Agenda for 51st GST Council Meeting

2nd August 2023

GST Council Secretariat New Delhi

OFFICE MEMORANDUM

Subject: Notice for the 51st Meeting of the GST Council scheduled to be held on 2nd August, 2023.

The undersigned is directed to refer to the subject stated above and to convey that the 51st Meeting of the GST Council will be held on 2nd August, 2023 through online mode (video conferencing). The schedule of the Meeting is as follows:

• Wednesday, 2nd August, 2023 : 4:00 P.M. onwards

2. In addition, an Officers’ Meeting will be held on 1st August, 2023 through online mode (video conferencing) as per the following schedule:

• Tuesday, 1st August, 2023 : 4:00 P.M. onwards

3. The agenda items and other details for the 51st Meeting of the GST Council will be communicated in due course of time.

4. Kindly convey the invitation to Hon’ ble Member of the GST Council to attend the 51st Meeting of the GST Council.

Sd/-

(Sanjay Malhotra)

Secretary to the Govt. of India and ex-officio Secretary to the GST Council

Tel: 011 23092653

Copy to:

1. PS to the Hon’ble Minister of Finance, Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

2. PS to the Hon’ble Minister of State (Finance), Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

3. The Chief Secretaries of all the State Governments, Union Territories of Delhi, Puducherry and Jammu and Kashmir with the request to intimate the Minister in charge of Finance/Taxation or any other Minister nominated by the State Government as a Member of the GST Council about the above said meeting.

4. Chairman, CBIC, North Block, New Delhi, as a permanent invitee to the proceeding of the Council.

5. Chairman, GST Network.

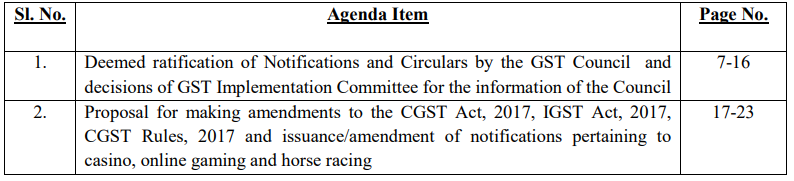

TABLE OF CONTENTS

Agenda Item 1: Deemed ratification of Notifications and Circulars by the GST Council

