Agenda for 50th GST Council Meeting 11th July 2023

Volume-III

GST Council Secretariat New Delhi

OFFICE MEMORANDUM

Subject: Notice for the 50th Meeting of the GST Council scheduled to be convened on 11th July, 2023.

The undersigned is directed to refer to the subject stated above and to convey that the 50th Meeting of the GST Council will be held on 11th July, 2023 at New Delhi. The schedule of the Meeting is as follows:

• Tuesday, 11th July, 2023: 11:00 A.M. onwards

2. In addition, an Officers’ Meeting will be held on 10th July, 2023 as per the following schedule:

• Monday, 10th July, 2023: 2: 00 P.M. onwards

3. The agenda items and other details for the 50th Meeting of the GST Council will be communicated in due course of time.

4. Keeping in view the logistical constraints, it is requested that participation from each State/UT may be kept limited to two (02) officers in addition to the Hon’ble Member of the GST Council.

5. Kindly convey the invitation to Hon’ble Member of the GST Council to attend the Meeting of the GST Council.

Sd/- (Sanjay Malhotra) Secretary to the Govt. of India and ex-officio Secretary to the GST Council Tel: 011 23092653

Copy to:

1. PS to the Hon’ble Minister of Finance, Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

2. PS to the Hon’ble Minister of State (Finance), Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting.

3. The Chief Secretaries of all the State Governments, Union Territories of Delhi, Puducherry and Jammu and Kashmir with the request to intimate the Minister in charge of Finance/Taxation or any other Minister nominated by the State Government as a Member of the GST Council about the above said meeting.

4. Chairman, CBIC, North Block, New Delhi, as a permanent invitee to the proceeding of the Council.

5. Chairman, GST Network.

TABLE OF CONTENTS

Agenda Item 3(xi)(a): Pilot Project for biometric-based Aadhaar authentication of registration applicants in Puducherry.

On the recommendations of the GST Council in its 48th meeting held on 17.12.2022, it was decided to conduct a pilot in the state of Gujarat for biometric-based Aadhaar authentication of highrisk registration applicants.

2. To this effect, –

(i) Amendments have been made in rule 8(4A), rule 8(5) and rule 9 have been made in the CGST Rules, 2017 as well as in the Gujarat SGST Rules, as below:

Rule 8(4A) of CGST Rules has been substituted vide notification no. 04/2023-Central Tax dated 31.03.2023 as under:

(4A) Where an applicant, other than a person notified under sub-section (6D) of section 25, opts for authentication of Aadhaar number, he shall, while submitting the application under sub-rule (4), undergo authentication of Aadhaar number and the date of submission of the application in such cases shall be the date of authentication of the Aadhaar number, or fifteen days from the submission of the application in Part B of FORM GST REG-01 under sub-rule (4), whichever is earlier.

Provided that every application made under sub-rule (4) by a person, other than a person notified under sub-section (6D) of section 25, who has opted for authentication of Aadhaar number and is identified on the common portal, based on data analysis and risk parameters, shall be followed by biometricbased Aadhaar authentication and taking photograph of the applicant where the applicant is an individual or of such individuals in relation to the applicant as notified under sub-section (6C) of section 25 where the applicant is not an individual, along with the verification of the original copy of the documents uploaded with the application in FORM GST REG-01 at one of the Facilitation Centres notified by the Commissioner for the purpose of this sub-rule and the application shall be deemed to be complete only after completion of the process laid down under this proviso.

rule 8(5) has been amended vide Notification No. 26/2022-CT dated 26.12.2022 as under: (5) On receipt of an application under sub-rule (4) or sub-rule (4A), as the case maybe, an acknowledgement shall be issued electronically to the applicant in FORM GST REG-02.

rule 9 has been amended vide Notification No. 26/2022-CT dated 26.12.2022 as under

(1) The application shall be forwarded to the proper officer who shall examine the application and the accompanying documents and if the same are found to be in order, approve the grant of registration to the applicant within a period of seven working days from the date of submission of the application:

Provided that where –

(a) a person, other than a person notified under sub-section (6D) of section 25, fails to undergo authentication of Aadhaar number as specified in sub-rule (4A) of rule 8 or does not opt for authentication of Aadhaar number; or

(aa) a person, who has undergone authentication of Aadhaar number as specified in sub-rule (4A) of rule 8, is identified on the common portal, based on data analysis and risk parameters, for carrying out physical verification of places of business; or;

(b) the proper officer, with the approval of an officer authorised by the Commissioner not below the rank of Assistant Commissioner, deems it fit to carry out physical verification of places of business, the registration shall be granted within thirty days of submission of application, after physical verification of the place of business in the presence of the said person, in the manner provided under rule 25 and verification of such documents as the proper officer may deem fit;

(2) Where the application submitted under rule 8 is found to be deficient, either in terms of any information or any document required to be furnished under the said rule, or where the proper officer requires any clarification with regard to any information provided in the application or documents furnished therewith, he may issue a notice to the applicant electronically in FORM GST REG-03 within a period of seven working days from the date of submission of the application and the applicant shall furnish such clarification, information or documents electronically, in FORM GST REG-04, within a period of seven working days from the date of the receipt of such notice.

Provided that where –

(a) a person, other than a person notified under sub-section (6D) of section 25, fails to undergo authentication of Aadhaar number as specified in sub-rule (4A) of rule 8 or does not opt for authentication of Aadhaar number; or

(aa) a person, who has undergone authentication of Aadhaar number as specified in sub-rule (4A) of rule 8, is identified on the common portal, based on data analysis and risk parameters, for carrying out physical verification of places of business; or

(b) the proper officer, with the approval of an officer authorised by the Commissioner not below the rank of Assistant Commissioner, deems it fit to carry out physical verification of places of business, the notice in FORM GST REG-03 may be issued not later than thirty days from the date of submission of the application.

…”

However, the said amendments have not been made in the SGST / UTGST Rules of other states/ UTs at present.

(ii) Further, rule 8(4B) has been introduced in CGST Rules only. Subsequently, Notification No. 27/2022-CT dated 26.12.2022 has been issued by the Centre under rule 8(4B) for specifying all states and UTs, except Gujarat, where provisions of rule 8(4A) will not apply.

3.1 Department of Revenue vide their email dated 27.06.2023 has informed that Puducherry has communicated their willingness to conduct pilot for biometric authentication of Aadhaar for high-risk registration applicants in their State also. In order to implement the said biometric-based Aadhaar authentication for registration applicants in Puducherry, the following notifications may be required to be issued:

(i) The State of Puducherry will need to substitute rule 8(4A) of Puducherry SGST Rules on the lines of corresponding substitution of Rule 8(4A) of CGST Rules vide notification no. 04/2023-Central Tax dated 31.03.2023;

(ii) Further, the State of Puducherry will also need to amend rule 8(5) and rule 9 of Puducherry SGST Rules on the lines of corresponding amendments in CGST rules notified vide notification no. 26/2022- CT dated 26.12.2022.

(iii) The Central government may also be required to further amend Notification No. 27/2022-CT dated 26.12.2022 for specifying that the proviso to rule 8(4A) will apply to the State of Puducherry as well.

3.2 Further, it is proposed that the Council may authorize the Chairperson to extend the said pilot project, if required, in other States and/ or Union territories which may be willing to conduct pilot for biometric authentication of Aadhaar for high-risk registration applicants.

4. It is further mentioned that the above amendments in sub-rule (5) of rule 8 and sub-rule (1) and

(2) of rule 9 of CGST Rules vide Notification No. 26/2022-CT dated 26.12.2022, as detailed in Para 2 above, have been made at present only in Gujarat SGST Rules and in CGST Rules but not in SGST Rules of other states. It is proposed to notify the said amendments in sub-rule (5) of rule 8 and sub-rule (1) and (2) of rule 9 in the SGST Rules of the remaining States as well to provide for enabling clause for mandatory physical verification of an applicant who has undergone authentication of Aadhaar and is identified on the common portal based on data analysis and risk parameters.

5. Therefore, the proposals at para 3.1, 3.2 and 4 are placed before the Council for approval

Agenda Item 3(xv): Goods and Services Tax Appellate Tribunal Appointment and Conditions of Service of President and Members) Rules, 2019

In 49th GST Council meeting held on 17th 18th February, 2023, the recommendation of the Group of Ministers (GoM) on the constitution of Goods and Services Tax Appellate Tribunal (GSTAT) was accepted by the Council. Accordingly, the law amendments in CGST Act, 2017 relating to the constitution of GST Appellate Tribunal have been incorporated through Finance Act, 2023 (vide clause 149 to154 of the Finance Act, 2023), by substitution of sections 109, 110 and 114 of CGST Act and by amending sections 117, 118 and 119 of CGST Act.

2. The said provisions of Finance Act, 2023 will be notified in due course in coordination with the states and Union territories once necessary amendments are made in the respective State/ UTGST Acts.

3. Meanwhile, it is proposed that Rules governing appointment and conditions of President and Members of the proposed GST Tribunal may be formulated for enabling smooth constitution and functioning of GST Tribunal. The said Rules may be notified after notification of the above provisions of the Finance Act, 2023.

3.1 The said issue was deliberated by the Law Committee in its meeting held on 31.05.2023. The Law Committee recommended the issuance of GSTAT (Appointment and Conditions of Service of President and Members) Rules, 2023. The draft GSTAT (Appointment and Conditions of Service of President and Members) Rules, 2023 as recommended by the Law Committee are enclosed as Annexure-A of this agenda note.

4. Accordingly, the same is placed before GST Council for deliberation and approval please.

Annexure-A

Draft Rules as per Finance Act, 2023

MINISTRY OF FINANCE

(Department of Revenue)NOTIFICATION

G.S.R. (E).— In exercise of the powers conferred by section 110 of the Central Goods And Services Tax Act, 2017 (12 of 2017) read with section 164 of the said Act, the Central Government, in super session of the Goods and Services Tax Appellate Tribunal (Appointment and Conditions of Service of President and Members) Rules, 2019, hereby makes the following rules, namely:-

CHAPTER I PRELIMINARY

1. Short title, commencement and application.—

(1) These rules may be called the Goods and Services Tax Appellate Tribunal (Appointment and Conditions of Service of President and Members) Rules, 2023.

(2) Save as provided in these rules, they shall come into force on the date of their publication in the Official Gazette.

(3) These rules shall apply to the President, Judicial Member, Technical Member (Centre) and Technical Member (State) of the Principal Bench and State Bench of Goods and Services Tax Appellate Tribunal.

