Agenda for 50th GST Council Meeting 11th July 2023

Volume-II

GST Council Secretariat New Delhi

OFFICE MEMORANDUM

Subject: Notice for the 50th Meeting of the GST Council scheduled to be convened on 11th July, 2023.

The undersigned is directed to refer to the subject stated above and to convey that the 50th Meeting of the GST Council will be held on 11th July, 2023 at New Delhi. The schedule of the Meeting is as follows:

- Tuesday, 11th July, 2023: 11:00 A.M. onwards

- In addition, an Officers’ Meeting will be held on 10th July, 2023 as per the following schedule:

- Monday, 10th July, 2023: 2: 00 P.M. onwards

- The agenda items and other details for the 50th Meeting of the GST Council will be communicated in due course of time.

- Keeping in view the logistical constraints, it is requested that participation from each State/UT may be kept limited to two (02) officers in addition to the Hon’ble Member of the GST Council.

- Kindly convey the invitation to Hon’ble Member of the GST Council to attend the Meeting of the GST Council.

Sd/-

(Sanjay Malhotra) Secretary to the Govt. of India and ex-officio Secretary to the GST Council

Tel: 011 23092653 Copy to:

- PS to the Hon’ble Minister of Finance, Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

- PS to the Hon’ble Minister of State (Finance), Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

- The Chief Secretaries of all the State Governments, Union Territories of Delhi, Puducherry and Jammu and Kashmir with the request to intimate the Minister in charge of Finance/Taxation or any other Minister nominated by the State Government as a Member of the GST Council about the above said meeting.

- Chairman, CBIC, North Block, New Delhi, as a permanent invitee to the proceeding of the Council.

- Chairman, GST Network.

Agenda Item 9: Report of 3rd Meeting of the Group of Ministers (GoM) on GST System Reforms

The GST Council in its 45th Meeting had decided to constitute a Group of Ministers (GoM) on System Reforms to analyse, to study and come up with ways and means to minimize tax evasion and offer other suggestions that can help avoid frauds in GST. The GoM was constituted vide OM dated 24.09.2021 by subsuming the earlier GoMs on IT challenges and revenue mobilization.

- Vide OM dated 22nd September 2022, the GoM has been reconstituted and the present constitution of the Group of Ministers committee is as follows:

| S.No. | Name | Designation | Convener/ Member |

| 1 | Shri Devendra Fadnavis | Deputy Chief Minister,Maharashtra | Chairman and Convener |

| 2 | Shri Dushyant Chautala | Deputy Chief Minister, Haryana | Member |

| 3 | Shri Manish Sisodia | Deputy Chief Minister, Delhi | Member |

| 4 | Smt. Ajanta Neog | Minister for Finance, Assam | Member |

| 5 | Shri Buggana Rejendranath | Minister for Finance, Planning and Legislative Affairs, Andhra Pradesh | Member |

| 6 | Shri Niranjan Pujari | Minister for Finance and Excise, Odisha | Member |

| 7 | Dr. Palanivel Thiaga Rajan | Minister for Finance and Human Resources Management, Tamil Nadu | Member |

| 8 | Shri T.S. Singh Deo | Minister for Commercial Taxes, Chhattisgarh | Member |

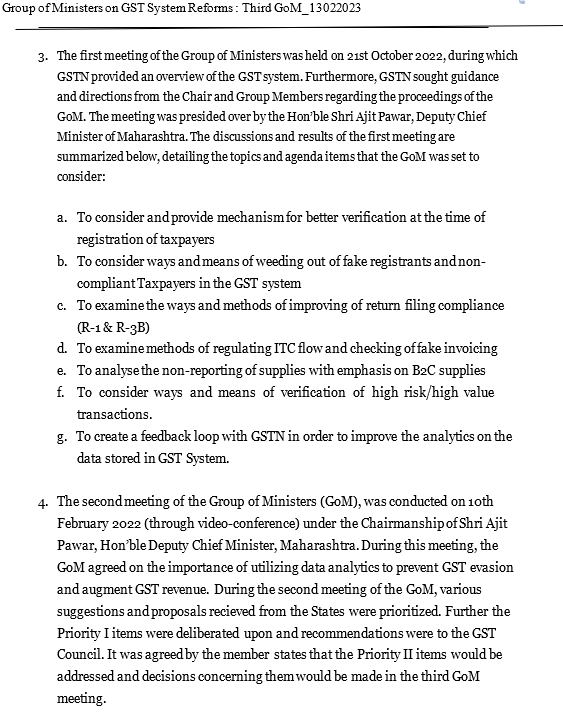

- The first meeting of the Group of Ministers was held on 21st October 2022 and the second meeting of the Group of Ministers (GoM), was conducted on 10th February, 2022 (through videoconference). The First Report of the GoM based on the approved minutes of these meeting was tabled before the GST Council in its 47th Meeting held on 28th and 29th June, 2022 at Chandigarh.

4. Third Meeting of GoM on System Reforms

4.1 The GoM on GST System Reforms held its 3rd Meeting on 13th February, 2023 under the Chairmanship of the Hon’ble Convenor of the GoM, Shri Devendra Fadnavis, Hon’ble Deputy Chief Minister of Maharashtra and the meeting was attended by Members from Haryana, Tamil Nadu, Delhi, Odisha and Andhra Pradesh. Members from Assam and Chhattisgarh were unable to attend due to prior commitments. Gujarat and Telangana were the special invitees at the meeting. Gujarat has been implementing a Biometric Authentication Pilot Project and the State of Telangana had been using data analytics on the Point of Sale (PoS) data to identify tax evaders.

