[FORM-GST-RFD-01A

[See rules 89(1) and 97A]

Application for Refund (Manual)

(Applicable for casual taxable person or non-resident taxable person, tax deductor, tax collector and other registered taxable person)

![]()

Annexure-1

Statement – 1 [rule 89(5)]

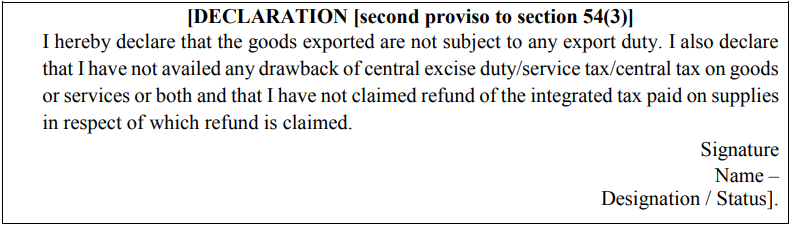

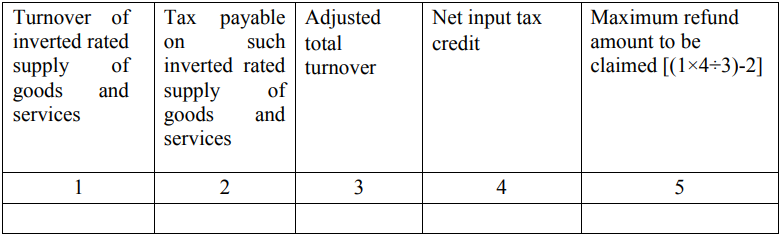

Refund Type: ITC accumulated due to inverted due to inverted tax structure [clause (ii) of first proviso to section 54(3)]

(Amount in Rs.)

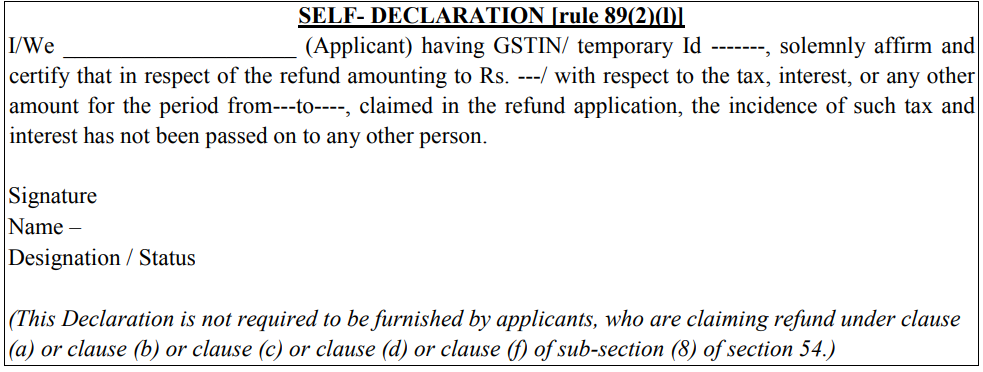

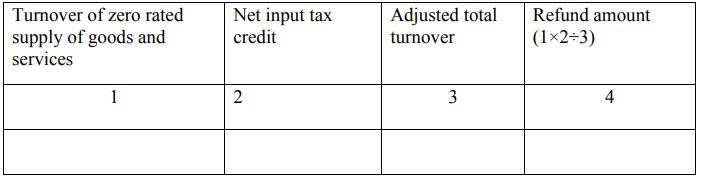

Statement 1A [rule 89(2) (h)]

Refund Type: accumulated due to inverted tax structure [clause (ii) of first proviso to section 54(3)]

* In case of imports or supplies received under reverse charge mechanism [sub-section (3) of section 9 of the CGST Act/SGST Act or sub-section (3) of section 5 of IGST Act], the GSTIN of supplier will mean GSTIN of applicant (recipient).