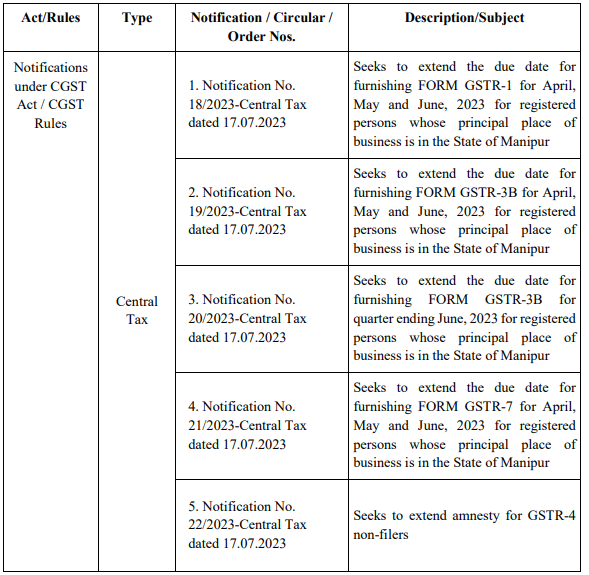

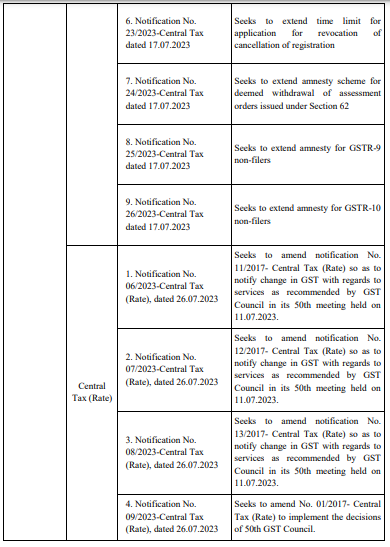

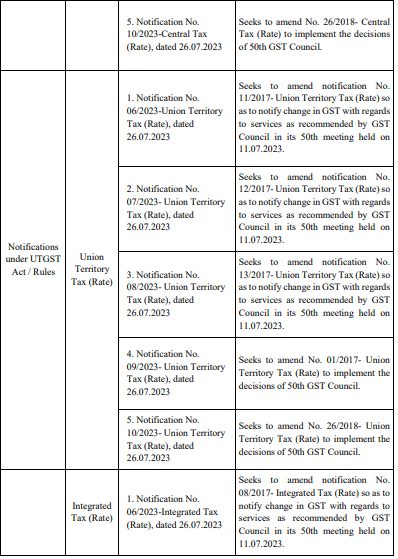

In the 22nd meeting of the GST Council held at New Delhi on 6thOctober, 2017, it was decided that the notifications, circulars and orders, which are being issued by the Central Government with the approval of the competent authority, shall be forwarded to the GST Council Secretariat, through email, for information and deemed ratification by the GST Council. Accordingly, in the 50th meeting held on 11th July, 2023, the GST Council had ratified all the notifications, circulars, and orders issued up to 30.06.2023.

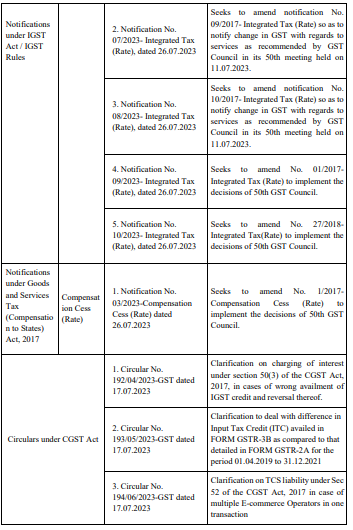

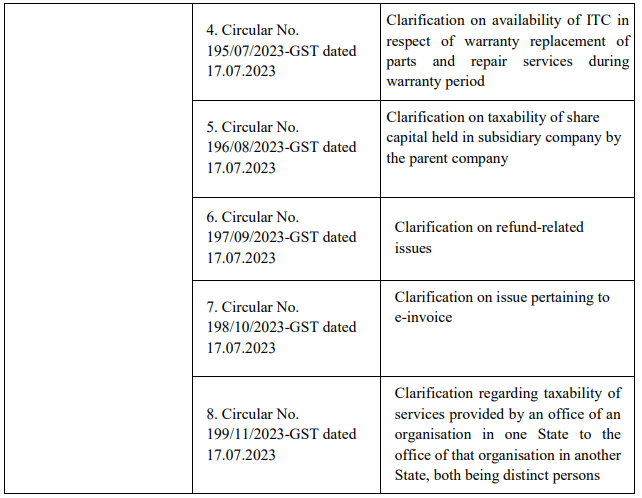

2. In this respect, the following notifications and circulars issued after 30.06.2023 till 26.07.2023 under the GST laws by the Central Government, as available on www.cbic.gov.in, are placed before the Council for information and ratification: –

3. It is mentioned that some of the notifications referred in Para 2 above have been issued as per the recommnedations of GST Impementation Committee (GIC). Details of the same are given in Annexure enclosed with this agenda note. The details of such decisions and the relevant Notifications and Circulars issued to implement such decisions are enclosed as Annexure 2A to this Agenda Note.

