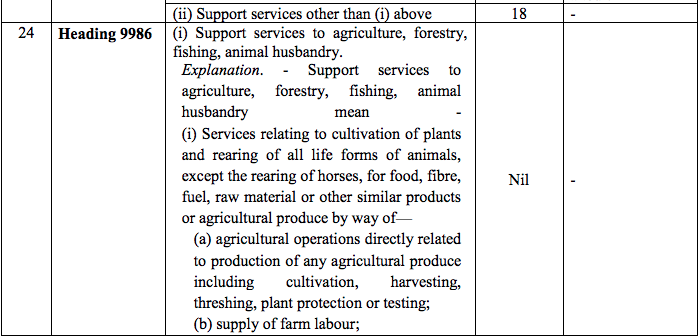

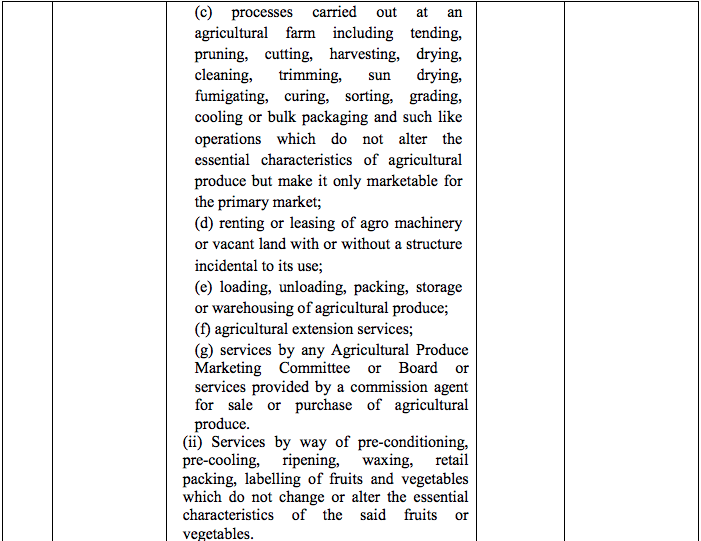

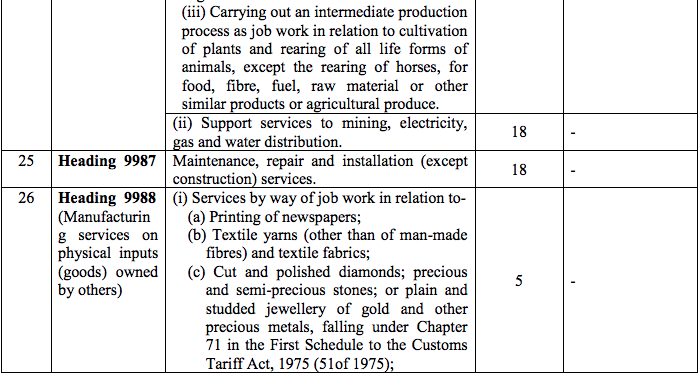

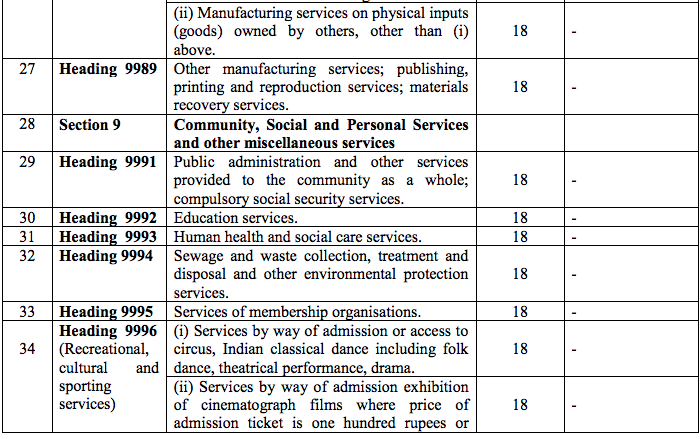

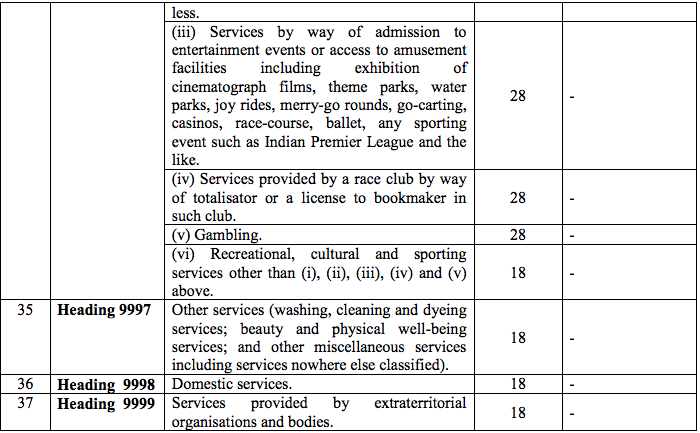

Table

2) In case of supply of service specified in column (3) of the entry at item (i) against serial no. 3 of the Table above, involving transfer of property in land or undivided share of land, as the case may be, the value of supply of service and goods portion in such supply shall be equivalent to the total amount charged for such supply less the value of land or undivided share of land, as the case may be, and the value of land or undivided share of land, as the case may be, in such supply shall be deemed to be one third of the total amount charged for such supply.

Explanation .– For the purposes of paragraph 2, “total amount” means the sum total of,-

(a) consideration charged for aforesaid service; and

(b) amount charged for transfer of land or undivided share of land, as the case may be.

3) Value of supply of lottery shall be 100/112 of the face value or the price notified in the Official Gazette by the organising State, whichever is higher, in case of lottery run by State Government and 100/128 of the face value or the price notified in the Official Gazette by the organising State, whichever is higher, in case of lottery authorised by State Government.

4) Explanation.- For the purposes of this notification,-

(i) Goods includes capital goods.

(ii) Reference to “Chapter”, “Section” or “Heading”, wherever they occur, unless the context otherwise requires, shall mean respectively as “Chapter, “Section” and “Heading” in the scheme of classification of services.

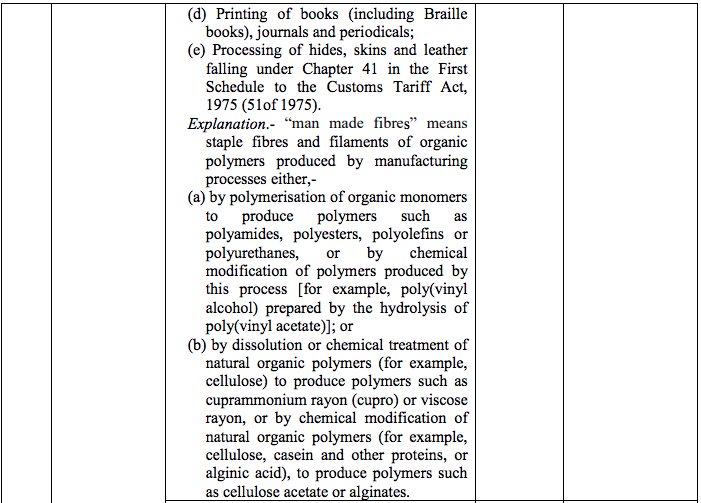

(iii) The rules for the interpretation of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975), the Section and Chapter Notes and the General Explanatory Notes of the First Schedule shall, so far as may be, apply to the interpretation of heading 9988.