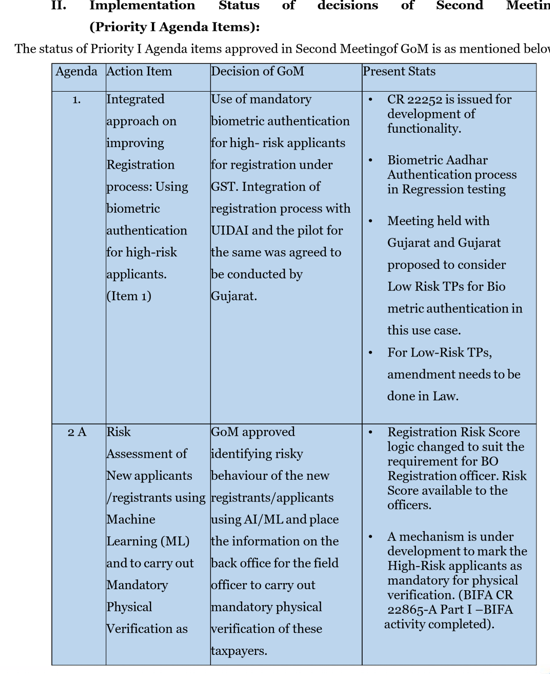

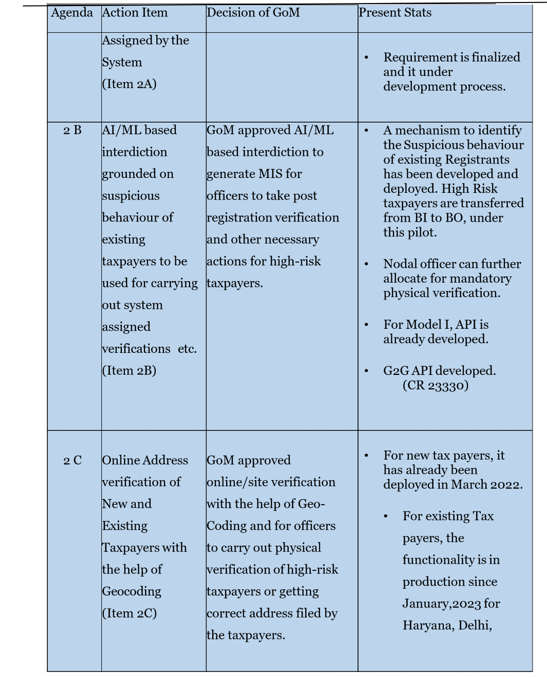

5. Implementation Status of decisions of Second Meeting (Priority I Agenda Items)

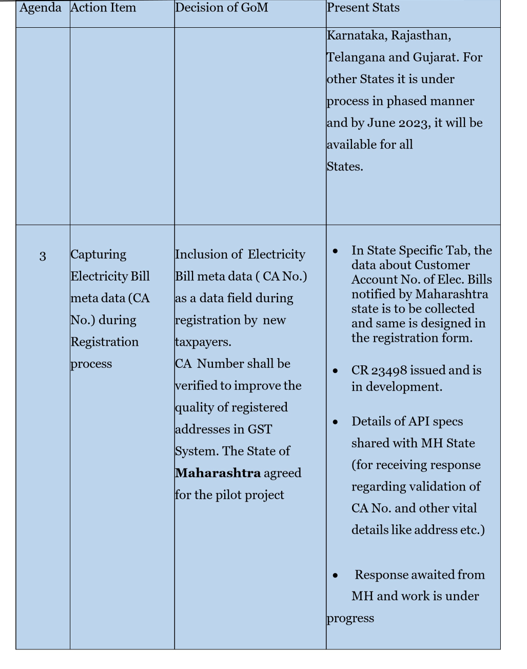

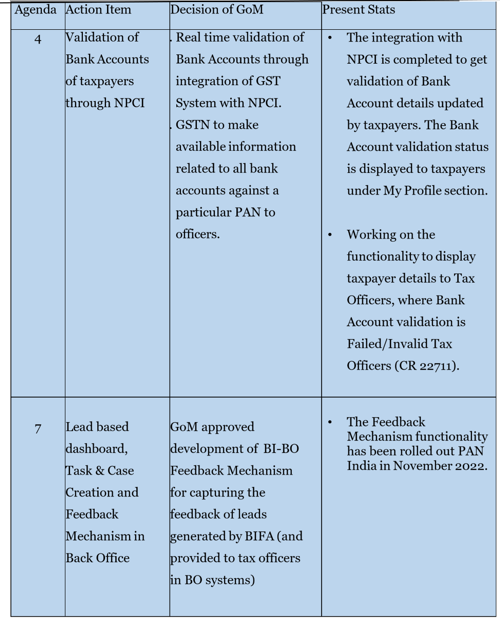

5.1 The implementation status of Priority I Agenda items as approved in Second Meeting of GoM is detailed out in the Report of 3rd Meeting of the GoM (pages 6- 9 of the Report).