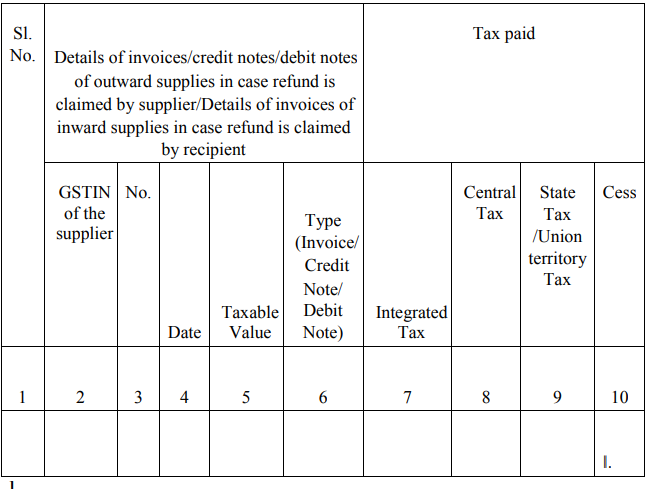

Statement-2 [rule 89(2) (c)]

Refund Type: Exports of services with payment of tax.

(Amount in Rs.)

Statement- 3 [rule 89(2)(b) and 89(2)(c)

Refund Type: Export without payment of tax (accumulated ITC)

(Amount in Rs.)

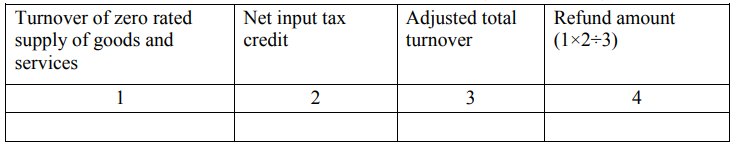

Statement-3A [rule 89(4)]

Refund Type: Export without payment of tax (accumulated ITC) – calculation of refund amount

(Amount in Rs.)

Statement-4 [rule 89(2) (d) and 89(2)(e)]

Refund Type: On account of supplies made to SEZ unit or SEZ Developer (on payment of tax)

(Amount in Rs.)

Statement-5A [rule 89(4)]

Refund Type: On account of supplies made to SEZ unit/ SEZ developer without payment of tax (accumulated ITC) – calculation of refund amount

(Amount in Rs.)

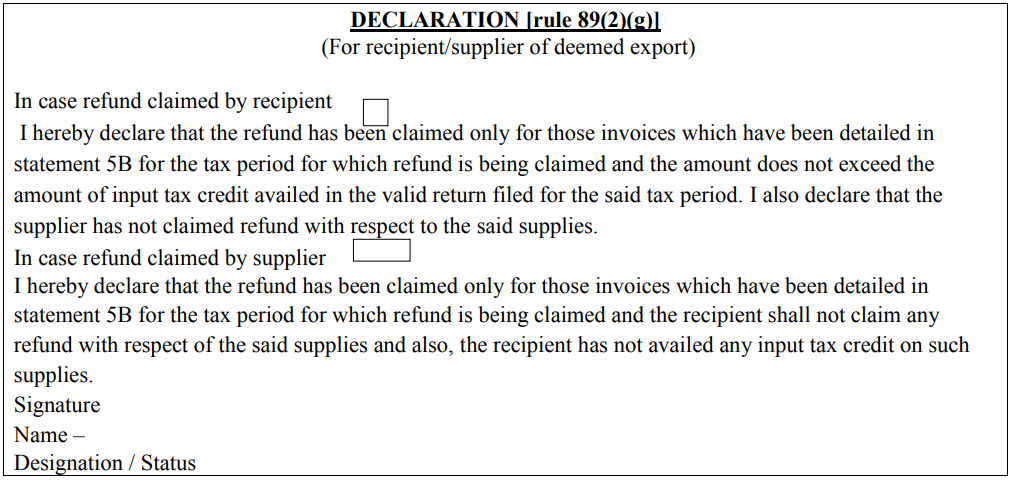

3[Statement 5B [rule 89(2) (g)]

Refund Type: On account of deemed exports

(Amount in Rs)

