Annexure to Agenda Item 5 on Report of GoM on Casinos, Race Courses and Online Gaming

Table of Contents

I. Background:

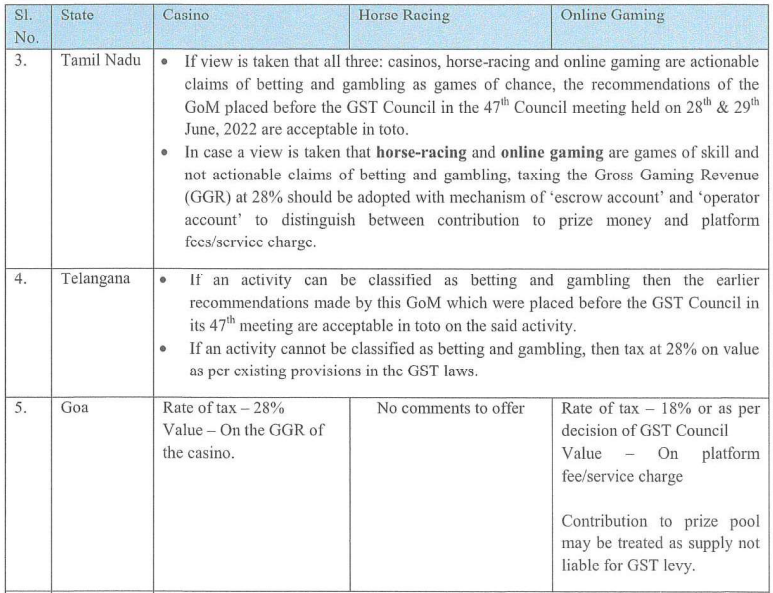

A Group of Ministry (GoM) on Casinos, Racc Courscs and Online Gaming was constituted vide OM dated 24.05.2021 based on the recommendation of the GST Council in its 42nd meeting held on 5th & 12th October, 2020. In the 45th meeting of the GST Council, held on the 17th September, 2021, the Council was of the view that the said GoM may examine all issues, including those around rates involved in online gaming, horse racing and casinos. The GoM was reconstituted on 10th February, 2022, with Chief Minister of Meghalaya as Convener with the existing Terms of Reference.

2. GoM report and decision of the GST Council:

2.1 The GoM submitted its report and it was place before the GST Council in its 47th meeting held on 28th and 29th June, 2022. [Annexure].

2.2 During the said GST Council meeting, the Convenor, Chief Minister of Meghalaya presented the report and explained that the GoM had looked into following three major aspects:

. What rate should be applied to these three different sectors; whether it should be 18% or 28%?

. Whether GST should be charged on the commission charged by the organizers or should it be charged on the entire value of the stakes?

. Casinos involve a bouquet of games, with different forms of betting, with interplay of multiple factors and different activities such as entry fee, fees on the food and beverages consumed inside, fees on the chips bought, transportation of the players etc. The GoM had to deliberate on as to how to tax these different components within the overall casino activity. Further online gaming, horse racing and casino are three very different sectors, though all involve some form of betting and gambling, but the way they operate is diverse from each other. It was felt that the GoM needed to find some uniformity in the rates and valuation of each activity in these sectors.

2.3 The GoM recommendations with regard to GST on Casinos, Race courses and Online Gaming are reproduced below:

I. Imposition of GST on these activities namely, casinos, race courses, online gaming and lottery should be uniform (in terms of and valuvation).

II. For the purpose of levy of GST, no distinction should be made in these activities merely on the ground that an activity is a game of skill or chance or both.

III. Rate of GST: GST may be levied at the rate of 28% on all activities namely Casinos, Race Courses and Online Gaming.

IV. Valuation:

a. In case of online gaming, the activities be taxed at 28% on the full value of the consideration, by whatever name such consideration may be called including contest entry fee, paid by the player for participation in such games without making a distinction such as games of skill or chance etc.

b. In case of Race Courses, GST continue to be levied at the rate of 28% on the full value of bets pooled in the totalisator and placed with the bookmakers.

c. In case of Casinos, GST be applied at the rate of 28% on full face value of the chips/coins purchased from casino by a player.

d In case of casinos, once GST is levied on purchase of chips/coins (on face value), no further GST to apply on the value of bets placed in each round of betting including those played with winnings of previous rounds.

V. Entry fee to casinos: GST at the rate of 28% is leviable on the services by way of access/entry to Casinos on payment of consideration/entry fee which compulsorily includes price of one or more other supplies such as food, beverages etc.; his being a mixed supply, However, optional supplies made independently of the entry ticket shall be taxed at the rates as applicable on such supplies.

Rationale;

(i) The general view in the GoM was that all these activities, because of their nature and negative externalities, should be taxed at the highest rate of tax. These activities involve elements of financial risk, are addictive in nature and have an adverse impact on the society at large and the youth in particular. There was broad consensus that imposition of GST on these activities should be uniform in terms of rate and valuation. In this background, it was unanimously decided that the activities of casinos, race courses, and online gaming should be subjected to GST at the highest rate of 28%.

(ii) As regards the question whether the activities of horse racing, casinos and online gaming are activities of games of skill or chance, the general view was that this distinction should not be relevant for GST. So long as there is betting for monetary winnings, the activities should be similarly taxed. The GoM was of the unanimous view that any such difference, if it exists in the GST law, differentiating the activities as games of chance or games of skill, be eliminated for application of uniform taxation on all these activities.

(iii) As regards valuation, there was broad agreement that mechanism of valuation should be simple and easy to calculate, in conformity with law and at the same time should not render the industry unviable. Further, it had to be ensured that any decision with regard to valuation of the said activities does not have an implication for taxation of lottery which is now a settled issue. Further as GST is a pass-through tax, the incidence of entire GST has to be borne by the players, and its incidence does not fall on the suppliers involved in these activities.