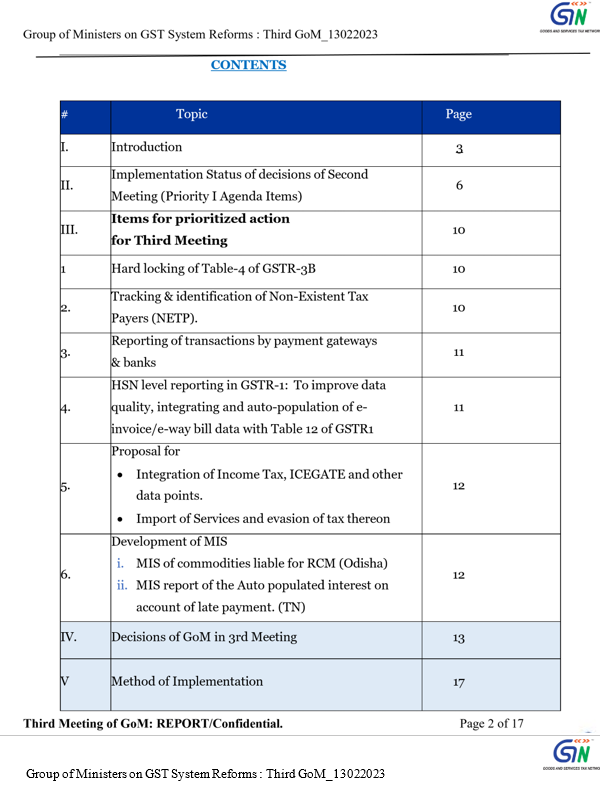

6. Items for prioritized action for 3rd Meeting of GoM

6.1 Accordingly, after receipt of the suggestions of the States and due deliberations, the final set of Priority II agenda items for the 3rd meeting were determined by the GoM as follows:

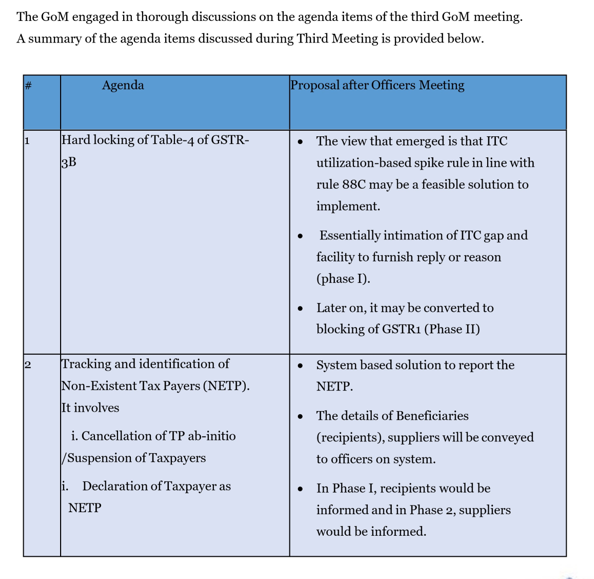

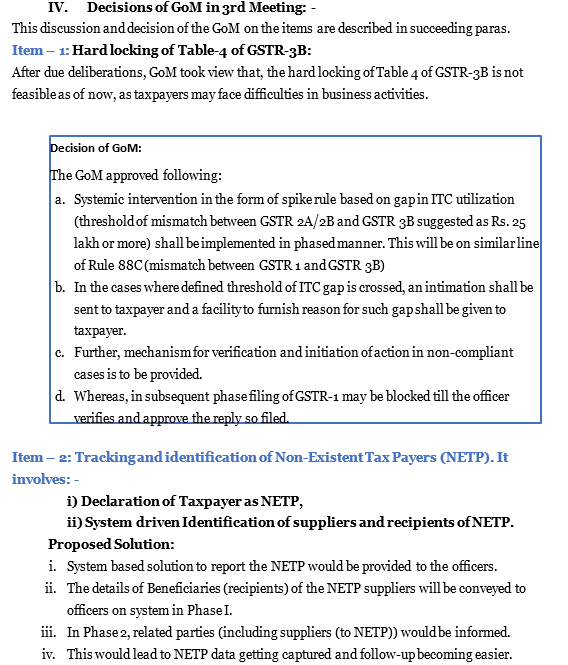

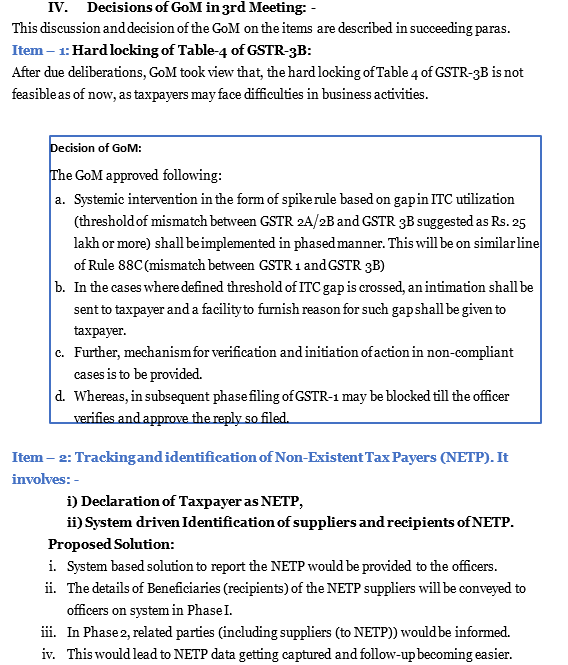

- Hard locking of Table-4 of GSTR-3B.