(iv) Wherever a rate has been prescribed in this notification subject to the condition that credit of input tax charged on goods or services used in supplying the service has not been taken, it shall mean that,-

(a) credit of input tax charged on goods or services used exclusively in supplying such service has not been taken; and

(b) credit of input tax charged on goods or services used partly for supplying such service and partly for effecting other supplies eligible for input tax credits, is reversed as if supply of such service is an exempt supply and attracts provisions of clause (iv) of section 20 of the Integrated Goods and Services Tax Act, 2017 read with sub-section (2) of section 17 of the Central Goods and Services Tax Act, 2017 and the rules made thereunder.

(v) “information technology software” means any representation of instructions, data, sound or image, including source code and object code, recorded in a machine readable form, and capable of being manipulated or providing interactivity to a user, by means of a computer or an automatic data processing machine or any other device or equipment.

(vi) “agricultural extension” means application of scientific research and knowledge to agricultural practices through farmer education or training;

(vii)“agricultural produce” means any produce out of cultivation of plants and rearing of all life forms of animals, except the rearing of horses, for food, fibre, fuel, raw material or other similar products, on which either no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market;

(viii)“Agricultural Produce Marketing Committee or Board” means any committee or board constituted under a State law for the time being in force for the purpose of regulating the marketing of agricultural produce;

5) This notification shall come into force with effect from 1st day of July, 2017.