2. Definitions.

In these rules, unless the context otherwise requires, —

(a) “Act” means the Central Goods And Services Tax Act, 2017 (12 of 2017);

(b) “Committee” means the Search-cum-Selection Committee constituted under clause (a) of sub-section 4 of section 110 of the Act for Technical Member (State) of the State Bench or the Search-cum-Selection Committee constituted under clause (b) of sub-section 4 of section 110 of the Act for President and other Members.

(c) “Form” means a Form appended to these rules;

(d) “Member” means a Technical Member (Centre) or Technical Member (State) or Judicial Member of the Goods and Services Tax Appellate Tribunal;

(e) “section” means a section of the Act;

(f) “Tribunal” means Goods and Services Tax Appellate Tribunal as established under section 109 of the Act.

CHAPTER II APPOINTMENT OF PRESIDENT AND MEMBER

3. Selection for posts of President and Members—

(1) The Committee shall determine its own procedure for making recommendation.

(2) The Committee may cause a vacancy circular to be issued through the Member Secretary, giving details of the posts of Members proposed to be filled up, including the following—

a. number of existing and anticipated vacancies;

b. qualifications;

c. salary and allowances;

d. format for application; and

e. last date for filing of applications,

in Form-I after making such modifications as may be deemed fit by the Committee.

(3) The Committee shall scrutinise, or cause to be scrutinised, every application received in response to the circular, against the qualifications and may shortlist such number of eligible candidates for personal interaction as it may deem fit.

(4) For the post of President, the Committee may, either cause a vacancy circular to be issued and call for applications or search for suitable persons eligible for appointment and make an assessment for selection to the post ofPresident.

(5) The Committee shall make its recommendations based on the overall assessment of eligible candidates including assessment through the personal interaction after taking into account the suitability, record of past performance, integrity as well as adjudicating experience keeping in view the requirements of the Tribunal and shall recommend a panel of two names for every post for which selection is being done in accordance with the provisions ofsub – section (6) of section 110 of the Act.

4. Selection for re – appointment.— (1) An application for re-appointment shall be considered in the same manner as that for the original appointment, preferably, along with all the persons shortlisted in response to the vacancy circular or otherwise.

(2) While making its assessment for suitability to a post, the Committee shall give additional weightage to the persons seeking re-appointment for their experience in the Tribunal and while doing so, shall take into account, the performance of the person while working as a President or Member in the Tribunal.

5. Medical fitness of President and Members.—

(1) No person shall be appointed as President, Judicial Member or Technical Member (Centre) of the Principal Bench or the State Bench of the Tribunal or as Technical Member (State) of the Principal Bench unless he is declared medically fit by an authority specified by the Central Government in this behalf.

(2) No person shall be appointed as Technical Member (State) of the State Bench of the Tribunal unless he is declared medically fit by an authority specified in this behalf by the State in which the said State Bench is located.

6. Retirement from parent service on appointment as President or Member.— (1) Where, the person appointed as President or Member is a serving Judge of the Supreme Court or a High Court or a serving Member of an organised Service, he shall either resign or obtain voluntary retirement before joining the Tribunal.

CHAPTER III RESIGNATION OR REMOVAL OF PRESIDENT OR MEMBER

7. Resignation.— President or Member may, by writing under his hand addressed to the Central Government, resign from his office at any time:

Provided that the President or Member shall, unless he is permitted by the Central Government to relinquish office sooner, continue to hold office until the expiry of three months from the date of receipt of such notice by the Government oruntil a person duly appointed as his successor enters upon his office or until the expiry of his term of office, whichever is earliest.

8. Procedure for inquiry into complaints.—

(1) Where a written complaint alleging any definite charge of the nature referred to in sub-section (12) of section 110 of the Act in respect of President or Member is received by the Central Government, it shall make a preliminary scrutiny of such complaint.

(2) Where, on preliminary scrutiny, the Central Government is of the opinion that there are reasonable grounds for making an inquiry into the truth of any allegation referred to in sub-rule (1), it shall make a reference to the concerned Committee.

(3) The said Committee shall conduct an inquiry or cause an inquiry to be conducted by a person who is, or has been, a –

(a) Judge of Supreme Court or Chief Justice of a High Court, where the inquiry is against President; or

(b) Judge of a High Court, where the inquiry is against a Member.

(4) The inquiry shall be completed within such time or such further time as may be specified by the Central Government preferably within six months.

(5) After the conclusion of the inquiry, the Committee shall submit its report to the Central Government stating therein its findings and the reasons thereof on each of the charges separately with such observations on the whole case as it may think fit.

(6) The Committee shall not be bound by the procedure laid down by the Code of Civil Procedure,1908 (5 of 1908) but shall be guided by the principles of natural justice and shall have power to regulate its own procedure, including the fixing of date, place and time of its inquiry.

CHAPTER IV SALARY AND ALLOWANCES

9. Salary. — (1) The President of the Tribunal shall, be paid a salary of Rs. two lakh fifty thousand (fixed) per month.

(2) The Member shall be paid a salary of Rs. two lakh twenty- five thousand per month.

(3) In case, a person appointed as the President, or Member, is in receipt of any pension, the pay of such person shall be reduced by the gross amount of pension drawn by him.

10. Allowances.— (1) The President and Members shall be entitled to draw allowances and benefits as areadmissible to a Government of India officer holding Group ‘A’ post carrying the same pay

(2) Notwithstanding anything contained in sub-rule (1), the President or Members shall have option to avail of accommodation to be provided by the Central Government as per the rules for the time being in force or shall be eligible for reimbursement of house rent subject to a limit of –

(a) one lakh fifty thousand rupees per month in case of President of the Tribunal; and

(b) one lakh twenty-five thousand rupees per month in case of Members of the Tribunal.

11. Transport allowance.— The President, or Members shall be entitled to the facility of staff car for journeys for official and private purposes in accordance with the facilities as are admissible to a Government of India officer holding Group ‘A’ post carrying the same pay as per the provisions of Staff Car Rules.

CHAPTER V PENSION, PROVIDENT FUND, GRATUITY AND LEAVE

12. Pension, Provident Fund and Gratuity.— Pension, Provident Fund and gratuity shall not be admissible for the service rendered in the Tribunal.

13. Leave. (1) The President or Member shall be entitled to thirty days of earned leave for every year of service.

(2) Casual Leave not exceeding eight days may be granted to the President or a Member in a calendar year.

(3) The payment of leave salary during leave shall be governed by rule 40 of the Central Civil Services (Leave) Rules, 1972.

(4) The President or Member shall be entitled to encashment of leave in respect of the earned Leave standing to his credit, subject to the condition that maximum leave encashment, including the amount received at the time of retirement from previous service shall not in any case exceed the prescribed limit under the Central Civil Service (Leave) Rules,1972.

(5) Leave sanctioning authority for-

(a) Member, shall be the President;

(b) President or Member in case of absence of President, shall be the Central Government.

(6) The Central Government shall be the sanctioning authority for foreign travel to the President and Members.

CHAPTER VI POWERS OF PRESIDENT AND VICE PRESIDENT

14. Powers of President.- The President shall exercise the powers of Head of the Department for the purpose of:-

(a) Delegation of Financial Power Rules, 1978;

(b) General Financial Rules, 2017; and

(c) Fundamental Rules and Supplementary Rules.

(d) CCS (CCA) Rules, 1965

15. Powers of Vice-President: – The Vice-President shall exercise the powers of the President provided under section 114 of the Act for the relevant State Benches for the purpose of:-

(a) Allocation of appeals amongst members within a bench under his jurisdiction.

(b) Deciding the appeals to be heard by Single Member as per provisions of the Act.

(c) Transfer of appeals amongst the State Benches within his jurisdiction.

(d) Refer cases under clause (a) of sub-section (9) of Section 109 of the Act to a Member in a State Bench within his jurisdiction.

(e) Such other administrative and financial powers as may be assigned by the President by a general or special order.

CHAPTER VII MISCELLANEOUS

16. Declaration of Financial and other Interests.— The President or the Member shall, before entering upon his office, declare his assets, and his liabilities and financial and other interests.

17. Other conditions of service.— (1)The terms and conditions of service of a President or Member with respect to which no express provision has been made in these rules, shall be such as are admissible to a Government of India officer holding Group ‘A’ post carrying the same pay.

(2) The President, or Member shall not undertake any arbitration assignment while functioning in these capacities in the Tribunals.

(3) The President, or Member of the Tribunal, shall not, for a period of two years from the date on which theycease to hold office, accept any employment in, or connected with the management or administration of, any person who has been a party to a proceeding before the Tribunal:

Provided that nothing contained in this rule shall apply to any employment under the Central Government or a State Government or a local authority or in any statutory authority or any corporation established by or under any Central, State or Provincial Act or a Government company as defined in clause (45) of section 2 of the Companies Act, 2013 (18 of 2013).

18. Oath of office and secrecy.— Every person appointed to be the President, or Member shall, before entering upon his office, make and subscribe an oath of office and secrecy in Form II and Form III annexed to these rules.

19. Power to relax:- Where the Central Government is of the opinion that it is necessary or expedient so to do, it may, on the recommendations of the Council, by order and for reasons to be recorded in writing, relax any of the provisions of these rules with respect to any class or category of persons.

20. Interpretation.- If any question arises relating to the interpretation of these rules, the decision of the Central Government thereon, on the recommendations of the Council shall be final.

FORM I

(See rule 3)

[Format for vacancy circular including the format for application]

F. No._.

Government of India

Ministry of ________

Department of ______. Room No.___.

New Delhi-110001

Dated,the ____

*****

Vacancy Circular

Subject: – Selection for the posts of President/Member in ……………………..Tribunal-reg.

*****

1. Tribunal: – The Goods and Services Tax Appellate Tribunal is an Appellate Authority established under ______________ the Central Goods And Services Tax Act, 2017 to hear various appeals under the ________ Act, ___.Principal Bench is situated at New Delhi ____________________ and its state Benches are situated at _________________.A Member, upon selection, may be posted at any of these places.

2. Vacancy: – Applications are being invited for the following existing and________ anticipated vacancies:

3. Qualification:- The qualifications, eligibility, salary and other terms and conditions of the appointment of a candidate will be governed by the provisions of the of Central Goods And Services Tax Act, 2017 and Goods and Services Tax Appellate Tribunal (Appointment and Conditions of Service of President and Members) Rules, 2023.

4. Procedure for selection: – The Search-Cum-Selection Committee constituted under the clause (a) of sub-section 4 of section 110 for the posts of Technical Member (State) of the State Bench and under clause (b) of sub-section (4) of the said section of Central Goods And Services Tax Act, 2017 for the posts of President and other Members shall recommend names for appointment to the said post/s and shall scrutinise the applications with respect to suitability of application for the posts by giving due weightage to qualification and experience of candidates and shortlist candidates for conducting personal interaction. The final selection will be done on the basis of overall evaluation of candidates done by the Committee based on the qualification, experience and personal interaction.