4. The GST Council may grant ratification to the notifications and circulars as detailed in para 2 above.

Annexure-2A

Decisions of GST Implementation Committee (GIC) for information of the GST Council

1. The GST implementation Committee (GIC) took three decisions before the 50th GST Council meeting which could not be placed before the Council as these decisions got approved after release of the agenda and therefore, they are placed before the Council for information. The details of the decisions taken are given below:

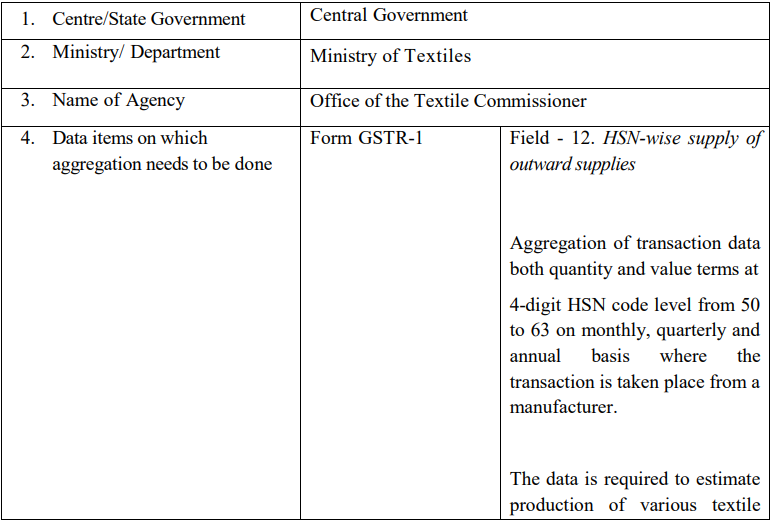

1. Decision of GIC by Circulation on 26th April, 2023 on GST Data sharing request by Ministry of Textiles

a. In the agenda note received from Department of Revenue, it was mentioned that Ministry of Textiles would hold deliberations to make recommendations on policy and other issues pertaining to entire cotton value chain. Since availability of statistics regarding inputs, intermediaries and outputs in the Textile Value Chain is a critical input for policy making, it has been proposed to consider data from GST portal considering the significant formalization of value chain participants in Tax matters.

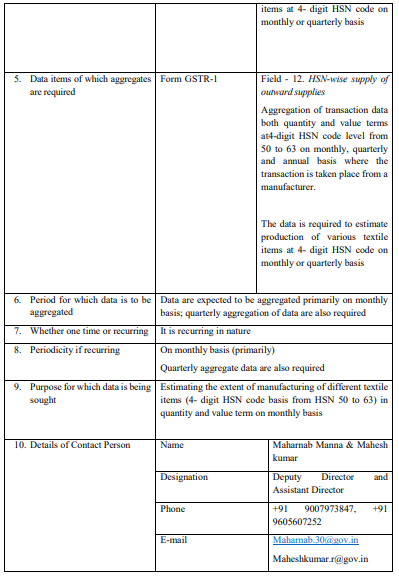

b. Further, Ministry of Textiles had stated that based on meetings held with Chief Commissioner of GST, Mumbai and GSTN, New Delhi, the latter has informed that the requisite data could be provided periodically either monthly or quarterly based on directions received from Department of Revenue. The format in which data is required by Ministry of Textiles is as below:

c. It was further stated that a constraint has, however, been noted for providing the requisite GST data to Ministry of Textiles. Since the data of aggregates of Table 12 of GSTR 1 pertains to gross outward supplies, there will be double counting in the total output as the same product being sold multiple times in the chain will be counted that many times.

d. Further, it was stated in the agenda note that GST Council in its 48th meeting has already approved the GST data sharing with other Ministries/ Departments. It has also been clarified that the Ministry of Textiles and Office of Textile Commissioner would only be the repository of data made available by the Council and that it will not be shared outside the Ministry/Department. Accordingly, approval of GIC was sought for sharing of GST data with Ministry of Textiles.

e. Decision: The Members of GIC approved the above proposal regarding GST data sharing with Ministry of Textiles.

