Central Tax Circulars

CGST Circular 195/2023

| Title | Clarification on availability of ITC in respect of warranty replacement of parts and repair services during warranty period |

| Number | 195/2023 |

| Date | 17.07.2023 |

| Download |

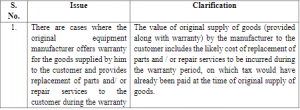

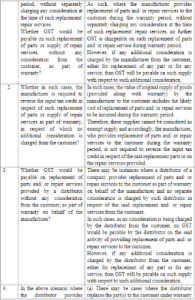

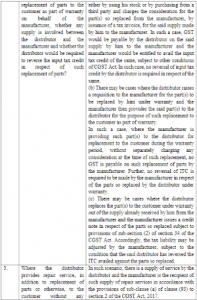

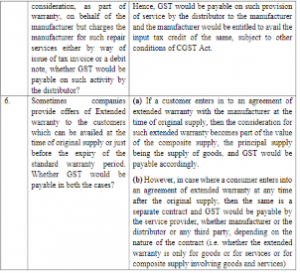

Representations have been received from trade and industry that as a common trade practice, the original equipment manufacturers /suppliers offer warranty for the goods / services supplied by them. During the warranty period, replacement goods /services are supplied to customers free of charge and as such no separate consideration is charged and received at the time of replacement. It has been represented that suitable clarification may be issued in the matter as unnecessary litigation is being caused due to contrary interpretations by the investigation wings and field formations in respect of GST liability as well as liability to reverse ITC against such supplies of replacement of parts and repair services during the warranty period without any consideration from the customers.

2. The matter has been examined. In order to ensure uniformity in the implementation of the provisions of the law across the field formations, the Board, in exercise of its powers conferred under section 168 (1) of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the CGST Act), hereby clarifies as follows:

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

4. Difficulty, if any, in implementation of this Circular may please be brought to the notice of the Board. Hindi version would follow.