5. Application Procedure:- Applications by eligible and willing officers are to be submitted through proper channel(wherever applicable) and should be accompanied with (i) bio-data in the proforma at Annexure-I (ii) Certificate to be furnished by the employer/ head of office/ forwarding authority as in Annexure-II (iii) clear photocopies of the up-to-date CR/APAR dossier of the officer containing CR/APARs of at least last five years duly attested by a Group A officer (iv) cadre clearance (v) integrity certificate/clearance from vigilance and disciplinary angle as in Annexure-III (vi) statement giving details of major or minor penalties, if any, imposed on the officer during the last ten years, to the following address, so as to reach this office latest by ________:-

[Name and Address]

Applicants can Log on to https://. to access the home page of the Online Application to apply (wherever applicable).

6. No TA/DA will be admissible to the candidates to be called for interview/interaction. The candidates are required to make own arrangements.

7. Advertisement and Prescribed application form can be downloaded from Ministry’s/Tribunals website (name of the website).

8. Any application received after due date or without necessary Annexure as mentioned above will not be entertained.

Wide publicity may be given in all organizations and their field formations to facilitate early and optimum number of application.

(Name of the Signing Officer) Under Secretary to the Govt. of India/Director

Annexure-I

PROFORMA

1. Name :

2. Date of Birth :

3. Category (SC/ST/OBC/UR) :

4. Designation/Profession :

5. Contact Details :

6. Cadre/Service [Wherever applicable] :

7. Educational qualification (in reverse chronological order):

8. Work Experience:

8 A. For the experience as employee, Employment record in chronological order starting with present Employment, list in reverse:

(a) For the post of Technical Member (Centre) and Technical Member (State) .

* Please specify whether the said work involves administration of an existing law (as defined in clause (48) of section (2) of the Central Goods and Services Tax Act, 2017) or the goods and services tax in the Central Government in respect of post of Technical Member (Centre) or whether the work involves administration of an existing law or the goods and services tax or in the field of finance and taxation in the State Government in respect of post of Technical Member (State).

Also specify whether the said works involves judicial/ quasi-judicial functions.

(b) For the post of President and Judicial Member

. Please specify whether the said work involves Judicial or Quasi-Judicial /Criminal/Civil /Taxation /Company Affairs/or any other as may be applicable.

9. Write up on adjudicating experience :

of the applicant (200 words)

[Wherever applicable]

10. Mention :

a. Whether minimum three years of experience is there : (Yes/No. If yes, provide details thereof )

in the administration of an existing law or goods and

services tax in the Central Government for the post of

Technical Member (Centre)

b.Whether minimum three years of experience is there : (Yes/No. If yes, provide details thereof )

in the administration of an existing law or goods and

services tax or in the field of finance and taxation

in the State Government for the post of

Technical Member (State)

c. Any experience in handling such cases involving : (Brief Writeup)

interpretation of goods and services tax law or an

existing law for the posts of Judicial Member

12. Write up on 05, major achievement : (200 words each)

13. Awards/honours/Publications, if any :

14. Affiliation with the professional bodies/ :

Institutions/societies/or any other body

Including political party.

15. Additional information, if any, which :

You would like to mention in support of the application for the post.

DECLARATION

1. I certify that the foregoing information is correct and complete to the best of knowledge and belief and nothing has been concealed/distorted. If at any time I found to have concealed/distorted any material information; my appointment shall be liable to summary termination without notice.

2. I shall not withdraw my candidature after the meeting of the Selection Committee.

3. I shall not decline the appointment, if selected for appointment by the ACC.

4. I shall join within 30 days from the date of issue of order of appointment.

5. I am aware that in case I violate any of the conditions mentioned at SI.No.2 to 4, the Government of India is likely to debar me for a period of three years for consideration for appointment outside the cadre and in any Autonomous Body/Statutory Body/Regulatory Body.

Place : Date:

Signature of the candidate

Annexure- II

CERTIFICATE TO BE FURNISHED BY THE EMPLOYER/HEAD OF OFFICE/FORWARDING AUTHOTITY

1. Certified that the particular furnished by Shri/Smt/Kum are correct and he/she possesses educational qualifications and experience mentioned in Annexure-I.

2. It is also certified that there is no vigilance/ disciplinary case either pending or being contemplated against him/her and vigilance clearance issued by competent Authority in the enclosed Annexure (III).

3. His/her integrity is certified.

4. No major or minor penalty was imposed on Shri/Smt/Kum during the last 10 years period.

5. The up-to-date attested Photostate copies of ACR/APAR of last 5years (each Photostat copy of ACR/APAR should be attested) in respect of Shri/Smt/Kum————————————————– are enclosed herewith.

Seal & Signature of the cadre controlling Authority

Annexure-III

PARTICULARS OF THE OFFICERS FOR WHOM VIGILANCE CLEARANCE IS BEING SOUGHT

(To be furnished and signed by the competent authority or HOD)

1. Name of the Officer (in full) :

2. Father’s name :

3. Date of Birth :

4. Date of Retirement :

5. Date of entry into service

6. Service to which the officer belongs :

including batch /year/ cadre etc. ,

wherever applicable

7. Positions held (During ten preceding years):

8. Whether the officer has been placed on :

the agreed list or list of Officer of

Doubtful Integrity (if yes, details to be given)

9. Whether any allegation of misconduct :

Involving vigilance angle was examined against

the officer during the last 10 Years and if so with what result (*)

10. Whether any punishment was awarded to :

the officer during the last 10 years and if

so, the date of imposition and details of penalty (*)

11. Is any disciplinary/ criminal proceedings :

or charge sheet pending against the

officer as on date (if so, details to be furnished)

12. Is any action contemplated against the :

Officer as on date (if so, details to be furnished (*)

(*) If vigilance clearance had been obtained in the past, the information may be provided for the period thereafter,

Date:

(NAME AND SIGNATURE)

FORM II

(See rule 17)

Form of Oath of Office for President/ Member

I, A. B., having been appointed as President/Member of the Goods and Service Tax Appellate Tribunal, do solemnly affirm/do swear inthe name of God that I will faithfully and conscientiously discharge my duties as the President/ Member of the Appellate Tribunal to the best of my ability, knowledge and judgment, without fear or favour, affection or ill-will.

FORM III

(See rule 17)

Form of Oath of Secrecy for President/Member

I, A. B., having been appointed as the President/Member of the Goods and Service Tax Appellate Tribunal, do solemnly affirm/do swear in the name of God that I will not directly or indirectly communicate or reveal to any person or persons any matter which shall be brought under my consideration or shall become known to me as President/ Member of the Appellate Tribunal except as may be required for the due discharge of my duties as the President/Member.

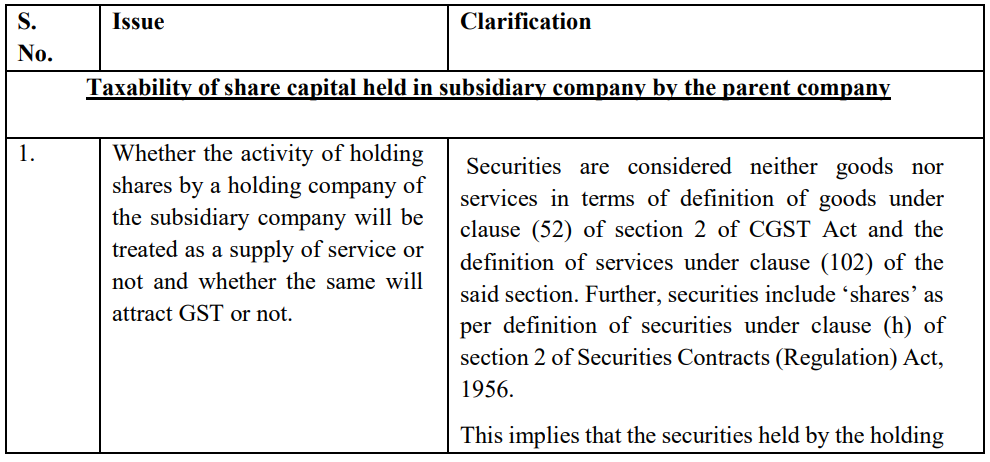

Agenda Item 3(xvi): Seeking clarity on tax ability of share capital held in subsidiary company by the parent company

Representation has been received from trade to clarify whether the holding of shares in a subsidiary company by the parent company will be treated as ‘supply of service’ under GST and will be taxed accordingly or whether such transaction is not a supply.

2. Some of the field formations/ investigative agencies are relying on the SAC code 997171- “services provided by holding companies, i.e. holding securities of (or other equity interests in) companies and enterprises for the purpose of owning a controlling interest”, and are demanding GST on “share capital held in subsidiary company’ under forward charge basis and on ‘share capital held by a foreign holding company’, on reverse charge basis by classifying the said activity as an import of service by invoking residual entry 15 of Notification 11/2017 CGST (rate). They have taken a view that equity capital is to be treated as a financial asset which is in the form of an investment made with a purpose to have control over the subsidiary company. Therefore, it is being claimed that the activity of holding securities is nothing but an investment made by holding company to have control over subsidiary company and therefore, it is a supply of “services of holding securities in subsidiary company” by the holding company to the subsidiary company.

3. Trade, on the other hand, has represented that a subsidiary company is controlled by the holding company by holding equity shares to protect the interests of the parent/ holding company and to regulate the capital infused by them. Such a control is not exercised with an intention to benefit the subsidiary company. It has also been represented that mere controlling interest does not qualify the said activity to be termed as a taxable ‘supply of service’ as per the SAC code 997171 and therefore, merely by holding equity shares in a subsidiary company, the parent company cannot be said to be rendering to the subsidiary company.

4. RELEVANT GST PROVISIONS:

4.1 Various definitions in CGST Act, 2017 to be referred in the Agenda Note are detailed below:

• Section 2(52) ” “goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;”

• Section 2(102) “services” means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged;

[Explanation.- For the removal of doubts, it is hereby clarified that the expression “services” includes facilitating or arranging transactions in securities;]

• “ Section 7. Scope of supply.-

(1) For the purposes of this Act, the expression – “supply” includes-

(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence,rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business,

[(aa) the activities or transactions, by a person, other than an individual, to its members or constituents or vice-versa, for cash, deferred payment or other valuable consideration.