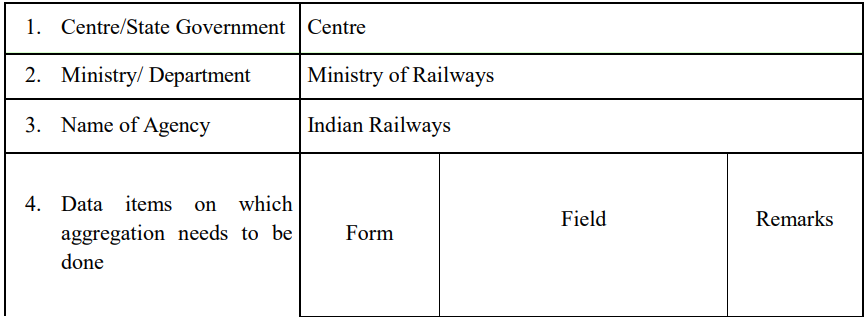

2. Decision of GIC by Circulation on 28th June, 2023 on GST Data sharing with Ministry of Railways

a. In the agenda note, it was mentioned that the request has been received from Ministry of Railways in the approved format wherein it has been mentioned that despite a railway network of 65000km, the modal share of Railways in freight is only 27%. Through e-way bill data, Railways will be able to plan aggregation and offer services to enable improving its modal share to 45% by encouraging shift of road to Railways. This will lead to saving in fuel and reduction in carbon emission which is a National priority.

b. It has been further stated that the data will serve as a key point for Railways to address the issues of network congestion and demand optimization and would be in line with the Hon’ble Prime Minister’s Gati Shakti Mission which seeks to bring about the comprehensiveness, optimization and synchronization among ministries for better coordination infrastructure planning and execution. It has also been stated that it will be ensured that data is not shared with anyone without the consent of Ministry of Finance. The format for sharing of data is as below:

c. It was further mentioned in the agenda note that the GST Council in its 48th Meeting held on 17th December, 2022 had already approved the policy for GST data sharing with other Ministries/Departments.

d. Decision: The Members of GIC approved the above proposal regarding GST data sharing with Ministry of Railways.

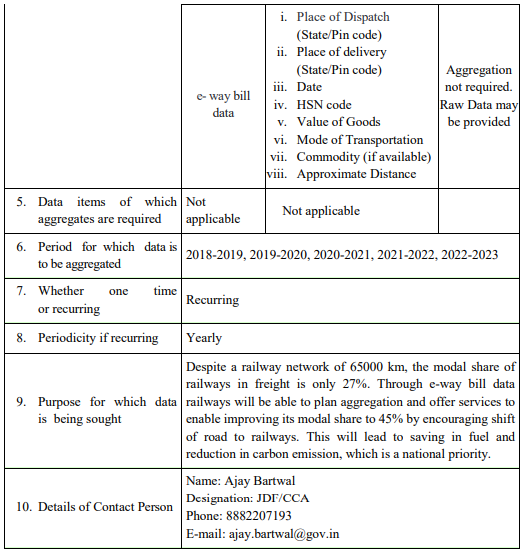

3. Decision of GIC by Circulation on 06th July, 2023 on Sharing of GSTN data with National Statistics Commission, Ministry of Statistics and Programme Implementation

a. In the agenda note received from Department of Revenue, it was mentioned that the request was received for sharing of GSTN data with National Statistics Commission, M/o Statistics and Programme Implementation wherein was mentioned that the following data from e-Way bill is required:

b. It was further mentioned in the agenda note that it may be noted that the GST Council in its 48th Meeting has already approved the GST data sharing with other Ministries/Departments.

c. Decision: The Members of GIC approved the above proposal regarding GST data sharing with National Statistics Commission, Ministry of Statistics and Programme Implementation