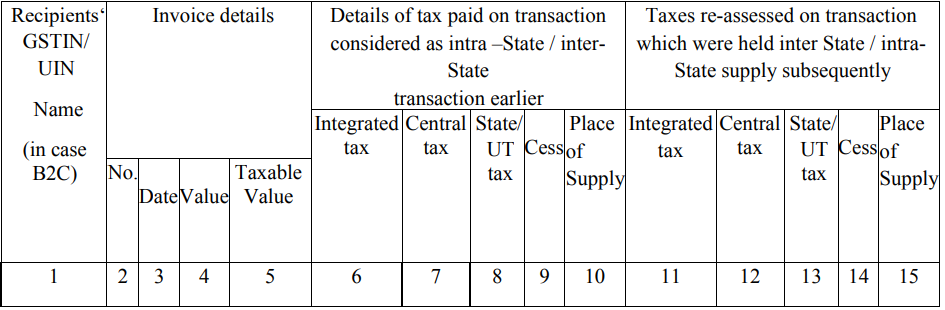

Statement-6 [rule 89(2) (j)]

refund Type: On account of change in POS (inter-State to intra-State and vice versa)

Order Details (issued in pursuance of sections 77(1) and 77(2), if any:

Order No: Order Date:

(Amount in Rs.)

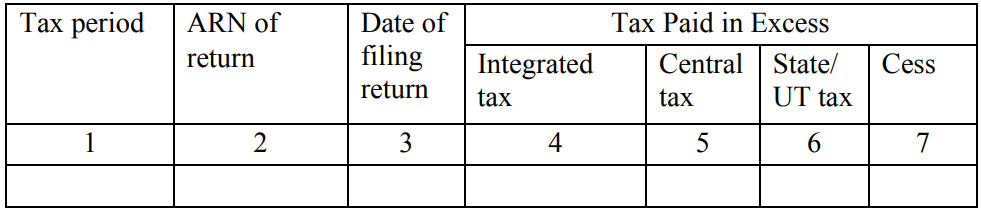

Statement-7 [rule 89(2) (k)]

Refund Type: Excess payment of tax, if any in case of last return filed.

(Amount in Rs.)

1. Substituted vide Notification No. 74/2018-CT dated 31.12.2018.

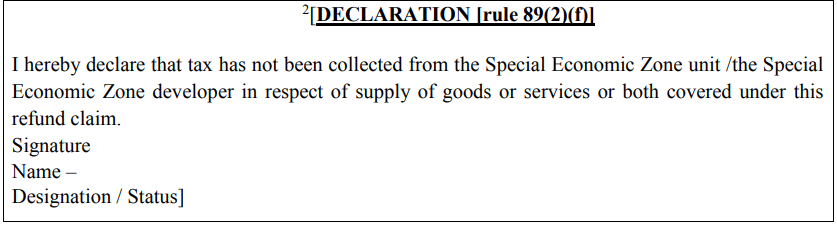

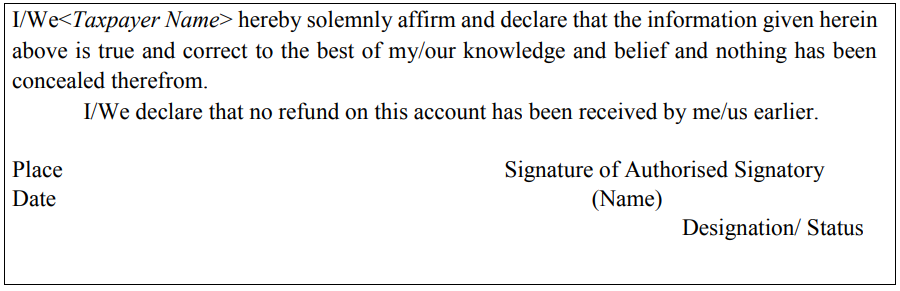

2. Substituted vide notification No. 03/2019-CT dated 29.01.2019 w. e. f. 01.02.2019. Before substitution it was “I hereby declare that the Special Economic Zone unit/the Special Economic Zone developer has not availed of the input tax credit of the tax paid by the application covered under this refund claim.”

3. Substituted vide Notification no. 33/2019-CT dated 18.07.2019.