Explanation .- For the purposes of this clause, it is hereby clarified that, notwithstanding anything contained in any other law for the time being in force or any judgment, decree or order of any Court, tribunal or authority, the person and its members or constituents shall be deemed to be two separate persons and the supply of activities or transactions inter se shall be deemed to take place from one such person to another;]

(b) import of services for a consideration whether or not in the course or furtherance of business; and

(c) the activities specified in Schedule I, made or agreed to be made without a consideration;

(d)[****].

[(1A) where certain activities or transactions constitute a supply in accordance with the provisions of sub-section (1), they shall be treated either as supply of goods or supply of services as referred to in Schedule II.]

(2) Notwithstanding anything contained in sub-section (1),-

(a) activities or transactions specified in Schedule III; or

(b) such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council,

shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to the provisions of sub-sections (1), (1A) and (2), the Government may, on the recommendations of the Council, specify, by notification, the transactions that are to be treated as – (a) a supply of goods and not as a supply of services; or (b) a supply of services and not as a supply of goods.”

4.2 Definition of securities under clause (h) of section 2 of Securities Contracts (Regulation) Act, 1956 is as below:

“securities” include— (i) shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate; …………………………………”

4.3 Further, subsidiary company has been defined in sub-section 87 of section 2 of Companies Act, 2013. The same is reproduced below for reference:

“subsidiary company” or “subsidiary”, in relation to any other company (that is to say the holding company), means a company in which the holding company— (i) controls the composition of the Board of Directors; or

(ii) exercises or controls more than one-half of the total share capital either at its own or together with one or more of its subsidiary companies:

Provided that such class or classes of holding companies as may be prescribed shall not have layers of subsidiaries beyond such numbers as may be prescribed.

Explanation.—For the purposes of this clause,—

(a) a company shall be deemed to be a subsidiary company of the holding company even if the control referred to in sub-clause (i) or sub-clause (ii) is of another subsidiary company of the holding company;

(b) the composition of a company‘s Board of Directors shall be deemed to be controlled by another company if that other company by exercise of some power exercisable by it at its discretion can appoint or remove all or a majority of the directors;

(c) the expression “company” includes any body corporate; (d)”layer” in relation to a holding company means its subsidiary or subsidiaries;”

5. Analysis of the Issue:

5.1 Under GST law, supply is the relevant taxable event for levying tax. For an activity/transaction to be liable to GST, existence of ‘supply’ as defined under section 7 of CGST Act, 2017 should be there.

5.2 Section 7 of CGST Act, 2017 defines supply to mean ‘all forms of supply of goods or services or both made or agreed to be made for a consideration by a person in the course or furtherance of business.’ Therefore, it needs to be established that the activity which is to be considered as a supply must be done in course or furtherance of business and there should be a consideration made for the same. Further, Schedule I lists certain activities which are to be treated as a supply even if they are made without any consideration. Entry 2 of Schedule I of CGST Act, 2017 mentions supply of goods or services or both between related persons or distinct persons as a supply even if the same is made without any consideration. Further, Entry 4 of the said Schedule deems import of service by a person from a related person/ company or any of his other establishments outside India as an import of service even if rendered without any consideration, if the said transaction is in course or furtherance of business.

5.3 Further, securities under GST Law is considered neither goods nor services in terms of definition of goods under clause (52) of section 2 of CGST Act, 2017 and in terms of definitions of services under clause (102) of the said section. Further, securities include ‘shares’ as per definition of securities under clause (h) of section 2 of Securities Contracts (Regulation) Act, 1956.

5.4 This implies that the securities held by the holding company in the subsidiary company are neither goods nor services. Further, purchase or sale of securities in itself is neither a supply of goods nor a supply of services. However, as per Explanation to definition of services “under clause 102 of section 2 of CGST Act”, facilitating or arranging transactions in securities may be treated as supply of services. Similarly, activity of lending securities where it provides the right of ownership to third party on payment of certain consideration can be treated as a supply of services. However, purchase and holding of securities/share of the subsidiary company does not in itself constitute a supply of services. Further, mere holding majority shares by holding company of a subsidiary company does not in itself imply that a service is being provided by the holding company to the subsidiary company, solely on the basis that there is a SAC entry ‘997171’ in the scheme of classification of services mentioning; “the services provided by holding companies, i.e. holding securities of (or other equity interests in) companies and enterprises for the purpose of owning a controlling interest.”

5.5 For a transaction/activity to be treated as supply of services there must be a supply as defined under section 7 of CGST Act. Further, if a view is taken that holding shares by a company in its subsidiary company constitutes supply of services, as SAC entry 997171 mentions, then it will also emerge as to whether holding shares of any company even without holding a majority shares will also be considered as supply of services, as nature of transaction essentially remains the same. If such a view is taken then, in effect, every purchase of securities will be deemed as supply of services as every such purchase will lead to holding of securities of the said company by the purchaser. This may be in contradiction with the definition of supply under section 7 of CGST Act read with section 2 of the said Act in terms of definition of goods under clause (52) and definition of services under clause (102) of the said section and therefore will not be tenable.

5.6 Therefore, it appears from the above provisions that the holding of shares in a company per se cannot be treated as a supply of services by a holding company to its subsidiary company.

6. Law Committee deliberated on the issue in its meeting held on 28.06.2023 and recommended that the issue may be clarified through a circular, specifying that mere holding of securities of a subsidiary company by a holding company, whether located in India or abroad, cannot be treated as a supply of services and therefore cannot be taxed under GST.

7. The draft circular in this regard as recommended by Law Committee is enclosed at Annexure A to this agenda note.

8. Accordingly, the Agenda is placed before the GST Council for deliberation and approval.

******

ANNEXURE-A DRAFT Circular No. XX/XX/2023-GST

F. No. CBIC-20001/2/2022 – GST

Government of India

Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs GST Policy Wing

*****

New Delhi, Dated the XXXXXX, 2023

To,

The Principal Chief Commissioners/ Chief Commissioners/ Principal Commissioners/ Commissioners of Central Tax (All) The Principal Directors General/ Directors General (All) Madam/Sir,

Subject: Clarification on various issues pertaining to GST-reg.

Representations have been received from the trade and field formations seeking clarification on certain issues whether the holding of shares in a subsidiary company by the holding company will be treated as ‘supply of service’ under GST and will be taxed accordingly or whether such transaction is not a supply.

2. In order to clarify the issue and to ensure uniformity in the implementation of the provisions of law across the field formations, the Board, in exercise of its powers conferred by section 168 (1) of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “CGST Act”), hereby clarifies the issues as under:

2. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

3. Difficulty, if any, in implementation of this Circular may please be brought to the notice of the Board. Hindi version would follow.

(Sanjay Mangal) Principal Commissioner (GST)

Agenda Item 3(xvii): Amendment in CGST Rules, 2017

Law Committee, in its various meetings, has deliberated upon several issues and has recommended changes in some of the provisions of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as “the CGST Rules”). In addition to the changes in the provisions of the CGST Rules, some changes in the FORMS under CGST Rules have also been recommended by the Law Committee. These changes are discussed below:

1. Omission of clause (c) of Explanation (1) to Rule 43

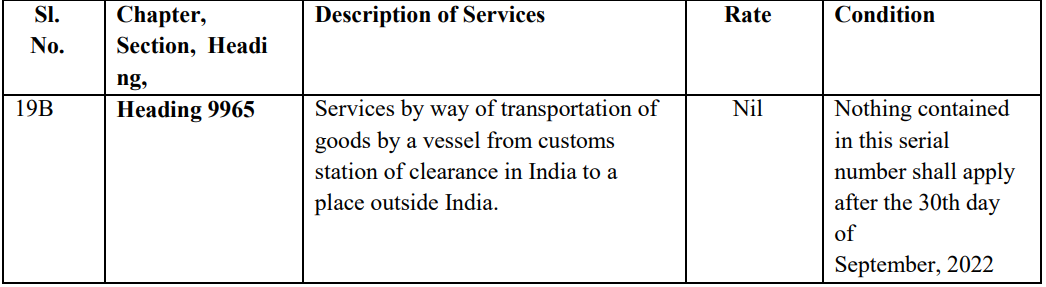

1.1 As per Sr. No 19B of Exemption Notification No. 12/2017 Central Tax (Rate) dated 28th June 2017, as amended from time to time, services by way of transportation of goods by a vessel from customs station of clearance in India to a place outside India was an exempt supply till 30.09.2022. Relevant extract of the said entry in the notification for ease of reference is as under –

1.2 However, this exemption has not been extended after 30.09.2022. As a result, the said service has become taxable after 30.09.2022. Normally, in the case when outward supply is exempt, the supplier needs to reverse the common ITC in accordance with rule 42 or rule 43 of CGST Rules. Since, the above service is not an exempt supply w.e.f 01.10.2022, reversal of ITC in respect of supply of the said services is not required w.e.f. 01.10.2022. Further, there are certain exclusion in the Explanation to Rule 43 of CGST Rules like the above mentioned services whose value of supply was excluded from the value of exempt supplies.

1.3 The Clause (c) of Explanation 1 to Rule 43 of CGST Rules is reproduced as under:

Explanation 1: -For the purposes of Rule 42 and this Rule, it is hereby clarified that the ggregate value of exempt supplies shall exclude:- (c) the value of supply of services by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.

1.4 Consequent to lapsing of the exemption given vide Entry No. 19B of Exemption Notification No. 12/2017 Central Tax (Rate) dated 28th June 2017, there is a need to omit the said clause (c) of Explanation to Rule 43 of CGST Rules, as supply of aforementioned services is not an exempt supply with effect from 1st October 2022.

1.5 In view of the above, the Law Committee in its meeting held on 10.04.2023 and 11.04.2023 recommended that clause (c) of Explanation (1) at the end of Rule 43 of CGST Rules may be omitted.