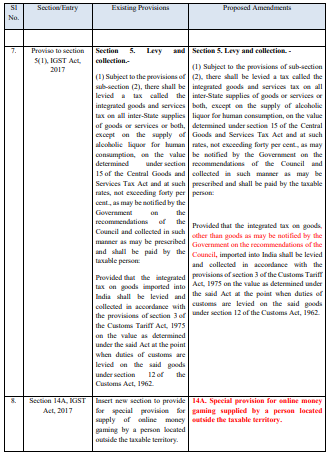

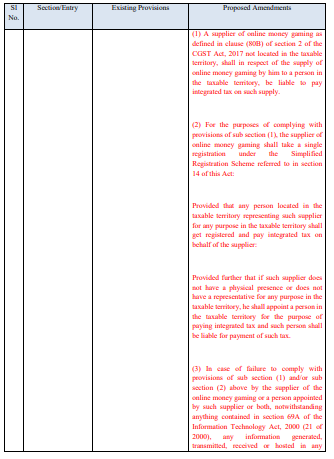

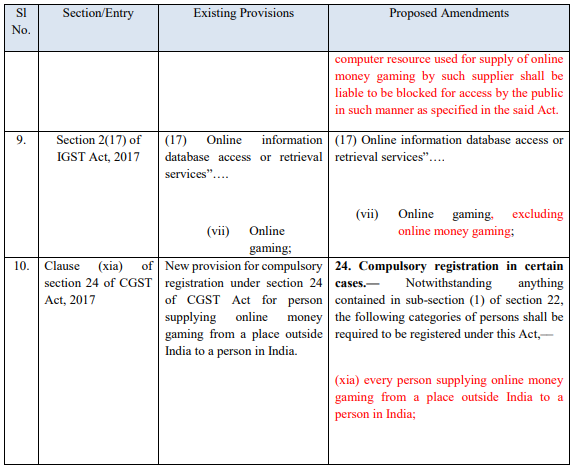

Agenda Item 2: Proposal for making amendments to the CGST Act, 2017, IGST Act, 2017, CGST Rules, 2017 and issuance/amendment of notifications pertaining to casino, online gaming and horse racing.

The GST Council in the 50th meeting held on 11.07.2023, deliberated on the Agenda Item No. 5 i.e. Second Report of the Group of Ministers (GoM) on Casinos, Race Courses and Online Gaming. The Council recommended that the actionable claims supplied in Casinos, Race course and Online gaming to be taxed at the rate of 28% on full face value irrespective of whether the activities are a game of skill or chance and accordingly, the law may be amended to provide clarity on the matter.

2. Accordingly, a proposal for draft amendments in the CGST/IGST Acts was prepared and placed before the Law Committee. Law Committee in its meeting dated 21.07.2023 and 27.07.2023 deliberated on the said proposal and recommended the following amendments in CGST Act 2017, IGST Act 2017 and CGST Rules 2017 as well as issuance of notifications/ amendment in notification as below:

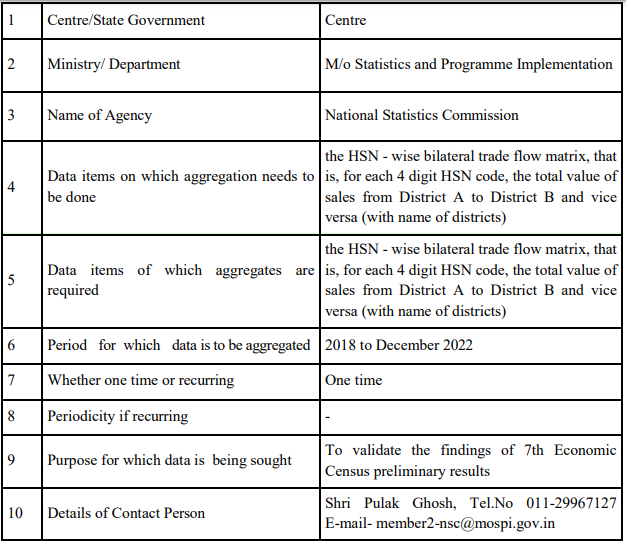

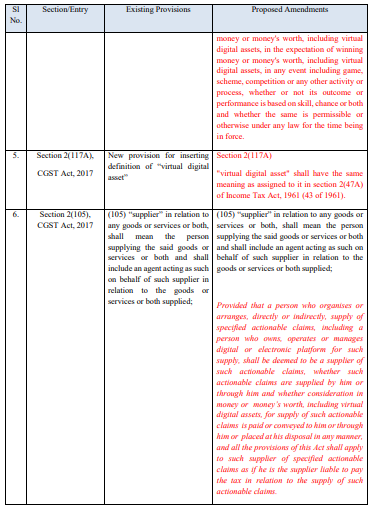

A. Amendments in CGST Act 2017 & IGST Act 2017

Peri Materia amendments will also be required to be made in SGST Act of various States.