(iv) On the question of taxing these activities on GGR/net value, the GoM observed that actionable claims in the form of lottery, betting and gambling have been consciously brought in the fold of GST. Only a single levy of GST is applied replacing a multitude of cascading taxes in pre-GST regime ranging from entry tax, statutory entry fee collected by Government, surcharge thereon, VAT, entertainment tax, betting/gambling tax, services tax and embedded excise duty on inputs. Many of these taxes were levied on full face value of bets/chip sale value etc. In such a context, by removing the prize pay-outs from the value of bets, it will result in effectively removing actionable claims from the value of supply, defeating the very legislative intent of bringing actionable claims within the purview of GST.

(v) Unlike other countries, India taxes actionable claims as a supply of goods and therefore, the international practice with regard to the levy of GST/VAT on these actionable claims has little relevance for India. As observed by the Hon’ble Supreme Court in Skill Lotto case, we will have to find answers to questions before us in our own statutes. The practice in other countries is guided by their own laws which are different from ours.

2.4 In the 47th meeting of the Council, Hon’ble Minister from Goa raised certain reservations about the recommendations in the said report of the GoM stating that if the Council accepted the GoM report, it would lead to closure of the industry and the activities would move into the grey markets. He also put forth the suggestion that the pre-GST model and international best practices on taxation of casinos need to be considered. He further stated that the stakeholders were not requesting a reduction in the rate of tax from 28% to 18% but a different valuation mechanism to tax the casinos. He emphasised that casinos, horse racing and online gaming should not be clubbed together as each activity is completely different. He requested that the issues may be reconsidered and that stakeholders may be consulted.

2.5 On the suggestion of few other states to relook the report on the whole, it was decided by the GST Council that the GoM may relook into all the issues in the light of submissions placed before it by eliciting information from Goa, Tamilnadu and Telangana for their respective areas.

II. Submission of the stakeholders before GoM:

3. Following the decision of the GST Council for GoM to re-examine the issues, the GoM conducted stakeholder consultations via video-conferencing on 12th July, 2022 with the Casino Association of Goa, Turf Authorities of India, E-Gaming Federation (EGF) and Federation of India Fantasy Sports (FIFS). The industry presentations and written representations along with legal opinions of Shri Deepak Mishra (Ex. Chief Justice of India), Shri Anil Kumar (Judge (retd.) Allahabad High Court), Shri Harish Salve and M/s Lakshmikumaran & Sridharan are enclosed as Annexure II to VII. GoM members also conducted field visits to Bangalore Turf Club and casinos at Goa on 23rd and 24th July, 2022 and met with the trade and industry associations of all three sectors during the field visits.

3.1 The main thrust of the views expressed by the industry has been summarised below:

3.2 Online Gaming:

(i) Online games are games of skill. Therefore, it does not come under the category of ‘betting and gambling’.

(ii) Although the amount at stake in online games is an actionable claim, online games do not come under the category of actionable claims taxable under GST, as they do not fall under the category of ‘betting and gambling’.

(iii) The words betting and gambling in the phrase ‘betting and gambling’ should be read together in view of the recent Hon’ble High Court of Madras decision in Junglee Games, according to which GST is applicable only on such betting which is on gaming activities or on games of chance.

(iv) Only platform fee is received as consideration for the services provided by the online game operators. Hence, only this amount can be taxed under GST.

(v) It is ultra-vires the law to tax those goods/services for which the power to tax has not been given by the Parliament.

(vi) The representatives of online gaming industry emphasized that the recommendation of 28% GST on face value would increase tax by 1000% Moreover, multiple High Courts such as Bombay High Court in Gurdeep Singh Sacchar (Dream 11) case and Punjab and Haryana High Court in Varun Gumber case have held that the activities in online gaming fall in the category of games of skill.

(vii) The Central government is in the process of formulating laws and regulations for online gaming industry and an Inter-Ministerial Task Force (IMTF) has already been constituted. It was requested that status quo be maintained till report of that task force is brought out.

3.3 Race Courses:

(i) Horse racing and bets placed thereon are not lottery and therefore the only question is, whether horse racing is ‘betting and gambling’.

(ii) The Hon’ble Supreme Court in RMD Chamarbaugwala and Dr. Lakshmanan case has concluded that games of skill do not amount to gambling and that if substantial skill is involved despite an element of chance. it would be a game of skill and would not amount to gambling. the CGST Act 2017 does not define “betting and gambling” or a game of skill or chance. Therefore, the Supreme Court rulings on the same are valid.

(iii) The words betting and gambling appearing in Entry 34 of State List of the Constitution, are required to be read together and not separately. Only such betting which takes place on gambling activities is taxable. In other words, betting on horse racing, which is a game of skill, is actionable claim but not actionable claim in the form of ‘betting and gambling’ and is thus not taxable under GST.

3.4 Casinos:

(i) The activities in casinos are admittedly of the nature of betting and gambling and thus taxable.

(ii) The activities in a casino are complicated and unlike horse racing and lottery, where transactions are ticket-based, in casinos, transactions are player-based and take place on the table mostly. Bets are not placed at the time of purchase of tokens/chips but at the time when these chips are used/ placed for bet on tables. After the purchase of chips, bets can be placed for entire or lesser number of chips.

(iii) Instead of calculating the tax player-wise, it should be calculated table-wise and that actionable claim in case of casinos is that amount which corresponds to the value of the chips that remain with the table at the end of the day.

(iv) International practice is to tax casinos on the Gross Gaming Revenue (GGR), that is, the difference between the amounts of money players wager minus the amount that they win.

(v) They pay 50 to 55% of their earnings as revenue to the Government. COVID has impacted the casino industry badly and they are facing competition from online gambling as well.

(vi) Rule 31A(3) should not be applicable on Casinos and a separate rule needs to be introduced for the method of valuation of Casinos.

III. Deliberations of the GoM:

4. The deliberations of the GoM mainly revolved around two questions, namely, –

(i) Whether or not the activities in race courses and online gaming amount to betting and gambling in the light of various High Court and Supreme Court judgments.

(ii) How should the supplies of casinos, race courses and online gaming be valued; on the full-face value of bets placed or on GGR in case of casinos, the totalisator fee in race courses and platform fee/GGR in the case of online gaming.