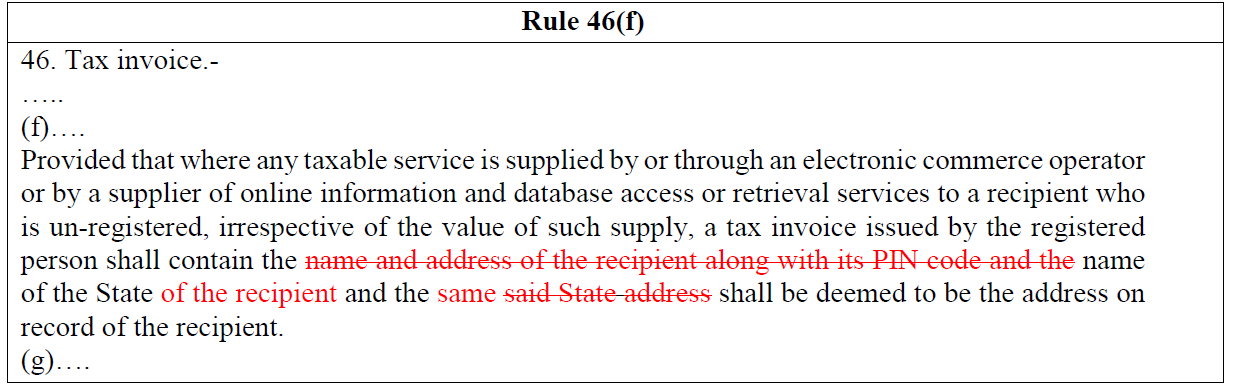

II. Amendment in proviso to rule 46(f)

2.1 As per the recommendations of GST Council in its 48th meeting, rule 46 of CGST Rules has been amended vide Notification No. 26/2022 –Central Tax dated 26.12.2022 by adding a proviso to clause (f) of the said rule to provide that where any taxable services is supplied by or through an electronic commerce operator or by a supplier of online information and database access or retrieval services to a recipient who is un-registered, irrespective of the value of such supply, a tax invoice issued by the registered person shall contain the name and address of the recipient along with its PIN code and the name of the State of the recipient and the said State address shall be deemed to be the address on record of the recipient.

2.2 However, subsequent to the said amendment, concerns were received from some tax administrations that there may be cases where the supplier may have the information about the State name of the recipient, but may not have the full address and the PIN code of the recipient. In such cases, there may be a possibility that the supplier may declare the place of supply as his own location, due to non-availability of the full address details of recipient. This may lead to loss of revenue for the consumption states. Besides, representations have also been received from some sections of the industry mentioning that in certain services sector, exact address of the recipient may not be feasible for the supplier to be collected due to peculiar nature of the supply, and only name of the State of the recipient may be collected and recorded. Accordingly, request has been made to not insist of full address details of the recipient and only the name of State of the recipient may be sufficient to be provided in the tax invoice.

2.3 The matter was deliberated by the Law Committee in its meeting held on 10.04.2023 & 11.04.2023. Law Committee recommended that proviso to rule 46(f) of CGST Rules may be amended to provide that the tax invoice shall contain the name of the State of the recipient and the name and address of the recipient along with its PIN code may not be mandatory to be declared on the tax invoice. Further, the State of the recipient shall be deemed to be the address on record of the recipient. Accordingly, the Law Committee recommended the following amendment in proviso to rule 46(f) pf CGST Rules, as shown, in red color:

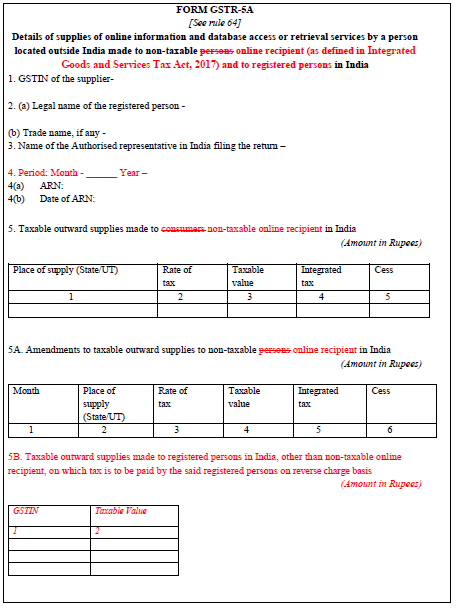

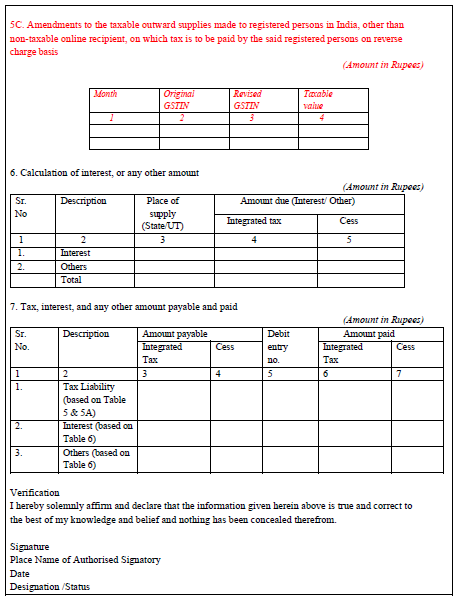

III. Amendment in rule 64 and FORM GSTR-5A

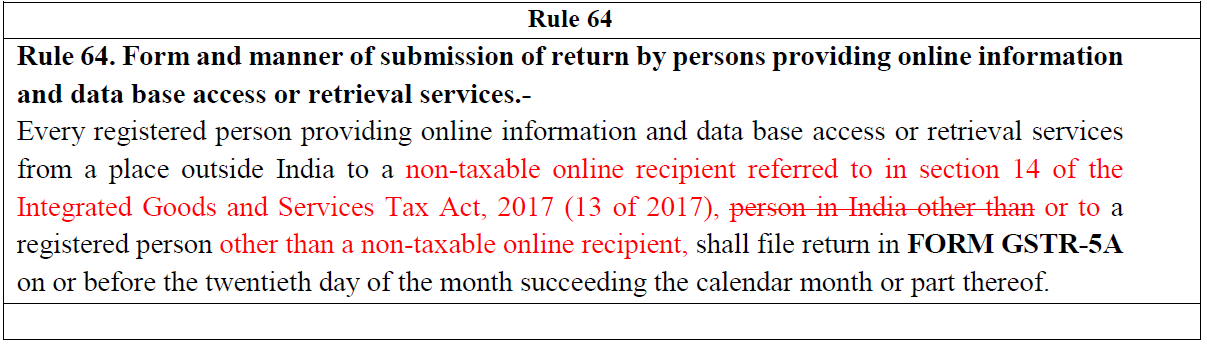

3.1 FORM GSTR-5A presently covers details of supplies of online information and database access or retrieval (OIDAR) services by a person located outside India made to non-taxable persons in India. The said form does not cover the details of supplies of online information and database access or retrieval services by a person located outside India made to a registered person in India. A registered person other than non-taxable online recipient located in India receiving online information and database access or retrieval services from a person located outside India is required to pay tax on such receipt of services on reverse charge basis as per Notification No. 10/2017-Integrated Tax (Rate) dated 28.06.2017. It is suggested that if the details of supplies made by the said OIDAR service provider to registered persons in India other than non-taxable online recipient can also be captured in FORM GSTR-5A, it can help in ensuring tax compliance by the said registered persons paying tax on reverse charge basis. Accordingly, it is proposed that format of FORM GSTR-5A be modified so as to also include details of supplies made by the OIDAR service provider located outside India to registered persons other than non-taxable online recipient in India.

3.2 Rule 64 of CGST Rules provides that every registered person providing online information and data base access or retrieval services from a place outside India to a person in India other than a registered person shall file return in FORM GSTR-5A on or before the twentieth day of the month succeeding the calendar month or part thereof. Since the proposed FORM GSTR-5A will also include details of supplies made by OIDAR services provider to registered persons in India, amendment is required in the said rule so as to prescribe that every registered person providing online information and data base access or retrieval services from a place outside India to non-taxable online recipient or to a registered person(other than a non-taxable online recipient) in India shall file return in FORM GSTR-5A.

3.3 Accordingly, Law Committee in its meeting held on 10.04.2023 & 11.04.2023 and 28.06.2023 has recommended amendment in rule 64 and in FORM GSTR-5A so as to also include details of supplies made by the OIDAR service provider located outside India to registered persons other than non-taxable online recipient in India. The proposed amendment in rule 64 and FORM GSTR-5A is shown, in red color, as below:

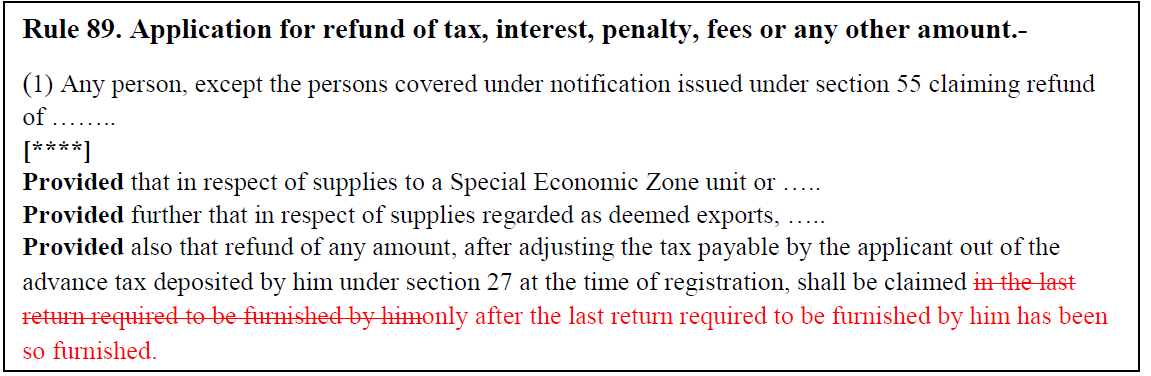

IV. Amendment in Rule 89(1):

4.1 Sub-rule (1) of rule 89 of the CGST Rules prescribes the manner of filing of Refund application for claiming refund of any balance in the electronic cash ledger in accordance with the provisions of sub-section (6) of section 49 or any tax, interest, penalty, fees or any other amount paid by a person, other than refund of integrated tax paid on goods exported out of India.

4.2 3rd proviso to sub-rule (1) of rule 89 provides that refund of any amount, after adjusting the tax payable by the applicant out of the advance tax deposited by him under section 27 of CGST Act, 2017 at the time of registration, shall be claimed in the last return required to be furnished by him. However, the Form GSTR- 3B for return does not provide any option for claiming refund.

4.3 In this regard, reference is drawn to section 24 of CGST Act, 2017 which specifies that casual taxable persons and Non-resident taxable persons who are making taxable supply are required to take compulsory registration. Sub-section (2) of section 27 of the Act ibid specifies that a casual taxable person or a non-resident taxable person shall, at the time of submission of application for registration under sub-section (1) of section 25 of CGST Act, 2017, make an advance deposit of tax in an amount equivalent to the estimated tax liability of such person for the period for which the registration is sought. Sub-section (3) of section 27 of CGST Act, 2017 states that the advance tax amount deposited shall be credited to the electronic cash ledger of such person and shall be utilized in the manner provided under section 49 of CGST Act, 2017. Further, Sub-section (6) of Section 49 of the CGST Act, 2017 specifies that the balance in the electronic cash ledger or electronic credit ledger after payment of tax, interest, penalty, fee or any other amount payable under this Act or the Rules made thereunder may be refunded in accordance with the provisions of section 54 of CGST Act, 2017.

