[FORM GST ASMT – 13

[See rule 100(1)]

Reference No.: Date:

To

_______________ (GSTIN/ID)

_______________ Name

_______________ (Address)

Tax Period: F.Y.: Return Type:

Notice Reference No.: Date:

Act/Rules Provisions:

(Assessment order under Section 62)

Preamble – << standard>>

The notice referred to above was issued to you under section 46 of the Act for failure to furnish the return for the said tax period. From the records available with the department, it has been noticed that you have not furnished the said return till date.

Therefore, on the basis of information available with the department, the amount assessed and payable by you is as under:

Introduction:

Submissions, if any:

Discussion and Findings:

Conclusion:

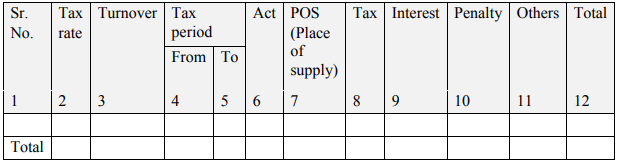

Amount assessed and payable (Details at Annexure):

(Amount in Rs.)

Please note that interest has been calculated up to the date of passing the order. While making payment, interest for the period between the date of order and the date of payment shall also be worked out and paid along with dues stated in the order.

You are also informed that if you furnish the return within a period of 30 days from the date of service of this order, the order shall be deemed to have been withdrawn; otherwise, proceedings shall be initiated against you, after the aforesaid period, to recover the outstanding dues.

Signature

Name

Designation

Jurisdiction

Address

Note –

- Only applicable fields may be filled up.

- Column nos. 2, 3, 4 and 5 of the above Table i. e. tax rate, turnover and tax period are not mandatory.

- Place of Supply (POS) details shall be required only if demand is created under IGST Act.]1