5. The GoM deliberated upon these issues in detail in the third meeting of the GoM held on 12th July, 2022 via video conference, in the fourth meeting held on 5th September, 2022 at New Delhi and in the fifth meeting of the GoM held on 22nd November, 2022 via video conference.

6. During the discussions, a view was expressed that the activities under consideration are diverse and different in nature and to formulate a simple uniform formula to tax them is a challenging task. In this context, it was stated that while casinos and horse racing are activities which are conducted physically, online gaming is completely on the digital platform and clubbing these activities into one category and prescribing a uniform formula for their valuation may not be desirable. It was also viewed that the ‘contribution towards prize pool’ may be treated as supply not liable to levy of GST. However, there were also contrary views presented expressing the view that whether the activity happens physically or on the digital platform, the supply remains the same, that is, the supply of actionable claim in the form of betting and gambling and that the doctrine of ejusdem generis needs to be applied in this context. There cannot be any ambiguity that the intent of the GST laws is to levy tax on all kinds of actionable claims that fall under the class of “lottery, betting and gambling”.

7. The GoM noted that betting and gambling have not been defined in the GST laws and that there are contrasting judgments by various courts. The GoM observed that the Hon’ble supreme Court in Dr K R Lakshmanan case held that horse racing is a game of skill. It was also observed by the Bombay High Court in Gurdeep Singh Sacchar (Dream 11) case and the Punjab and Haryana High Court in Varun Gumber case that the activities in online gaming are in the category of games of skill. The GoM, however, observed that these judgments cited by the industry have been passed in the context of statutes of various States for regulating/prohibiting gaming activities and are not in the context of taxation, per se.

8. The Convenor requested the members of Gom to send their views in writing which could be presented to the Council. It was also decided to seek legal opinion.

9. Some observations made in the following court judgments were also brought to the notice of the GoM:

(i) In case of State Of Andhra Pradesh vs K. Satyanarayana & Ors 1968 AIR 825, Hon’ble Supreme Court has, inter alia, observed …… “Of course, if there is evidence of gambling in some other way or that the owner of the house or the club is making a profit or gain from the game of rummy or any other game played for stakes, the offence may be brought home. …”

(ii) In the case M J Sivani and Ors Vs Stake of Karnataka & ORs, 1995, the Hon’ble Supreme Court has, inter alia, observed, “Gaming, therefore, is an inclusive definition which includes a game of chance and skill combined or a pretended game of chance or of chance and skill combined …. Gaming is to play any game whether of skill or chance for money or money’s worth and the act is not less gaming because the game played is not in itself unlawful and whether it involved or did not involve skill…

“To game”, therefore, is to play any game, whether of skill or chance, for money or money’s worth.”

(iii) Hon’bel Supreme Court in the case of State of Karnataka & ORs, Vs. State of Meghalaya & Ors 2022, has observed, “The expression ‘betting and gambling’ is relatable to an activity which is in the nature of ‘betting and gambling’. Thus, all kinds and types of ‘betting and gambling’ fall within the subject of Entry 34 of List II. The expression ‘betting and gambling’ is thus a genus it includes several type or species of activities such as horse racing, wheeling and other local variations/forms of ‘betting and gambling’ activity.”

(iv) The Hon’ble Supreme Court vide order dated 06.03.2020 has stayed the Bombay High Court judgment the case of the State of Maharashtra vs. Gurdeep Singh Sachar SLP (CRIMINAL) 42282/2019 (Dream 11 case) wherein it was held that Dream 11 is a game of skill.

10. During the discussion in meetings, the following broad positions emerged:

(1) While there was like-mindedness amongst some members of the GoM that activities of casinos, horse racing and online gaming constitute betting and gambling and are taxable as supply of actionable claims in the form of betting and gambling, Goa expressed the view that the ‘contribution towards prize pool’ may be treated as supply not liable to levy of GST. Some of the GoM members also held the view that the contribution made by the players of online game towards the prize pool constitutes an Actionable Claim other than lottery, betting and gambling as the game is considered to be a game of skill and not game of game of chance. Thus, the said amount is explicitly covered at Para 6 of the Schedule III of CGST Act, 2017.

(2) Barring Goa, there was broad agreement on the rate of 28% to be applicable to these taxable activities. Goa has stated that “platform fee/service charge” charged for services provided by the platform company may be taxed at existing rate of 18%.

(3) There were strong differences of opinion on whether actionable claims of casinos, horse racing and online gaming should be taxed on full bet value or on GGR/platform fees. Divergent views and several points and counter points in favour and against taxing the supplies on GGR, the different mechanisms of arriving at GGR, difficulties in monitoring the compliance etc. were expressed by the members.

11. The possibility of seeking legal opinion was also explored by GoM. However, the same was not found feasible as it was seen as beyond the scope of Terms of Reference of GoM [Annexure VIII].

12. The views expressed by the members during the meetings and also submitted in writing (enclosed as Annexures IX to XV) are summarized as below:

A. Online Gaming:

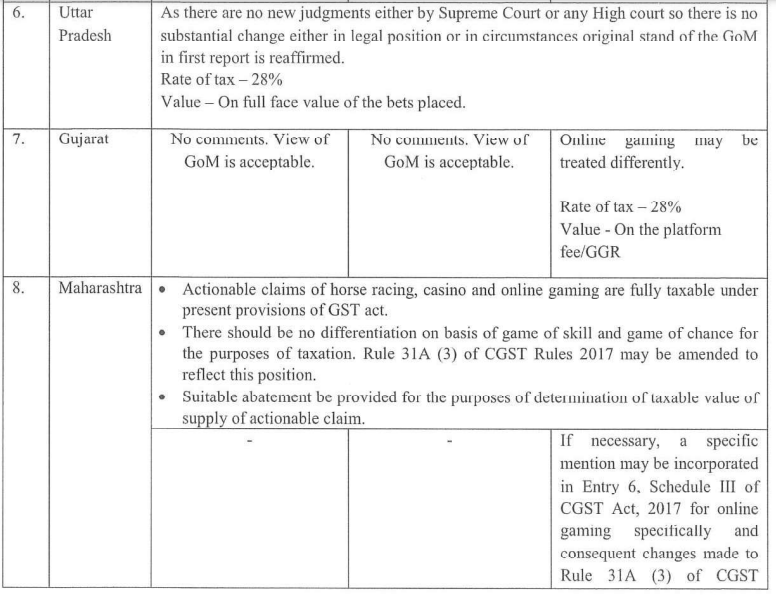

Gujarat has contended that online gaming is very different from other three forms i.e., lottery, casino and horse racing as the latter three are organized in physical form. However, in Online gaming both the supplier and recipient operate on virtual platform. Further the other three forms i.e., lottery, casino and horse racing may use partially manual records and cash transactions leaving scope for leakages, however, for online gaming, there are only online transactions and therefore, 100% transactions are recorded. Therefore, the point of similarity should not be used to put all these 4 categories into one basket. As far as rate of tax is concerned, Gujarat agreed that it could be 28%. Further that if full value is considered in case of online gaming, then the operators might move outside India and may supply such games from other countries like Singapore, Hong Kong, Maldives etc. In such circumstances, the country will not have any control on these online gaming activities. Therefore, Gujarat suggested that we should consider only service charge (platform fee) for taxation purpose.

Uttar Pradesh made the submission that online gaming has elements of both game of skill and game of chance. It is difficult to decide which of these two elements are in excess.

. As per the order given by the Hon’ble Gujarat High Court in the suit of Yashpalsinh Rajendrasinh … vs State Of Gujarat (SPECIAL CRIMINAL APPLICATION NO. 767 of 2020) on 22 September, 2020, betting on the performance of a player is a Game of Chance.

. In M.J. Sivani And Ors. vs State Of Karnataka And Ors (Appeal (civil) 4564 of 1995) on 17 April, 1995, it was held by the Hon’ble Supreme Court that it is not necessary to decide in terms of mathematical precision the relative proportion of chance or skill when deciding whether a game is a game of mere skill. Uttar Pradesh also put forth the argument that although there may be elements of skill in tasks such as selection of players etc., but in a real game, the performance of the selected player is a further event over which the participant who is placing the bet has no control and such a participant has equal chances for both gain and loss. So, in this way there is a wager/betting element in these games. Therefore, these games should be considered as a game of chance and the amount related to them is taxable due to being an actionable claim. The adverse effect on the youth in particular was highlighted as a grave issue of concern. In online games the activities such as collection of pool money, point allocation to the players, gradation of the players’ points so allocated, deciding the winner, distribution of prize money among the players are solely controlled by the game operator. There is no mechanism that can be devised by States for verification of such activities. Hence, in interest of revenue, tax on total pool money (which is aggregate of face value of bets placed) is the only source available for fixing as basis of taxation. Under section 15(5) of the CGST Act, 2017, the Government has the power to determine the value of supply after the recommendations of the Council, with the overriding clause (Non-obstante clause). Therefore, in the cases of Online Gaming, there is no legal impediment in levying pool money as the value of supply. The power to levy tax on actionable claims like lottery, betting and gambling has been given by the Parliament to the States and the Centre.

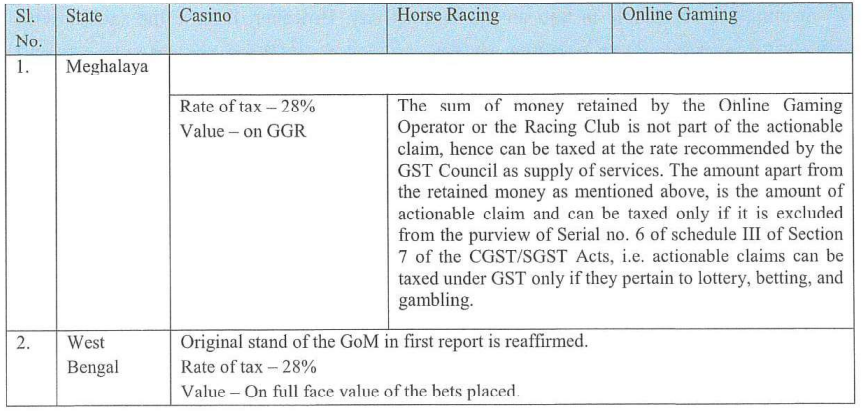

West Bengal reiterated its original stand as in the earlier Report submitted by GoM and reaffirmed that all these activities whether online gaming or horse racing or casinos should be taxed at 28% on full value of bets placed.

Tamil Nadu opined that if a clear-cut view is taken that all three- casinos, horse-racing and online gaming are actionable claims of betting and gambling as games of chance, the recommendations of the GoM placed before the GST Council in the 47th Council meeting held on 28th & 29th June, 2022 are acceptable in toto. However, in case a view is taken that horse racing and online gaming are games of skill and not actionable claims of betting and gamibling, taxing the Gross Gaming Revenue (GGR) at 28% should be adopted and mechanism for determining the taxable value may be as follows:

(i) There shall be a mechanism to segregate and split at inception, the receipts amount directly into ‘operator account’ and ‘escrow account’. The online gaming company shall divide the receipts into the said two accounts. The ‘operator account’ shall hold the purveyor’s portion of the money and the ‘escrow account’ shall hold the prize money for eventual payout.

(ii) All winnings shall be paid out of escrow account and need not be subjected to GST. However, all such payments will be subject to direct tax including TDS applicable at 30%.

Telangana stated that the question of whether the online games are ‘games of skill’ or ‘games of chance’ is crucial. If an activity can be classified as betting and gambling then the earlier recommendations made by this GoM which were placed before the GST Council in its 47th meeting are acceptable in toto on the said activity. However, in case the said activity does not fit into betting and gambling, tax may be levied at highest rate and value may be arrived at by following the existing provisions of the GST Act.