4.4 In view of the provisions mentioned above, it is felt that the balance remaining out of advance tax amount deposited by the casual taxable person is in the nature of excess balance in electronic cash ledger only, which can be claimed as refund of balance in the electronic cash ledger after filing of the last return.

4.5 The Law Committee, in its meeting dated 10.04.2023 & 11.04.2023 deliberated on this issue and recommended that 3rd proviso to sub-rule (1) of rule 89 may be amended (shown in red color), as below:

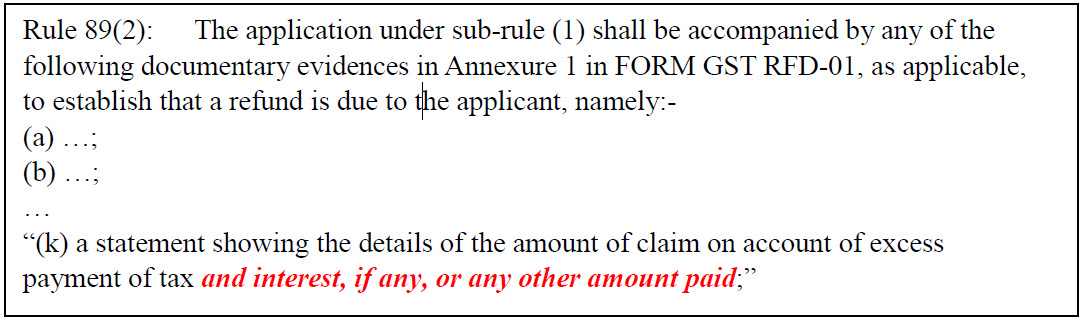

V. Amendment in Rule 89(2)(k):

5.1 In terms of clause (e) of sub-section (8) of section 54 of the CGST Act, 2017, a registered taxpayer can file an application for refund of excess payment of tax and interest, if any, or any other amount paid by him if he has not passed on the incidence of such tax and interest to any other person.

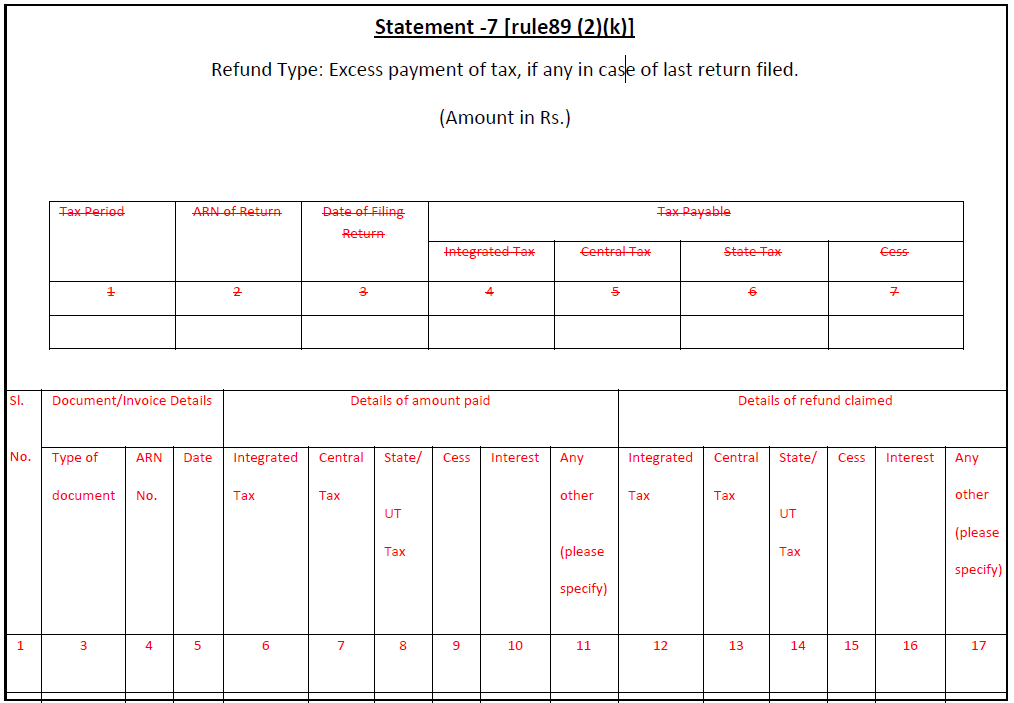

5.2 In terms of clause (k) of sub-rule (2) of Rule 89 of CGST Rules, Statement 7 as appended to FORM GST RFD-01 is required to be submitted along with the application for refund which is made under the category ‘Excess Payment of Tax’.

5.3 The format of Statement -7 is as follows:-

Statement -7 [rule 89 (2)(k)]

Refund Type: Excess payment of tax, if any in case of last return filed.

(Amount in Rs.)

5.4 It appears that Statement -7 is designed for excess payment of tax made in a particular return. It has been reported by some tax administrations that this restricts a taxpayer from filing the claim of refund under the category ‘Excess Payment of Tax’ for any amount of excess payment of tax which is not relatable to a particular return period or that of excess payment of interest, penalty or late fee. However, it is possible that excess payment may happen under various circumstances some of which are illustrated below:

a) Excess payment can be detected at the time of reconciliation of accounts and it might be relatable to multiple return periods without clearly being attributable to any particular return.

b) Excess payment may be made through FORM GST DRC-03, FORM GST DRC-07 andFORM GST CMP-08.

5.5 In such cases, it is being reported that a taxpayer cannot claim refund under the category “Excess Payment of Tax” as the related particulars cannot be furnished in Statement-7 of FORM GST RFD-01 and they end up claiming the same under the category “Any Other”.

5.6 However, circumstances under which refunds can be claimed under the category “Any Other” is clarified in the circulars issued in this regard and the same are specific in nature which do not cover this condition.

5.7 Furthermore, though sub-section (8) of section 54 provides for refund of excess payment of tax and interest, if any, or any other amount paid, statement as required in terms of clause (k)of sub-rule (2) of Rule 89 restricts the same to tax only necessitating alignment of the same withthe aforesaid sub-section.

5.8 In view of the above, Law Committee, in its meeting held on 14.06.2023 &15.06.2023 deliberated on this issue and recommended that clause (k) of sub-rule (2) of Rule 89 may be amended (shown in red colour), as below. Further, Statement 7 in FORM GST RFD 01 may also be amended to incorporate the said rule change.

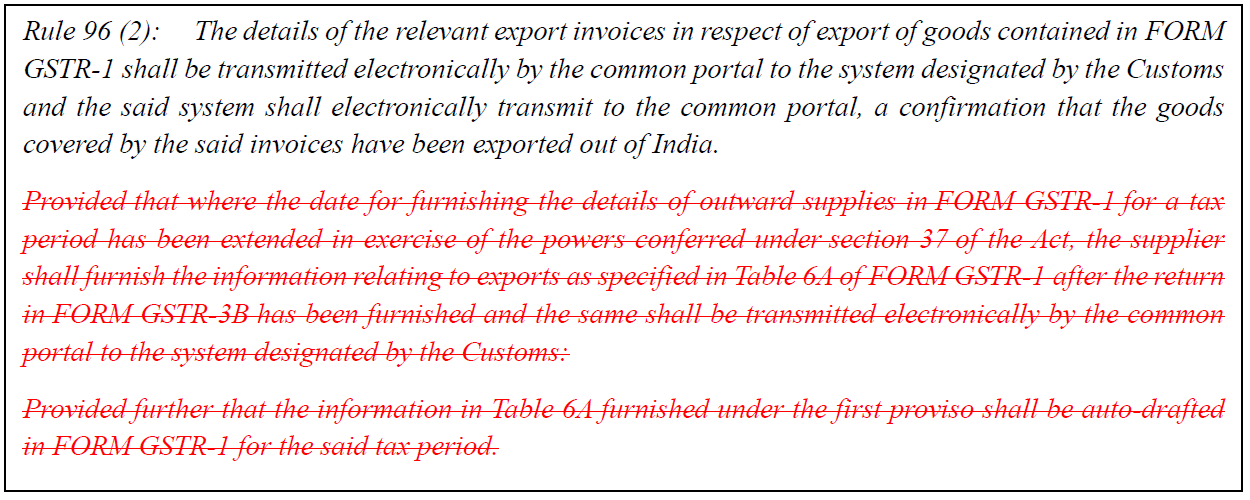

VI. Amendment in Rule 96(2):

6.1 Rule 96 of the CGST Rules, 2017 prescribes the manner of processing of Refund of integrated tax paid on goods [or services] exported out of India. Sub-rule (2) of rule 96 prescribes the process of transmission of export data from common portal to system designated by the Customs for further processing of the said refund application.

6.2 1st Proviso to Rule 96(2) provides that where the date for furnishing the details of outward supplies in FORM GSTR-1 for a tax period has been extended in exercise of the powers conferred under section 37 of CGST Act, 2017, the supplier shall furnish the information relating to exports as specified in Table 6A of FORM GSTR-1 after the return in FORM GSTR-3B has been furnished and the same shall be transmitted electronically by the common portal to the system designated by the Customs. 2nd Proviso to Rule 96(2) of CGST Rules provides further that the information in Table 6A furnished under the first proviso shall be auto-drafted in FORM GSTR-1 for the said tax period.

6.3 It may be observed that the option to file the export details of Table 6A of FORM GSTR 1 separately was made available initially during the period when filing of FORM GSTR-1 was delayed on the portal and filing of FORM GSTR-1 was not mandatory before filing of return in FORM GSTR-3B. However, now concept of sequential filling of Return has been introduced. Section 37 & section 39 of CGST Act, 2017 have been amended vide Notification No. 18/2022–Central Tax dated 28th September, 2022 with effect from 01 October, 2022. According to section 37(4) of CGST Act, 2017, a taxpayer shall not be allowed to file FORM GSTR-1 if previous FORM GSTR-1 is not filed and as per section 39(10) of the said Act, a taxpayer shall not be allowed to file return in FORM GSTR-3B if FORM GSTR-1 for the same tax period has not been filed.

