CGST Rules – Central Goods and Services Tax Rules, 2017

Rule 7 – Rate of tax of the composition levy

This rule was made and amended vide the following notifications • Central Tax Notification No. 03/2019 (dated 29th January 2019)

The category of registered persons, eligible for composition levy under section 10 and the provisions of this Chapter, specified in column (2) of the Table below shall pay tax under section 10 at the rate specified in column (3) of the said Table:-

Sl. No.

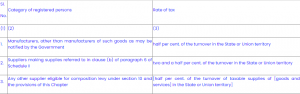

Category of registered persons Rate of tax

1

2

3

1

Manufacturers, other than manufacturers of such 1goods goods and services as may be notified by the Government half per cent. of the turnover in the State or Union territory

2

Suppliers making supplies referred

to in clause (b) of paragraph 6 of Schedule II

two and a half per cent. of the

turnover in the State or Union territory

3

Any other supplier eligible for

composition levy under section 10 and the provisions of

this Chapter

half per cent. of the turnover of

taxable supplies of goods and services in the State or Union territory

| Sl.No. | Section under which composition levy is opted | Category of registered persons | Rate of tax |

|---|---|---|---|

| (1) | (1A) | (2) | (3) |

| 1. | Sub-sections (1) and (2) of section 10 | Manufacturers, other than manufacturers of such goods as may be notified by the Government | half per cent. of the turnover in the State or Union territory |

| 2. | Sub-sections (1) and (2) of section 10 | Suppliers making supplies referred to in clause (b) of paragraph 6 of Schedule II | two and a half per cent. of the turnover in the State or Union territory |

| 3. | Sub-sections (1) and (2) of section 10 | Any other supplier eligible for composition levy under sub-sections (1) and (2) of section 10 | half per cent. of the turnover of taxable supplies of goods and services in the State or Union territory |

| 4. | Sub-section (2A) of section 10 | Registered persons not eligible under the composition levy under subsections (1) and (2), but eligible to opt to pay tax under sub-section (2A), of section 10 | three per cent. of the 2[turnover of] taxable supplies of goods and services in the State or Union territory. |

1 Substituted in Central Goods and Services Tax (Amendment) Rules, 2017, vide Notification No. 03/2019 Central Tax (dated 29th January 2019)

1. Substituted (w. e. f. 01.04.2020) vide Notification No. 50/2020-CT dated. 24.06.2020 for

2. Substituted by Corrigendum G.S.R. 412(E), dated 25.06.2020.