- Tracking and identification of Non-Existent Tax Payers (NETP).

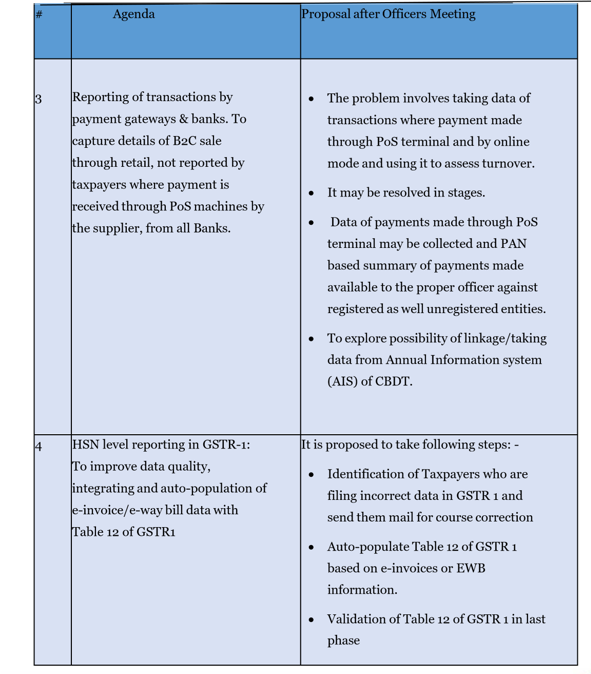

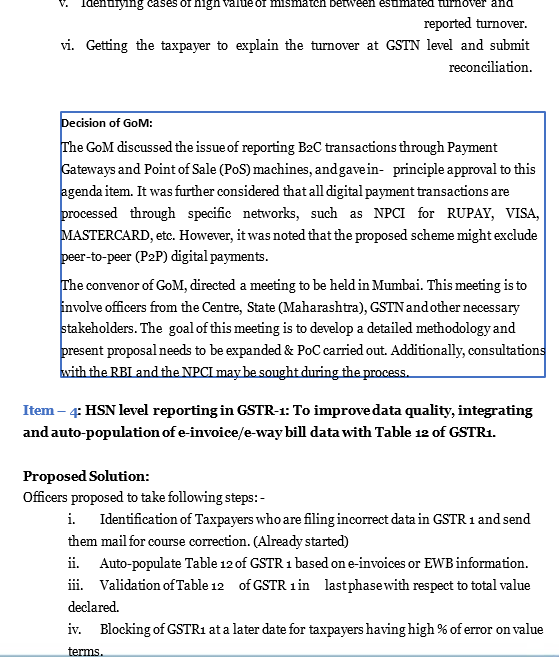

- Reporting of transactions by payment gateways & banks.

- HSN level reporting in GSTR-1.

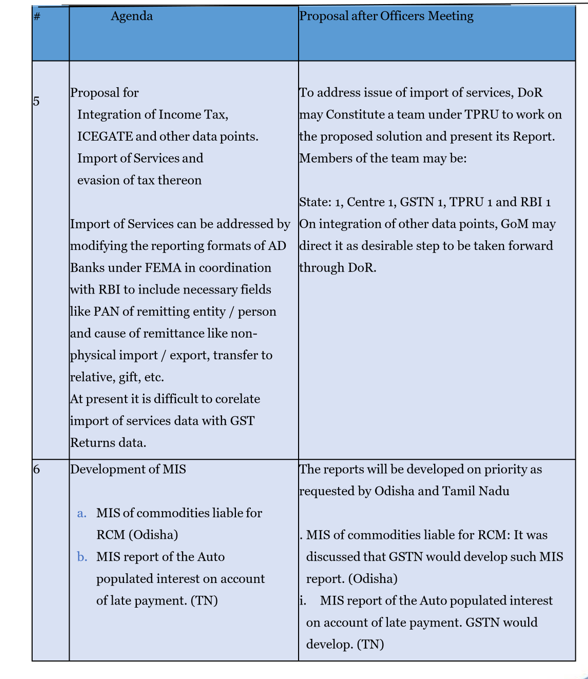

- Proposal for

- Integration of Income Tax, ICEGATE and other data points. ii. Import of Services and evasion of tax thereon

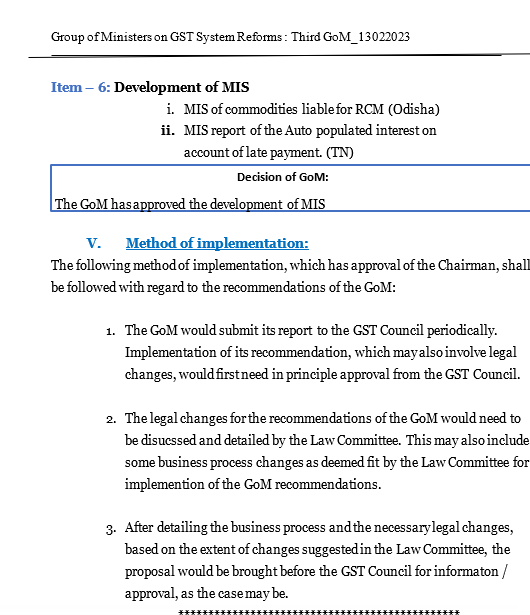

- Development of MIS

- MIS of commodities liable for RCM (Odisha) ii. MIS report of the Auto populated interest on account of late payment. (TN)

7.The detailed discussion and decisions of the GoM on GST System Reforms with respect to these Priority II agenda items are detailed out in the Report of 3rd Meeting of GoM on GST Systems having the approval of the Hon’ble Convenor of the GoM and is placed as Annexure A.