6.4 Hence, Law Committee observed that 1st and 2nd proviso to sub-rule (2) of rule 96 do not serve any purpose now after the said amendments in CGST Act and hence have become redundant. Accordingly, the Law Committee in its meeting dated 10.04.2023 and 11.04.2023 recommended omission (shown in red colour) of Proviso 1 and Proviso 2 to rule 96(2) of CGST Rules, as below:

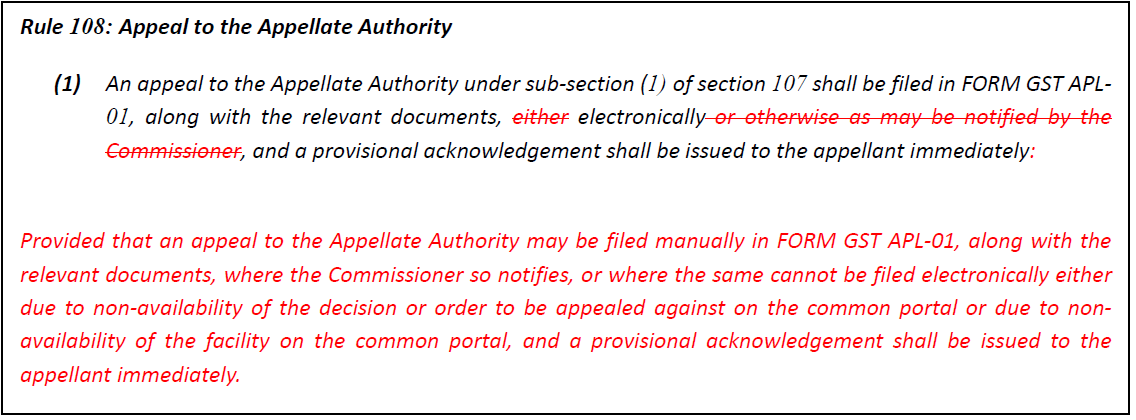

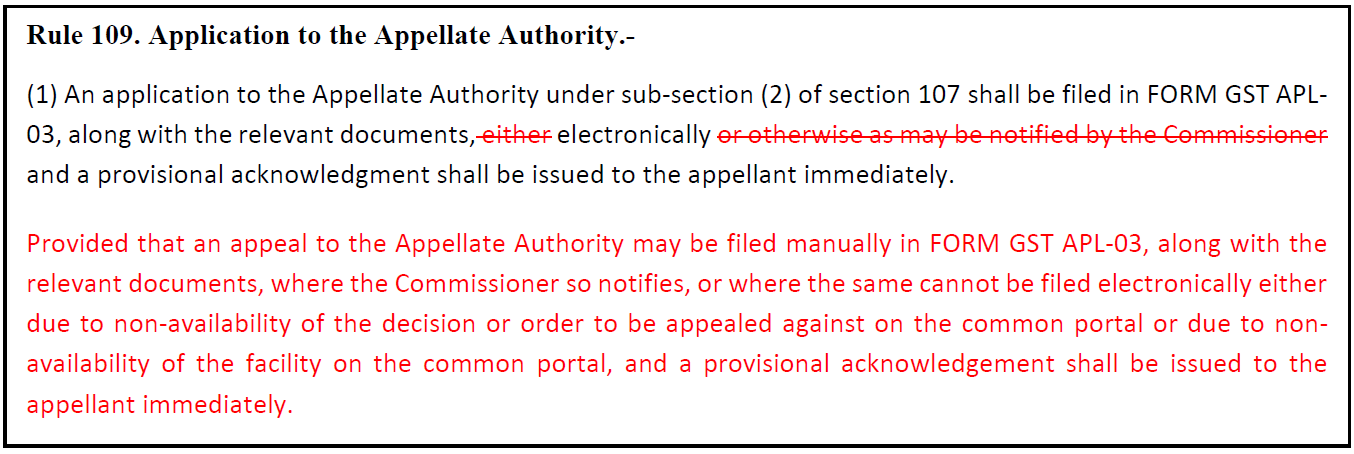

VII. Amendment in rule 108 and rule 109

7.1 In terms of sub-section (1) of section 107 of the CGST Act, 2017, any person aggrieved by any decision or order passed by an adjudicating authority may appeal to the concerned appellate authority within three months from the date of communication of the said decision or order to such person. Similar provision exists under sub-section (2) of section 107 of CGST Act to provide for filing appeal by an officer authorised by the Commissioner to the appellate authority within six months from the date of communication of the said decision or order.

7.2 In terms of sub-rule (1) of rule 108 of the CGST Rules, a doubt emerges whether an appeal under section 107 can be filed either electronically or manually, at the liberty of the Appellant. The aforesaid formulation has remained un-amended since the inception of GST in 2017. This was the time when the functionalities relating to registration, returns, payments and refunds had been rolled out on the common portal and the other processes/functionalities like Appeal, Advance Ruling, Scrutiny, etc. were still being developed. Thus, it was felt that, for instance, where the filing of an Appeal becomes necessary, an alternative mechanism as notified by the Commissioner may also be provided.

7.3 The issue was deliberated by the Law Committee in its meeting held on 10th/ 11th April, 2023, 31.05.2023 and 28.06.2023. The Law Committee noted that the rule provides mainly for filing of appeals, electronically, on the portal. Only in the cases where the Commissioner so notifies, the appeal can be filed in a mode other than electronically on the portal. However, as some of the Courts are taking a view that as per the present wording of rule 108 of CGST Rules, manual filing of appeals may also be considered as a default route of filing appeal under section 107 of CGST Act, there may be a requirement of the amendment in rule 108 and rule 109 of CGST Rules to provide clearly under what circumstances manual appeals may be filed under section 107 of CGST Act.

7.4 The Law Committee accordingly recommended amendment in rule 108 and rule 109 of CGST Rules (amendment shown in red color) by inserting a proviso in both of the said rules for filing appeal manually in certain specified circumstances.

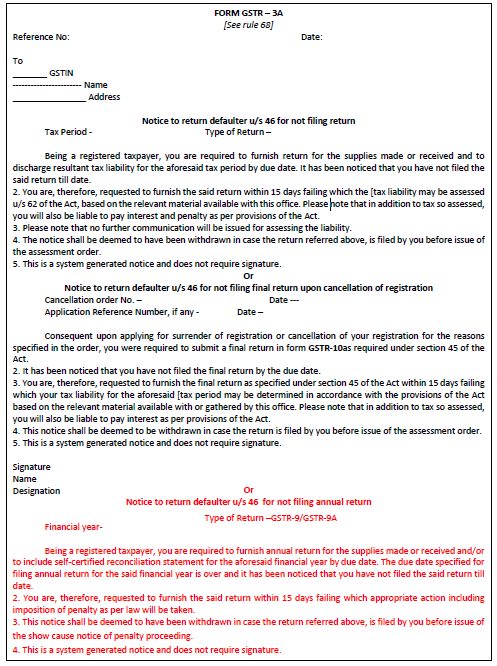

VIII. GSTR-3A notice for non-filing of Annual Return in FORM GSTR-9 or FORM GSTR-9A:

8.1 Section 46 of the CGST Act, 2017 read with Rule 68 of CGST Rules, 2017 requires issuance of a notice in FORM GSTR-3A to a registered person who fails to furnish return under Section 39 or Section 44 or Section 45 or Section 52 requiring him to furnish such return within fifteen days.

8.2 While FORM GSTR-3A has provision to issue notice to return defaulter as well as defaulters of final return, there is no provision in it to issue notice to defaulters of Annual returns.

8.3 In view of the same, the Law Committee in its meetings held on 15.03.2023, 10.04.2023 and 11.04.2023 recommended suitable amendment in FORM GSTR-3A (highlighted in red) for issuance of notice to the registered taxpayer for their failure to furnish Annual Return in FORM GSTR-9 or FORM GSTR-9A.

9. Accordingly, the agenda note is placed before the GST Council for deliberation and approval. Pari-Materia changes would also be required in the respective SGST Rules.

**********

Agenda Item 3(xviii): Proposal to provide a special procedure to file appeal against the orders passed in accordance with the Circular No. 182/14/2022-GST, dated 10.11.2022, pursuant to the directions issued by the Hon’ble Supreme Court in the Union of India v/s Filco Trade Centre Pvt. Ltd – regarding.

The Hon’ble Supreme Court in the Union of India v/s Filco Trade Centre Pvt. Ltd., SLP(C) No.32709-32710/2018 had directed that the common portal be opened for filing prescribed forms for availing Transitional Credit through TRAN-1 and TRAN-2 for two months from 01.10.2022 to 30.11.2022 for the aggrieved registered persons. In this regard, reference is also invited to Circular No. 180/12/2022 dated 09.09.2022 vide which guidelines have been issued for the applicants for filing new TRAN-1/TRAN-2 or revising the already filed TRAN-1/TRAN-2 on the common portal, and to Circular No. 182/14/2022-GST dated the 10th of November, 2022 prescribing guidelines to the officers for verifying the Transitional Credit and pass orders accordingly.

2. In light of this, it has been brought to the notice that though several taxpayers, or the Department, intend to file appeal against the orders issued by the proper officers in respect of such claims of transitional credit filed by the registered persons in accordance with the above mentioned directions issued by Hon’ble Supreme Court, there is presently no functionality available on the portal for enabling them to file such appeals. In some cases, time limit for filing appeals under provisions of section 107 of CGST Act, 2017 has already expired or is going to expire shortly.

3. Law Committee in its meetings held on 03.05.2023, 14/15.06.2023 and 28.06.2023 deliberated on the issue and recommended to provide a special procedure for filing of appeals manually against the orders passed in accordance with Circular No. 182/14/2022-GST dated the 10th of November, 2022. A draft notification providing the special procedure to be followed by a person desirous of filing an appeal against an order passed by the proper officer in accordance with Circular No. 182/14/2022-GST, dated10th of November, 2022 pursuant to the directions issued by the Hon’ble Supreme Court in the Union of India v/s Filco Trade Centre Pvt. Ltd., SLP(C) No.32709-32710/2018, as recommended by the Law Committee is enclosed with this agenda note as Annexure-A.

4. Accordingly, the recommendations of the Law Committee as detailed in para 3 is placed before the GST Council for approval.

ANNEXURE A

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS NOTIFICATION No. /2023 – CENTRALTAX

New Delhi, the —- June, 2023

S.O.(E).— In exercise of the powers conferred by section 148 of the Central Goods and Services Tax Act,2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby notifies the following special procedure to be followed by a registered person (hereinafter referred to as “the said person”) desirous of filing an appeal against an order (hereinafter referred to as “the said order”) passed by the proper officer in accordance with Circular No. 182/14/2022-GST, dated 10th of November, 2022 pursuant to the directions issued by the Hon’ble Supreme Court in the Union of India v/s Filco Trade Centre Pvt. Ltd., SLP(C) No.32709-32710/2018.

Explanation. – For the purposes of this notification, the expression “said person” shall include the officer referred to in sub-section (2) of Section 107.

