CGST Circular 192/2023

| Title | Clarification on charging of interest under section 50(3) of the CGST Act, 2017, in cases of wrong availment of IGST credit and reversal thereof. |

| Number | 192/2023 |

| Date | 17.07.2023 |

| Download |

Reference have been received from trade requesting for clarification regarding charging of interest under sub-section (3) of section 50 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the “CGST Act”) in the cases where IGST credit has been wrongly availed by a registered person. Clarification is being sought as to whether such wrongly availed IGST credit would be considered to have been utilized for the purpose of charging of interest under sub-section (3) of section 50 of CGST Act, read with rule 88B of Central Goods and Services Tax Rules, 2017 (hereinafter referred to as the “CGST Rules”), in cases where though the available balance of IGST credit in the electronic credit ledger of the said registered person falls below the amount of such wrongly availed IGST credit, the total balance of input tax credit in the electronic credit ledger of the registered person under the heads of IGST, CGST and SGST taken together remains more than such wrongly availed IGST credit, at all times, till the time of reversal of the said wrongly availed IGST credit.

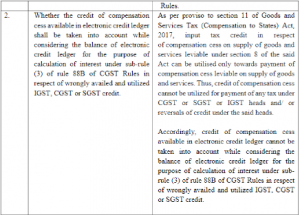

2. Issue has been examined and to ensure uniformity in the implementation of the provisions of law across the field formations, the Board, in exercise of its powers conferred by section 168 (1) of the CGST Act, hereby clarifies the issues as under:

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

4. Difficulty, if any, in implementation of this Circular may please be brought to the notice of the Board. Hindi version would follow.