8. Decisions of GoM in 3rd Meeting

8.1 GoM has inter alia approved following decisions and recommendations for placing before GST Council:

8.1.1 Approved systemic intervention in the form of spike rule based on gap in ITC utilization (threshold of mismatch between GSTR 2A/2B and GSTR 3B suggested as Rs. 25 lakh or more) shall be implemented in phased manner. This will be on similar line of Rule 88C (mismatch between GSTR 1 and GSTR 3B). In the cases where defined threshold of ITC gap is crossed, an intimation shall be sent to taxpayer and a facility to furnish reason for such gap shall be given to taxpayer.

8.1.2 Approved to formulate an SoP for handling NETP and a uniform policy for ab-initio cancellation of NETP across State/CBIC Tax Administration to be followed. An SoP for the same may be issued by policy wing. Further to develop System driven solution to facilitate the declaration of NETP by Tax Administration.

8.1.3 The issue of reporting B2C transactions through Payment Gateways and Point of Sale (PoS) machines was considered and the GoM gave in-principle approval to this agenda item.

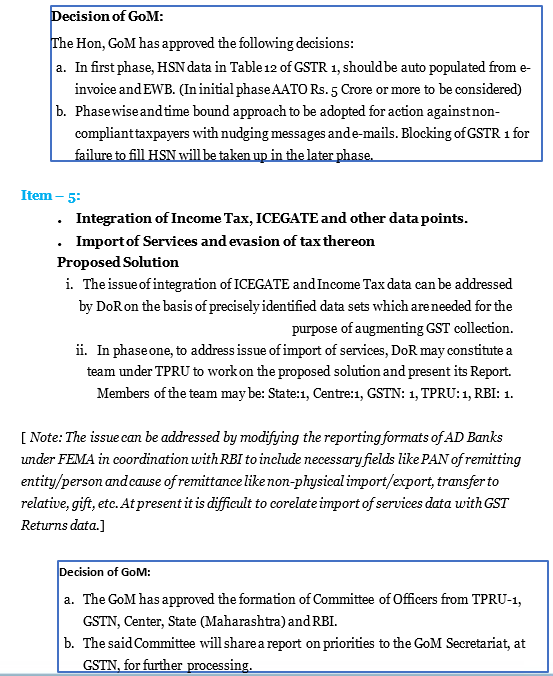

8.1.4 Approved that in first phase, HSN data in Table 12 of GSTR 1, should be auto populated from einvoice and EWB. (In initial phase AATO Rs. 5 Crore or more to be considered). Further, phase wise and time bound approach to be adopted for action against noncompliant taxpayers with nudging messages and e-mails. Blocking of GSTR 1 for failure to fill HSN will be taken up in the later phase.

8.1.5 Approved the formation of Committee of Officers from TPRU-1, GSTN, Center, State (Maharashtra) and RBI and the said Committee will share a report on priorities to the GoM Secretariat, at GSTN, for further processing.

8.1.6 Approved the development of MIS.

9. Method of Implementation

9.1 The method of implementation for implementation of the recommendation of GoM as agreed upon by the Members are as follows:

9.1.1 The GoM would submit its report to the GST Council periodically. Implementation of its recommendation, which may also involve legal changes, would first need in principle approval from the GST Council.

9.1.2 The legal changes for the recommendations of the GoM would need to be discussed and detailed by the Law Committee. This may also include some business process changes as deemed fit by the Law Committee for implementation of the GoM recommendations.

9.1.3 After detailing the business process and the necessary legal changes, based on the extent of changes suggested in the Law Committee, the proposal would be brought before the GST Council for information / approval, as the case may be.

- The Report of the 3rd Meeting of GoM on GST System Reforms (Annexure A) having approval of the Hon’ble Convenor of the GoM, is placed before the GST Council for consideration and approval.

GoM on GST System Reforms: Report of Third Meeting

Group of Ministers (GoM) on GST System Reforms: Report on

Recommendations of Third Meeting

I. Introduction

- During the 45th meeting of the GST Council, held on 21st September 2021, it was decided to constitute a sub-committee of Group of Ministers (GoM). The GoM was tasked with the objective of analyzing, studying, and proposing strategies to curb tax evasion. Additionally, they were assigned to provide suggestions that might aid in preventing fraudulent activities within the GST framework.