2. The appeal against the said order shall be made in duplicate in the Form appended to this notification at ANNEXURE-1 and shall be presented manually before the Appellate Authority within the time specified in sub-section (1) of Section 107 or sub-section (2) of Section 107, as the case may be, and such time shall be computed from the date of issuance of this notification or the date of the said order, whichever is later:

Provided that any appeal against the said order filed in accordance with the provisions of Section 107 with the Appellate Authority before the issuance of this notification, shall be deemed to have been filed in accordance with this notification.

3. The said person shall not be required to deposit any amount as referred to in sub-section (6) of Section 107 as a pre-condition for filing an appeal against the said order.

4. An appeal filed under this notification shall be accompanied by relevant documents including a self-certified copy of the said order. Further, the appeal and the relevant documents shall be signed by the person specified in sub-rule (2) of rule 26 of CGST Rules.

5. Upon receipt of the appeal referred to in para 4, duly verified in the manner provided above and accompanied by the relevant documents, an acknowledgement, indicating the appeal number, shall be issued manually in FORM GST APL-02 by the Appellate Authority or an officer authorized by him in this behalf and the appeal shall be treated as filed only when the aforesaid acknowledgement is issued.

6. The Appellate Authority shall, along with its order, issue a summary of the order in the Form appended to this notification as ANNEXURE-2.

Name Designation

ANNEXURE-1

Appeal to Appellate Authority

(Filed against an order passed in accordance with Circular No. 182/14/2022-GST, dated 10th of November, 2022 pursuant to the directions issued by the Hon’ble Supreme Court in the Union of India v/s Filco Trade Centre Pvt. Ltd., SLP(C) No.32709-32710/2018)

1. GSTIN– 2. Legal name of the appellant –

3. Trade name, if any –

4. Address –

5. Order No. – Order dated –

6. Designation of the officer passing the order appealed against –

7. Date of communication of the order appealed against –

8. Name of the authorized representative –

9. Details of the case under dispute –

(i) Brief issue of the case under dispute –

(ii) Amount of transitional credit claimed before the issuance of circular no. 182/14/2022-GST, dated 10th of November, 2022 (Act-wise)–

(iii) Details of any order u/s 73/74 passed in respect of the claim referred to in sub-item (ii) above:

(a) Order No. – Order dated-

(b) Amount allowed as per said order (Act-wise)- Rs.

(c) Interest and penalty levied as per said order (Act-wise)- Rs.

(d) Whether any appeal preferred against said order- Yes/No

(e) If appeal filed then Appeal No.- Appeal Date-

(f) Status of said Appeal- Disposed/Pending

(g) If appeal disposed off then amount of credit allowed as per said Appeal (Act-wise)- Rs.

(iv) Amount of transitional credit claimed after the issuance of circular no. 182/14/2022-GST, dated 10th of November, 2022 (Act-wise)–

(v) Amount of credit allowed in pursuance of claim referred to in sub-item (iii) above (Act-wise)- Rs.

(vi) Amount under dispute (Act-wise)- Rs.

10. Whether the appellant wishes to be heard in person – Yes / No

11. Statement of facts:

12. Grounds of appeal:

13. Prayer:

Verification

I, < _________________________ >, hereby solemnly affirm and declare that the information given here in above is true and correct to the best of my knowledge and belief and nothing has been concealed therefrom.

Place: Date:

Signature Name of the Applicant

Note:

1. If the space provided for answering any item is found to be insufficient, separate sheets may be used.

2. The letters “N.A.” may be recorded against any item that is not required for this Appeal.

ANNEXURE-2

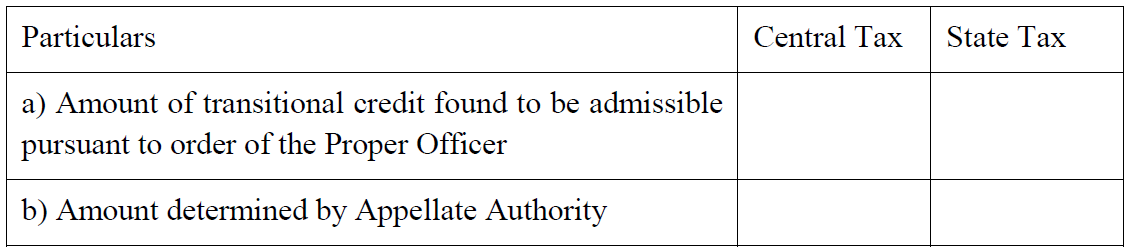

SUMMARY OF TRANSITIONAL CREDIT AVAILABLE AFTER ISSUE OF ORDER BY THE APPELLATE AUTHORITY WITH REFERENCE TO AN ORDER PASSED IN ACCORDANCE WITH CIRCULAR NO. 182/14/2022-GST, DATED 10th of NOVEMBER, 2022

A. GSTIN –

B. Name of the Appellant/ person-

Address of the appellant/person –

C. Order appeal against- Ref. (if any) Dated-

E. Personal Hearing- Dated-

F. Order in Brief-

G. Status of Order- Confirmed/Modified/Rejected

H. Amount of Credit/ Demand after Appeal-

Place: Date:

Signature: Name of the Appellate Authority: Designation: Jurisdiction

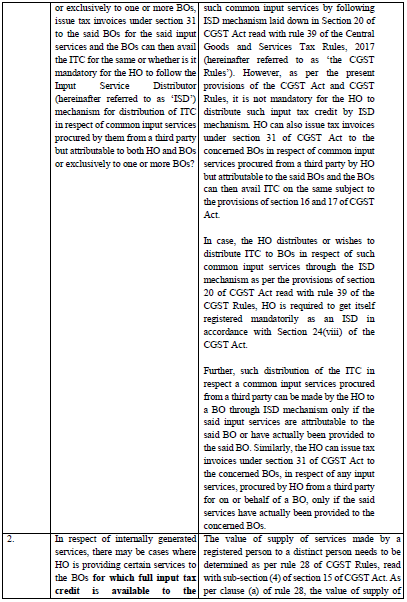

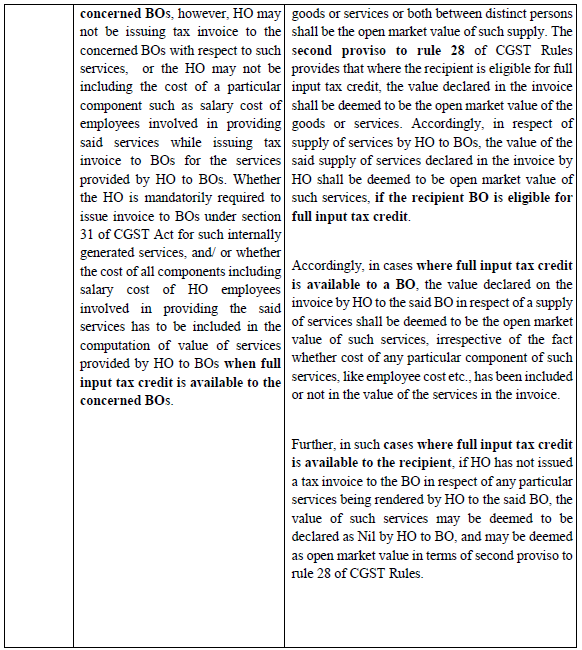

Agenda Item 3(xix): Issues pertaining to ISD mechanism and taxability of services provided by one distinct person to another distinct person.

A taxpayer with multiple branch offices often procures the input services from a third party at Headquarters or at one office, for and on behalf of the other offices. Such taxpayers can then adopt various mechanisms to transfer the ITC pertaining to such input services to the said offices.

1.Input Service Distributor Mechanism:

1.1 An Input Service Distributor (ISD) is a taxpayer that receives invoices for input services used by its one or more branches. It distributes the Input Tax Credit (ITC), to such branches based on a specified mechanism by issuing ISD invoices. The branches can have different GSTINs but must have the same PAN as that of ISD. Section 2(61) of CGST Act, 2017 defines ISD as under:

“2(61) “Input Service Distributor” means an office of the supplier of goods or services or both which receives tax invoices issued under section 31 towards the receipt of input services and issues a prescribed document for the purposes of distributing the credit of central tax, State tax, integrated tax or Union territory tax paid on the said services to a supplier of taxable goods or services or both having the same Permanent Account Number as that of the said office;” 1.2 Further section 20 of CGST Act, 2017 provides for manner of distribution of credit by Input Service Distributor to its branch offices. Section 20 is reproduced below:

“20. Manner of distribution of credit by Input Service Distributor.— (1) The Input Service Distributor shall distribute the credit of central tax as central tax or integrated tax and integrated tax as integrated tax or central tax, by way of issue of a document containing the amount of input tax credit being distributed in such manner as may be prescribed.

(2) The Input Service Distributor may distribute the credit subject to the following conditions, namely:––

(a) the credit can be distributed to the recipients of credit against a document containing such details as may be prescribed;

(b) the amount of the credit distributed shall not exceed the amount of credit available for distribution;

(c) the credit of tax paid on input services attributable to a recipient of credit shall be distributed only to that recipient;

(d) the credit of tax paid on input services attributable to more than one recipient of credit shall be distributed amongst such recipients to whom the input service is attributable and such distribution shall be pro rata on the basis of the turnover in a State or turnover in a Union territory of such recipient, during the relevant period, to the aggregate of the turnover of all such recipients to whom such input service is attributable and which are operational in the current year, during the said relevant period;

(e) the credit of tax paid on input services attributable to all recipients of credit shall be distributed amongst such recipients and such distribution shall be pro rata on the basis of the turnover in a State or turnover in a Union territory of such recipient, during the relevant period, to the aggregate of the turnover of all recipients and which are operational in the current year, during the said relevant period.

Explanation.––For the purposes of this section,––

(a) the “relevant period” shall be––

(i) if the recipients of credit have turnover in their States or Union territories in the financial year preceding the year during which credit is to be distributed, the said financial year; or (ii) if some or all recipients of the credit do not have any turnover in their States or Union territories in the financial year preceding the year during which the credit is to be distributed, the last quarter for which details of such turnover of all the recipients are available, previous to the month during which credit is to be distributed;

(b) the expression “recipient of credit” means the supplier of goods or services or both having the same Permanent Account Number as that of the Input Service Distributor; (c)the term ‘‘turnover’’, in relation to any registered person engaged in the supply of taxable goods as well as goods not taxable under this Act, means the value of turnover, reduced by the amount of any duty or tax levied under entries 84 and 92 A of List I of the Seventh Schedule to the Constitution and entries 51 and 54 of List II of the said Schedule.”

2. Mechanism whereby head office raises invoice under section 31 to the branch office without registering as ISD