Goa stated that as per the submissions of the trade and industry, online skill gaming platforms collect amount from players which is split as “platform fee/service charge” and “contribution towards prize pool” and bifurcation of the amount collected is communicated to all the players through the ‘Terms & Conditions’ available on the platform’s website. The “platform fee/service charge” charged for services provided by the platform company are taxed at 18%, whereas the amount collected as “contribution towards prize pool” is treated as supply which is not liable for levy of GST. The contribution made by the players of online game towards the prize pool constitutes as actionable claim other than lottery, betting and gambling as they are considered to be game of skill and not a game of chance. The said amount is explicitly covered at para 6 of Schedule III of CGST Act, 2017 and therefore, is not leviable to GST. Therefore, the “platform fee/service charge” collected by online skill gaming platform may be continued to be taxed at existing rate or as may be decided by the GST Council and amount collected as “contribution towards prize pool” may be treated as supply not liable for levy of GST.

Maharashtra conveyed that their views that were expressed during the GoM meeting held on 22.11.2022 may be taken on record. Maharashtra expressed the view that actionable claims of online gaming are fully taxable under present provisions of GST Acts and are covered under Entry 6 of Schedule III. Judgments cited by industry emanate from regulatory aspect under prevention of Gambling Acts & various Police Acts and no specific judgment on taxability aspect has been cited. There should be no differentiation on basis of game of skill and game of chance for the purposes of taxation. Accordingly, Rule 31A (3) of CGST Rules, 2017 may be amended to reflect this position. If necessary, a specific mention may be incorporated in Schedule III entry 6, for online gaming and consequent inclusions may be made to Rule 31A (3) of CGST Rules, 2017. Further, as Government of India has formed an inter-ministerial group to study the regulation on online gaming industry, the fear expressed by the industry that certain activities will shift to grey market and outside the country can be taken care of by suitable regulation. Taxation provision on the lines of Online Information Database Access and Retrieval (OIDAR) services may be considered. Suitable abatement may be provided for the purposes of determination of taxable value of supply of actionable claim.

Meghalaya stated that the interactions made with the industry representatives from race courses and online gaming highlighted that both horse racing and online gaming are games of skill and not games of chance and that it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST, only if they pertain to lottery, betting and gambling, duly substantiated and supported by various court rulings, which have held that games where there is preponderance of skill do not amount to gambling and that the betting and gambling have to be read together, i. e. tax can be levied only on betting on the game of chance and not on the game of skill. The sum of money retained by the Online Gaming Operator or the Racing Club is not part of the actionable claim, hence can be taxed at the rate recommended by the GST Council as supply of services. The amount apart from the retained money as mentioned above, is the amount of actionable claim and can be taxed only if it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST only if they pertain to lottery, betting, and gambling.

13. The GoM also noted that the Union Government had also set up an Inter-Ministerial Task Force (IMTF) for regulation of online gaming, with Ministry of Electronics and Information Technology (MeitY), as the Convener. However, the broad view in the GoM was that the IMTF has been set up for making recommendations on regulation of online gaming and therefore, the same has no bearing on taxation of online gaming.

B. Race Courses:

West Bengal has stated that the judgment of Hon’ble Supreme Court in K R Lakshmanan case for horse racing was in respect of Madras City Police Act, 1988 and Madras Gaming Act, 1930 and not in respect of taxing statute. Therefore, argument that horse racing cannot be classified as betting and gambling on the grounds that they are games of skill is incorrect. Further, the following have been stated:

. Horse racing is covered within the expression ‘betting and gambling’ as per the judgment of the Hon’ble Supreme Court in State of Karnataka Vs. State of Meghalaya case 2022.

. Common Parlance Test is an established norm for deciding taxability of goods in any taxation statute and needs to be considered in this context.

. Doctrine of “Ejusdem Generis” meaning ” of the same kind and nature” needs to be applied in this context. There cannot be any ambiguity that the intent of the GST laws is to levy tax on all kinds of actionable claims that fall under the class of lottery, betting and gambling.

. It is not only difficult but impossible to ascertain the accurate percentage of skill or percentage of chance that is involved in a particular game and therefore, it would be absolutely inappropriate to classify all kinds of such activities as game of skill. The Ho’ble Supreme Court judgments in M.J Sivani Vs State of Karnataka 1995 and in State of Andhra Pradesh Vs K Satyanarayana 1968 have been cited in support.

As regards the principle of valuation in respect of horse racing, West Bengal has expressed the view that deciding to tax actionable claims in the form of lottery, betting and gambling was a conscious of the GST Council. Further, Rule 31A of the GST rules has already been upheld by the Hon’ble Supreme Court in Skill Lotto Solutions Pvt. Ltd. Vs UOI 2020. The principle of valuation in Rule 31A of the GST rules covers not only lottery but also horse racing and betting and gambling.

Uttar Pradesh stated that in pre-GST regime horse races were taxable under different state taxation laws and multiple taxes were levied such as entry tax, service tax by Centre on license fee and tote commission, embedded excise duty and taxes. Further, though for a player who is participating in horse racing it may be a game of chance. Cases of Yashpalsinh Rajendrasinh & ors vs State Of Gujarat (Special Criminal Application No. 767 of 2020) on 22 September, 2020 in Gujarat High Court and case of Public Prosecutor v. Veraj Lal Sheth, (AIR 1915 Mad 164) in Madras High Court have been cited in support of the above statement. Moreover, the race course authorities do not conduct any test/examination to examine the skills of any person who places bets on horses and the entry to the race course does not need any special knowledge of any particular field related to horse racing, a common man having no knowledge or experience of horse racing can go to the race course and may place bet based on any feature/quality of the horse such as appearance, coat colour, hairs etc. Therefore, horse racing is a game of skill but betting on result of horse racing is a game of chance.

Tamil Nadu opined that if a clear-cut view is taken that all three-casinos, horse-racing and online gaming are actionable claims of betting and gambling as games of chance, the recommendations of the GoM placed before the GST Council in the 47th Council meeting held on 28th & 29th June, 2022 are acceptable in toto. However, in case a view is taken that horse racing and online gaming is a game of skill and not actionable claim of betting and gambling, taxing the Gross Gaming Revenue (GGR) at 28% should be adopted and mechanism for determining the taxable value may be as follow:

(i) There shall be a mechanism to segregate and split at inception, the receipts amount directly into ‘operator account’ and ‘escrow account’. The race-club shall divide the receipts into the said two accounts. The ‘operator account’ shall hold the purveyor’s portion of the money and the ‘escrow account’ shall hold the prize money for eventual payout.