- As per the OM dated 22nd September 2022, the GoM is reconstituted and present Membership of the GoM is as follows:

| # | Name | Designation | Convener/

Member |

|

| 1. | Shri Devendra Fadnavis | Deputy Chief Maharashtra | Minister, | Chairman and Convener |

| 2. | Shri Dushyant Chautala | Deputy Chief Haryana | Minister, | Member |

| 3. | Shri Manish Sisodia | Deputy Chief Delhi | Minister, | Member |

| 4 | Smt.Ajanta Neog | Minister for Assam | Finance, | Member |

| 5 | Shri Buggana

Rejendranath |

Minister for Planning and

Affairs, Andhra P |

Finance,

Legislative radesh |

Member |

| 6 | Shri Niranjan Pujari | Minister for Finance and

Excise, Odisha |

Member | |

| 7 | Dr. Palanivel Thiaga Rajan | Minister for Finance and Human Resources Management, Tamil Nadu | Member | |

| 8 | Shri T.S. Singh Deo | Minister for Commercial Taxes, Chhattisgarh | Member | |

|

|

|

|

|

Agenda Item 10: Proposal for creation of State Co–ordination Committee comprising of the GST authorities from the State and the Central Tax Administrations.

- The National Coordination Meeting was held on 24th April, 2023 under the

Chairmanship of the Revenue Secretary. As an outcome, it was decided to launch an All India drive against fake registrations. Instructions No.1/2023 dated 04.05.2023 regarding the conduct of the special drive were issued. Also, a National Coordination Committee headed by Member (GST), CBIC and comprising Chief Commissioner/Commissioner of State Taxes of Gujrat, Telangana,

West Bengal and Principal/Chief Commissioner of Delhi CGST Zone and Bhopal CGST Zone as

Members was formed to monitor the progress of the drive against fake registrations and fake ITC. The results of this coordinated drive against fake registrations and fake ITC have been very encouraging.

- The fake registration cases require follow up in cases where the ITC has been passed on. For sharing of this information regarding follow up of the fake drive cases and other enforcement measures at ground level, for sharing of Audit findings and other audit related matters, for adopting a common legal stand/strategy, it is proposed that there should be an institutionalized platform for information sharing and collaboration across Central and State GST

- It is proposed that a Co-ordination Committee may be formed in each State/UTs comprising of Central and State Tax Authorities for knowledge sharing on GST matters and coordinated efforts towards administrative and preventive

- The constitution of the said Committee, its functions, mandate/scope, frequency of the meetings is proposed below. Further, whereas the Chief Commissioner/Commissioners of CGST/SGST shall be co-chairs, they shall be conveners on rotational basis for one year eac

- Constitution of the Committee:

The proposed Constitution of the Committee is as follows:

- Zonal Principal Chief Commissioner/ Chief Commissioner of Central Tax (Co- chair) ii. Chief Commissioner/ Commissioner of State Tax (Co-chair) iii. Representative of DG GST Intelligence (DGG), CBIC from concerned Zone/ State iv. Additional/Joint Commissioner of office of Zonal Principal Chief Commissioner/ Chief Commissioner of Central Tax and an officer nominated by the Chief Commissioner/ Commissioner of State Tax,

- Any other member/officer may be co-opted with the permission of the Co- chairs.

The co-opted officers could be officers well conversant with the ground level issues and serve for greater coordination between Centre and States.

- Term of the Committee – The Committee will be constituted on perpetual basis.

- Functions and mandate of the Committee:

- The Committee shall engage in data sharing on important cases of evasion or audit, knowledge sharing and promote coordinated efforts in checking fake ITC being passed on, curbing tax evasion practices, sharing important audit paras & modus-operandi detected in Audit/Investigation, maintaining and updating contact details of field level officers and other GST related matters.

- Referring any issue requiring a change in Act/Rules/Notification/ Form/Circular/Instruction/improvement on GST portal, etc., to the GST Council Secretariat and the relevant Policy Wing of the CBIC/ GSTN/ DoR.

- Make collaborative efforts on the issues pertaining to taxpayer facilitation as well as taxpayer grievances and conducting outreach p

- To arrive at a uniform stand by the Central and State GST Administration in GST related petitions before any legal forum.

- Co-ordination in the matter regarding Investigation/anti-evasion proceedings so as to ensure that on the same issue, investigation in respect of taxpayers are not undertaken by multiple administratio

- Conducting a coordinated verification drive for suspicious tax payers at local level.

- Any other GST matter deemed fit for coordinated work between Central and State Tax Administrations.

- Periodicity of Meeting of the Committee- The Committee shall meet once every quarter or as the Co-chairs may decide.

Agenda Item 11: Implementation of GSTAT consequent to passing of Finance Act, 2023

The final Report and recommendations of the Group of Ministers (GoM) on constitution of Goods and Services Tax Tribunal constituted vide OM No. A-50050/150/2018-Cestat-DoR was tabled before the GST Council in its 49th Meeting.

- After detailed deliberations, the Council recommended that there should be one GST Appellate Tribunal with a Principal Bench and State Benches. Each Bench of the Appellate Tribunal would consist of four members i.e. two Judicial Members and two Technical Members, one Member from Centre and one from the State. Appeals, where the tax or input tax credit involved or the amount of fine, fee or penalty determined in any order appealed against, does not exceed fifty lakh rupees and which does not involve any question of law may, with the approval of the President, and subject to such conditions as may be prescribed on the recommendations of the Council, be heard by a single Member, and in all other cases, shall be heard together by one Judicial Member and one Technical Member.