Besides, specified actionable claims, as defined under the proposed section 2(102A) of CGST Act, will be required to be notified under the proposed amended proviso to section 5(1) of IGST Act.

B. Issuance of notification under section 15(5) of CGST Act 2017

Section 15(5) of CGST Act, 2017 provides that notwithstanding anything contained in section 15(1) and 15(4) of CGST Act, 2017, the value of such supplies, as may be notified by the Government on the recommendations of the Council, shall be determined in such manner as may be prescribed.

Law Committee recommended to notify supply of online money gaming, supply of online gaming other than online money gaming and supply of actionable claims in casinos under section 15(5) of CGST Act 2017 for prescribing the manner of determination of the value of these supplies through CGST Rules, 2017. The draft notification recommended by the Law Committee is as under:

Draft Notification

G.S.R. (E):— In exercise of powers conferred under sub-section (5) of section 15 of the Central Goods and Services Tax Act, 2017, the Government, on the recommendations of the Council, notifies the following supplies under the said sub-section:

(i) Supply of online money gaming; (ii) Supply of online gaming, other than online money gaming; and (iii) Supply of actionable claims in casinos

C. Amendment in CGST Rules, 2017

Law Committee recommended insertion of rule 31B and rule 31C in CGST Rules 2017 for prescribing the manner of determination of the value of supply in case of online gaming and the value of supply of actionable claims in case of casino respectively, as under:

Value of supply in case of online gaming Rule 31B.Notwithstanding anything contained in this chapter, the value of supply of online gaming (including supply of actionable claims involved in online money gaming) shall be the total amount paid to or deposited with the supplier by way of money or money’s worth, including virtual digital assets, by or on behalf of the player.

Value of supply of actionable claims in case of casino Rule 31C. Notwithstanding anything contained in this chapter, the value of supply of actionable claims in casino shall be the total amount paid by or on behalf of the player for purchase of the tokens, chips, coins or tickets, by whatever name called, for use in casino.

D. Amendment in Notification No. 66/2017-Central Tax dated 15.11.2017 to exclude specified actionable claims

Notification No. 66/2017-Central Tax dated 15.11.2017 was issued to exempt all registered persons from the requirement of payment of tax at the time of receipt of advances in case of supply of goods and to provide for payment of tax in such cases at the time of supply as specified in Section 12(2)(a) of CGST Act. Law Committee recommended amendment in Notification No. 66/2017-Central Tax dated 15.11.2017 to exclude registered persons making supply of specified actionable claims as defined in proposed clause (102A) of section 2 of the CGST Act from the said exemption, so that in case of specified actionable claims, the tax may be required to be paid at the time of receipt of payment for such supplies by the suppliers. The amended notification recommended by the Law Committee is as under:

G.S.R. (E):— In exercise of the powers conferred by section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act) and in supercession of notification No. 40/2017-Central Tax, dated the 13th October, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number

G.S.R.1254(E), dated the 13th October, 2017, except as respects things done or omitted to be done before such supercession, the Central Government, on the recommendations of the Council, hereby notifies the registered person who did not opt for the composition levy under section 10 of the said Act, other than the registered person making supply of specified actionable claims as defined in clause (102A) of section 2 of the said Act, as the class of persons who shall pay the central tax on the outward supply of goods at the time of supply as specified in clause (a) of sub-section (2) of section 12 of the said Act including in the situations attracting the provisions of section 14 of the said Act, and shall accordingly furnish the details and returns as mentioned in Chapter IX of the said Act and the rules made thereunder and the period prescribed for the payment of tax by such class of registered persons shall be such as specified in the said Act.

3. Accordingly, the agenda is placed before the Council for deliberation and approval.