(ii) All winnings shall be paid out of escrow account and need not be subjected to GST. However, all such payments will be subject to direct tax including TDS applicable at 30%.

Telangana stated that the question of whether horse racing are ‘games of skill’ or ‘games of chance’ are crucial. If an activity can be classified as betting and gambling then the earlier recommendations made by this GoM which were placed before the GST Council in its 47th meeting are acceptable in toto on the said activity. However, in case the said activity does not fit into betting and gambling, tax may be levied at highest rate and value may be arrived by following the existing provisions of the GST Act.

Goa stated that services of betting on horse racing were not available in the state of Goa and therefore, there were no comments to offer on the issue.

Gujarat mentioned that as the activity of horse racing does not take place in Gujarat, there are no specific comments to offer and the final decision of GoM is acceptable.

Maharashtra expressed the views that actionable claims of horse racing are fully taxable under present provisions of GST acts and are covered under Entry 6 of of Schedule III. judgments cited by industry emanate from regulatory aspect under prevention of gambling acts & various police acts and on specific judgment on taxability aspect has been cited. There should be no differentiation on basis of game of skill and game of chance for the purposes of taxation. Accordingly, Rule 31A (3) of CGST Rules, 2017 may be amended to reflect this position. Suitable abatement may be provided for the purposes of determination of taxable value of supply of actionable claim.

Meghalaya stated that the interactions made with the industry representatives from race courses and online gaming highlighted that both horse racing and online gaming are games of skill and not games of chance and that it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST, only if they pertain to lottery, betting and gambling, duly substantiated and supported by various court rulings, which have held that games where there is preponderance of skill do not amount to gambling and that the betting and gambling have to be read together, i.e. tax can be levied only on betting on the game of chance and not on the game of skill. The sum of money retained by the Online Gaming Operator or the Racing Club is not part of the actionable claim, hence can be taxed at the rate recommended by the GST Council as supply of services. The amount apart from the retained money as mentioned above, is the amount of actionable claim and can be taxed only if it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST only if they pertain to lottery, betting, and gambling.

C. Casinos:

The GoM observed that as acknowledged by the industry itself, there is no contest to the fact that there is supply of actionable claims which is taxable as per Entry 6 of Schedule III to the CGST Act, 2017. However, the issue is whether the tax should be levied on full face value of chips at the time of sale of chips to individual players or whether the tax should be levied on GGR.

Goa stated that it is the major State affected with other States being Sikkim and Meghalaya. The practice all over the world is to tax the casinos on gross gaming revenue and that the best international practices in GST should be adopted. If we tax full value of betting, the tax will be more than what the casinos earn. This is impractical and will close down the businesses and if the businesses close down the Government will not get any revenue and will also push the business into the grey market. It is the gross gaming revenue (GGR) of the casinos which needs to be taxed. The cardinal principle of GST has been that it has to align to pre-GST levels. In pre-GST, entertainment tax @ 15% and tax on GGR for sale of chips was levied. Goa is a tourism dependent state and based on a conservation estimate, almost 60% of inbound flights to Goa bring tourism (both domestic and international) who come to Goa just for the casinos. Further, an unfavourable decision for the casinos would also adversely impact the entertainment industry in Goa. Further, Goa also stated that there is no objection to levy of tax on entry fee in Casinos as suggested by GoM earlier. However, the taxable value of supply of actionable claims may be based on the GGR of the casino as it is a certain and efficient measure of levy and has a cogent nexus with the supply of actionable claims. Insertion of a separate rule for casinos to levy GST on GGR may be considered.

Meghalaya proposed that highest rate of tax i.e., 28% should be levied on GGR, following the table-wise model of revenue and not stake money wagered in casino. Further, the chips won in subsequent rounds should not be further subjected to tax as recommended by GoM in its first report. As proposed in the first report of GoM, GST @ 28% should be levied on entry fee, which compulsorily includes price of one or more supplies bundled together viz. food, non-alcoholic beverages etc. However, optional supplies made independently of the entry fee shall be taxed at the rates as applicable on such supplied. Liquor served inside casino should be taxed as per the VAT rate of respective State Government.

West Bengal stated that deciding to tax all actionable claims in the form of lottery, betting and gambling was a conscious decision of the GST Council. The Rule 31A of CGST Rules, 2017 governing the principle of valuation of such actionable claims has been upheld by the Hon’ble Supreme Court in Skill Lotto case.

As regards the request of trade to follow international practice, wherein tax is levied on platform fees or GGR, the observations of the Hom’ble Supreme Court in Skill Lotto Solutions Pvt. Ltd. Vs UOI 2020 case is relevant. The apex court observed that the taxing policy and the taxing statute of various countries are different which are in accordance with taxing regime suitable and applicable in different countries. Therefore, it needs to be noted that every country is different and has different priorities and there is no reason to adopt international practice selectively. Further, doctrine of ejusdem generis does not permit to extend any separate treatment to any of these activities than what has been extended in case of lottery. It has also been stated that the GST Council has concluded after several rounds of discussion that there cannot be two rates for one category of goods. Therefore, when there is a settled stand of the GST Council, there cannot be any reason to deviate from it and uniform valuation principles and rate for all such activities considered as “actionable claims” must be adopted. With regard to the apprehensions that the industry will shut down completely, it was stated that similar apprehensions that the industry will shut down completely, it was stated that similar apprehensions were raised when it was decided by the GST Council to tax lotteries at 28% but the revenues from lottery business have been increasing even after such a decision.

Gujarat mentioned that as the activity of casino does not take place in Gujarat, there are no specific comments to offer and the final decision of GoM is acceptable.

Tamil Nadu reiterated that if a clear-cut view is taken that all three-casinos, horse-racing and online gaming are actionable claims of betting and gambling as games of chance, the recommendations of the GoM placed before the GST Council in the 47th Council meeting held on 28th & 29th June, 2022 are acceptable in toto. No specific view was provided on Casinos.