- The report of GoM on GSTAT was adopted by the Council with certain modifications. Further, the amendments in CGST Act relating to the constitution of GST Appellate Tribunal have been incorporated through Finance Act, 2023 (refer clause 149-154 of the Finance Act, 2023), by substitution of sections 109, 110 and 114 of CGST Act, 2017 and by amending sections 117, 118 and 119 of CGST Act, 2017.

- The status of corresponding amendments proposed to be made in State/UT GST Acts and number & location of proposed Tribunal benches in States/UT are compiled and placed as Annexure A along with their jurisdictions.

- The GST Council may recommend a suitable date for notifying the amendments to CGST Act, 2017 made vide Finance Act, 2023. Accordingly, the States/UTs with legislature may also notify the corresponding amendments in their respective Acts on the same date. The GSTAT would be constituted after these amendments are notified.

- As per Sec 110(4)(b)(iii) of CGST Act 2017, the Search-cum-Selection Committee for all cases other than Technical Member (State) of a State Bench shall have Chief Secretary of a State to be nominated by the Council as one of the Members. Accordingly, the GST Council may make suitable recommendations in this regard. The list of States is given in Column 2 of Annexure A.

- Further, in case of North Eastern States, it is submitted that there are five High Courts in North East in the States of Tripura, Sikkim, Meghalaya, Manipur and Assam. In case of Arunachal Pradesh and Meghalaya, the GSTAT has been proposed at Guwahati, Assam. It is proposed that it may be clarified that the appeal arising out of GSTAT order in such cases will fall within jurisdiction of the High Court of the State where the taxpayer is located and not in the High Court of Guwahati for clarity of the taxpayers and the department. Meghalaya has also requested for this clarification.

Annexure A

Status of confirmation of Amendments to SGST/UTGST Act corresponding to formation of GSTAT

| S.No. | State | Act | Ordinance | No. of Benches proposed | Location of Benches proposed * |

| 1 | Andhra Pradesh | under process | 3 | Vijayawada, Visakhapatnam, Tirupati | |

| 2 | Arunachal

Pradesh |

under process | Common Bench with

Guwahati, Assam |

Guwahati | |

| 3 | Assam | Passed | 1 | Guwahati | |

| 4 | Bihar | under process | 1 | Patna | |

| 5 | Chhattisgarh | under process | 2 | Raipur,

Bilaspur |

|

| 6 | Delhi | under process | 2 | Delhi | |

| 7 | Goa | under process | 1 | Panaji | |

| 8 | Gujarat | under process | 3 | Ahmedabad,

Surat, Rajkot |

|

| 9 | Haryana | under process | 2 | Gurugram

Hisar |

|

| 10 | Himachal

Pradesh |

under process | 1 | Shimla | |

| 11 | Jammu and

Kashmir |

under process | 1 | Jammu & Srinagar on rotational basis | |

| 12 | Jharkhand | under process | 1 | Ranchi | |

| 13 | Karnataka | under process | 3 | All three in Bengaluru | |

| 14 | Kerala | under process | 3 | Thiruvananthapuram,

Ernakulam, Kozhikode |

|

| 15 | Madhya

Pradesh |

under process | 1 | Bhopal | |

| 16 | Maharashtra | ||||

| 17 | Manipur | under process | |||

| 18 | Meghalaya | under process | Common Bench with

Guwahati, Assam |

Guwahati | |

| 19 | Mizoram | under process | 1 | Aizawl | |

| 20 | Nagaland | under process | |||

| 21 | Odisha | under process | 1 | Cuttuck | |

| 22 | Punjab | under process | 1 | Chandigarh/Mohali | |

| 23 | Puducherry | under process | 1 | Puducherry | |

| 24 | Rajasthan | under process | |||

| 25 | Sikkim | under process | Common Bench with

Kolkata |

Kolkata | |

| 26 | Tamil Nadu | ||||

| 27 | Telangana | 2 | Both at Hyderabad | ||

| 28 | Tripura | under process | 1 | Agartala | |

| 29 | Uttarakhand | under process | 1 | Dehradun | |

| 30 | Uttar Pradesh | under process | 5 | Lucknow , Varanasi,

Ghaziabad, Agra and Prayagraj |

|

| 31 | West Bengal | under process | 2 | Both at Kolkata |

* The States of Andhra Pradesh, Chhattisgarh, Gujarat, Kerala, Telangana and Uttar Pradesh have defined the jurisdictions of the Benches based on Division/Zone/Revenue division.

Karnataka and West Bengal have defined the jurisdiction of the Benches as entire state jurisdiction.

Agenda Item 12: Performance Report of Competition Commission of India (CCI) for month of December, 2022 and 4th quarter of the F.Y 2022-23 along with Performance Reports of State

Level Screening Committee (SLSC), Standing Committee (SC) and Directorate General of AntiProfiteering (DGAP) for 3rd quarter and 4th quarter of the F.Y 2022-23 for the information of the Council

The performance report of Anti-profiteering authorities at various levels are as under:

1.1. Performance of Competition Commission of India (CCI):

| Opening

Balance |

No. of

Investigation Reports received from DGAP |

Disposal of Cases | Closing

Balance

|

||||

| Total Disposal | No. of cases

Where Profiteering established |

No. of cases Where

Profiteering not established |

No. of cases referred

back DGAP |

to | |||

| December 2022* | |||||||

| 128 | 0 | 0 | 0 | 0 | 0 | 128 | |

| 4th Quarter-1st January 2023 to 31st March 2023 | |||||||

| 128 | 42 | 0 | 0 | 0 | 0 | 170 | |

*Report of National Anti-Profiteering Authority (NAA) for the month of October and November 2022 were tabled in 48th Meeting of GST Council. In accordance with the Notification No. 23/2022-Central Tax dated 23.11.2022, the mandate of NAA has been transferred to the Competition Commission of India (CCI) w.e.f 1st December, 2022.

1.2 Performance Report of DG of Anti-Profiteering (DGAP):

| Opening Balance (No.

of cases) |

Receipt | Disposal | Mode of disposal of cases | Closing Balance

(No. of cases)

|

|

| Report to NAA confirming profiteering | Report to NAA for closure

action |

||||

| 3rd Quarter- 1st October 2022 to 31st December 2022 | |||||

| 65 22 7 6 1 80*

|

|||||

| 4th Quarter – 1st January 2023 to 31st March 2023 | |||||

| 80 | 0 | 44 | 28 | 16 | 36**

|

*Out of these 80 cases, 26 cases have been stayed by various Hon’ble High Courts

- One case has been held up per direction by NAA.

- Actual pendency of cases in which investigation is under process are 53 only.

**Out of these 36 cases, 28 cases have been stayed by various Hon’ble High Courts.

- One case has been held up as per direction by NAA.

- Actual pendency of cases in which investigation is under process are 7 only.

1.3 Performance Report of the Standing Committee (SC) on Anti-profiteering:

| Opening Balance (No. of cases) | Receipt | Disposal | Closing Balance (No. of cases) |

| 3rd Quarter – 1st October, 2022 to 31st December, 2022 | |||

| 32* | 25 | 0 | 57 |

| 4th Quarter – 1st January, 2023 to 31st March, 2023 | |||

| 57 | 1 | 25 | 33 |

- The closing balance of quarter ending September 2022 and Opening Balance of Quarter ending December 2022 differs by 39 as complaints received in August and September 2022 got time barred due to administrative reasons.

1.4 Performance Report from the State Level Screening Committee (SLSC):

| Opening Balance (No.

of cases) |

Receipt | Disposal | Closing Balance (No.

of cases) |

||

| Cases referred

Standing Committee |

to | Cases Rejected | |||

| 3rd Quarter- 1st October, 2022 to 31st December, 2022 | |||||

| 94 91 3 | 0 182* | ||||

| 4th Quarter -1st January, 2023 to 31st March, 2023 | |||||

| 176** | 137 | 9 | 6 | 298 | |

- The Closing Balance of Quarter ending September 2022 and Opening Balance of Quarter ending December 2022 may differ by 1 due to non-receipt of report from State of Jharkhand.

** The closing balance of Quarter ending December 2022 and Opening Balance of Quarter ending March 2023 may differ by 6 due to non-receipt of report from Andhra Pradesh & Punjab.

- During these quarters CCI has undertaken the following activities/initiatives-

For the month of December 2022:-

- Vide Notification No. 23/2022-Central Tax dated 23.11.2022, the mandate of the Authority has been transferred to the Competition Commission of India (CCI) w.e.f 01.12.2022. In the absence of quorum of CCI, no matter was heard in the month of December 2022. At present, total 128 transferred cases related to anti-profiteering transferred matters are now pending for completion of proceedings at the level of CCI.

- The erstwhile NAA had passed 380 orders since its inception establishing profiteering of Rs. 2563 Cr. (Approx.) out of which amount of Rs. 563 Cr. (Approx.) has either been passed on to the buyers or deposited in the Consumer Welfare Funds or deposited with the High Courts.

- Forty-Four (44) complaints related to anti-profiteering provisions were received during the quarter ending December, 2022 via NAA portal, e-mails and by post. Twenty-Nine (29) complaints relating to profiteering in terms of Section 171 of the CGST Act, 2017 were forwarded to the respective Screening Committees/ Standing Committee for further action/examination thereof. Fifteen (15) complaints that related to other GST/enforcement issues were forwarded to the Jurisdictional State & Central GST Commissioners/ Chief Commissioners for necessary action.

For the quarter 01.01.2023 to 31.03.2023:- iv. At present, 170 cases related to anti-profiteering matters are pending with the CCI.

- Thirty-One (31) complaints related to anti-profiteering provisions were received during the quarter ending March, 2023 via NAA portal, e-mails and by post. Twelve (12) complaints relating to profiteering in terms of Section 171 of the CGST Act, 2017 were forwarded to the respective Screening Committees/ Standing Committee for further action/examination thereof. Nineteen (19) complaints that related to other GST/enforcement issues were forwarded to the Jurisdictional State & Central GST Commissioners/ Chief Commissioners for necessary action.

- Accordingly, the Performance Report of Competition Commission of India (CCI) for month of December, 2022 and for the 4th quarter of the F.Y 2022-23 along with Performance Reports of SLSC, SC and DGAP on Anti-Profiteering for 3rd quarter and 4th quarter of the F.Y 2022-23 are placed before the GST Council for information.

*****