Telangana stated that if an activity can be classified as betting and gambling then the earlier recommendations made by this GoM which were placed before the GST Council in its 47th meeting are acceptable in toto on the said activity. However, in case the said activity does not fit into betting and gambling, tax may be levied at highest rate and value may be arrived by following the existing provisions of the GST Act.

Uttar Pradesh stated that taxation on basis of GGR is neither practical nor legally feasible. So, the previous recommendation of GoM to impose one-time tax at the rate of 28% at full value is a practical solution. If only GGR is taxed, then the revenue receipt will be very less. In GGR based tax it is possible that even after several cycle of supplies no revenue for Government may be generated. Sikkim, which also has operational casinos has also opposed the taxation on GGR basis and have stated that in GGR system, the tax payable becomes nil when the casino owner loses in total to the players. In this aspect the GGR system is not in parlance with the basis principle of levy. It does not generate tax despite of abundant supply and consumption of service in such case. If a player after playing several games returns with the same amount of chips as purchased by him, it will be impossible to trace that whether or not he has played a game on any table. Thus, in such a case there will be a supply but no tax will accrue to the Government.

In the present legal framework under GST, every time a bet is placed on the table there will be a taxable supply. It is possible that a single payment of money may generate several cycles of game and accordingly the tax liability. However, the GoM had already agreed in its first report that it would be difficult to monitor every bet on each and every table. Therefore, considering the plight of the casino industry the initial recommendation that the chips won in subsequent rounds should not be further subjected to tax may be agreed to.

Maharashtra expressed that actionable claims of casinos are fully taxable under present provisions of GST acts and are covered under Entry 6 of Schedule III. Judgments cited by industry emanate from regulatory aspect under prevention of gambling acts & various police acts and no specific judgment on taxability aspect has been cited. There should be no differentiation on basis of game of skill and game of chance for the purposes of taxation. Accordingly, Rule 31A (3) of CGST Rules, 2017 may be amended to reflect this position. Suitable abetment may be provided for the purposes of determination of taxable value of supply of actionable claim.

Summary:

14. The views of GoM have been tabulated in brief as under:

IV. Recommendations:

15. The GoM, after wide stakeholder consultations and taking into account views of the GoM Members, makes the following recommendations:-

Online Gaming:

(i) As regards taxability of activities in online gaming, GoM could not reach a consensus. Goa has expressed the view that the ‘contribution towards prize pool’ may be treated as supply not liable to levy of GST. West Bengal and Uttar Pradesh have expressed the view that as recommended by the GoM in the report submitted to the Council in its 47th meeting, the activities of online gaming may be taxed as supply of actionable claims in the form of betting and gambling irrespective of whether the online games involve betting on a game of skill or a game of chance. Tamil Nadu has expressed that in case a view is taken that horse racing and online gaming are games of skill and not actionable claims of betting and gambling, taxing the Gross Gaming Revenue (GGR) at 28% should be adopted and mechanism for determining the taxable value was also proposed.

(ii) There was broad agreement that the said supplies may be taxed at the highest rate of 28%. However, no consensus could be reached as Goa has suggested that platform fees/service charge may be taxed at existing rate of 18%.

(iii) As regards valuation, the GoM could not reach a consensus. While Uttar Pradesh and West Bengal were of the view that the said activity may be taxed on the full value of bets placed on online games, Gujarat and Goa expressed the view that the same may be taxed on the platform fees. Maharashtra has proposed that suitable abatement be provided for the purposes of determination of taxable value of supply of actionable claim.

Race Courses:

(i) There was no broad consensus that the activities of betting on horse racing in race courses may be taxed as supply of actionable claims in the form of betting and gambling, though there was an understanding amongst most members that it may be taxed at the highest rate of 28%.

(ii) As regards valuation, some members held that the value of such supplies shall be 100% of the face value of the bets placed or the amount paid into the totalisator. Tamil Nadu has expressed the view that in case it is held that horse racing and online gaming are games of skill and not actionable claims of betting and gambling, taxing the Gross Gaming Revenue (GGR) at 28% should be adopted and suggested a mechanism for determining the taxable value.

Casinos:

(i) There was consensus that activities in casinos are in the nature of betting and gambling and hence, it is a taxable supply of actionable claims.

(ii) There was also no disagreement on the rate of tax at 28%.

(iii) The GoM could not reach a consensus on valuation for purposes of taxing the activity. While Uttar Pradesh and West Bengal were of the view that the said activity may be taxed on full face value of chips at the time of sale of chips to individual players and once GST is levied on purchase of chips /coins (on face value), no further GST to apply on the value of bets placed in each round of betting including those played with winnings of previous rounds. Goa and Meghalaya expressed the view that the same may be taxed on the Gross Gaming Revenue. Maharashtra has, while agreeing on the rate at 28% on the full value of bets but suggested suitable abatement be provided for the purposes of determination of taxable value of supply of actionable claim.

(iv) As regards, GST on entry fee to casinos, GST at the rate of 28% is leviable on the services by way of access/entry to Casinos on payment of consideration/entry fee which compulsorily includes price of one or more other supplies such as food, beverages etc.; this being a mixed supply. However, optional supplies made independently of the entry ticket shall be taxed at the rates as applicable on such supplies.

V. Conclusion:

16. In pursuance of the directions given by GST Council in its 47th meeting, wide consultations with the stakeholders along with study visits were undertaken by the GoM. Considering the complexity of the issues involved in these three sectors, which are not comparable. the views of the members were divergent in nature and GoM could not reach the consensus. The views of each member State are included in the report individually and giving due respect to all the valuable views and insights shared by all members, the report has been finalised with a request made by the members to the Hon’ble Convener to express his specific views/opinion on the subject-matter.

17. Upon meeting with the stakeholders and delving into issues raised, there appears to be a difference made between the nature of the games on which GST is sought to be levied i.e., games of chance (those games that are solely based on luck and chance) and games of skill (those games that are primarily and substantially based on skill). The stakeholders have impressed upon us that the Hon’ble Supreme Court, in several judgements has recognized that games that are categorized as games of skill ought not to be made susceptible to taxation in a similar way as games of chance are. The following are some of the judgements that have held so:-

(a) State of Bombay versus R.M.D. Chamarbaugwala and Others – AIR 1957 SC 699. where the Supreme Court has recognized that activities that possessed even a “scintilla of skill” that was required for winning, could not be recognized as a game of chance and therefore, could not be a gambling activity.

(b) R.M.D Chamarbaugwala and Anr. versus Union of India – 1957 I SCR 930, where the Supreme Court has recognized that “competitions in which success depends to a substantial extent on skill and competitions in which it does not so depend, form two distinct and separate categories.”

18. This difference between activities that are categorized as games of skill versus those that are so categorized as games of chance is relevant, inasmuch as the activity of horse racing and the bets placed on such races have been recognized by the Hon’ble Supreme Court, in the case of Dr. K.R. Lakshmanan versus State of Tamil Nadu and Anr. – 1996 (2) SCC 226, as being a game of skill, in the breeding, selection and training of the racehorse, the disceming in the selection and skill of the jockey as also the skill and discretion involved in the selection of a potential winning horse and the placing of the bet.

19. The difference between games of skill and chance is significant in light of the provisions of the CGST Act, 2017, wherein while “actionable claims” have been stated as being outside the purview of taxation, an exception has been created in the cases of “lottery, betting and gambling“. The Hon’ble Supreme Court, in the above cited cases, has found activities that are primarily dependent on skill for success, as not being gambling/betting activities, which would include horse racing as well.

20. The sense/perception which emerges out of such wide interactions is that both horse racing and online gaming are games of skill and not games of chance and that it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST, only if they pertain to lottery, betting and gambling, duly substantiated and supported by various court rulings, which have held that games where there is preponderance of skill do not amount to gambling and that the betting and gambling have to be read together, i.e. tax can be levied only on betting on the game of chance and not on the game of skill.

21. Under Section 9 of the CGST/SGST Acts, the Council is empowered to recommend the rates of tax on the taxable goods and services and prescribe the manner (read valuation) for levy of GST.

22. It is understood that during horse racing, consumers place bets or wagers. Race courses act as the service provider for the wagering transaction. The wagers are placed through a totalisator, which pools the wagers. The commission for offering the services are retained and the balance amount is kept aside as a pool for prize winning. Similar is the case with online gaming, where the gaming operator provides the online platform for gaming and part of the pool money is retained by the operator as platform fee/facilitation fee/membership fee/access fee and the remaining balance becomes the stake money.

23. The sum of money retained by the Online Gaming Operator or the Racing Club is not part of the actionable claim, hence can be taxed at the rate recommended by the GST Council as supply of services.

24. The amount apart from the retained money as mentioned above, is the amount of actionable claim and can be taxed only if it is excluded from the purview of Serial no. 6 of schedule III of Section 7 of the CGST/SGST Acts, i.e. actionable claims can be taxed under GST only if they pertain to lottery, betting, and gambling.

25. In conclusion, the Hon’ble Convener of the GoM opines that the levy of GST may be only on the GGR in case of Casinos and part of transaction what is relatable to service, i.e. the commission/platform fee/Gross Gaming Revenue in case of race Courses and Online Gaming coupled with a desirable special mechanism to carve out Escrow Account wherein the prize money is pooled in, for the payouts to the winners, segregated from the amount collected/retained toward commission/platform fee, for the purpose of easy tax administration and considering the cascading effect of taxation not only on the main sectors of Casinos, Race coursed and Online gaming, but also on the ancillary section and industries like tourism, transport, entertainment, sports etc. for its viability and long term growth prospects in the larger interest of our economy. However, since no consensus could be reached on whether the activities of online gaming, horse racing and casinos should be taxed at 28% on the full-face value of bets placed or on the GGR, the GoM recommends that GST Council may decide.

****

1. Background:

1.1 Betting and gambling taxes have been subsumed in GST. Entry 62 of State List in the 7th Schedule of the Constitution which empowered the States to levy taxes on betting and gambling has been substituted by another entry by the 101st amendment Act to the Constitution. Subsuming of betting & gambling taxes along with VAT & other State levies and Services tax, as was imposed by Centre on service aspect of these activities, in GST, meant that entire gamut of these activities is subjected to GST.

1.2 Supply of actionable claims by way of both betting and gambling has been declared to be taxable in GST law. Goods have been defined to include actionable claims.

1.3 Accordingly, lottery, betting and gambling activities in casinos, horse racing and online gaming etc. have been subjected to GST. Certain issues have arisen as regards taxability. rate and valuation of these activities under GST. These issues have been widely litigated. Issues related to taxation of lottery have now been settled. Lottery which was earlier taxed at dual rates, depending on whether it was State-run or State-authorised, is now taxed at the single highest rate@ 28% on full face value as recommended by the earlier GoM on lottery. The challenge to levy of GST on lottery at full face value has been set aside by the Hon’ble Supreme Court in the case of Skill Lotto.

1.4 However, disputes remained in other arenas of betting and gambling. The questions raised by different sections of the stakeholders include whether a particular activity or game is an activity of skill or chance and whether it constitutes an actionable claim. If it is an actionable claim, whether it is a taxable actionable claim or outside the scope of GST or whether it is merely a supply of service. Related to these are the questions of their taxability, classification and the rates of GST applicable. The other major bone of contention is whether they should be taxed at full value of bets or wagers or only on the margin which the organizers get to retain after paying out the prizes to the participating players. It has been argued that these activities should be taxed on Gross Gaming Revenue (GGR) or margin instead of imposition of tax on the entire bet value (which is inclusive of Prize Money/pool). These matters have been extensively litigated.

1.5 It is in this background that the GST Council recommended in the 42nd meeting that a new GoM be constituted to look into the issues related to taxation of casinos, horse racing and online gaming.

2. Constitution & Terms of Reference of GoM on Casinos, Race Courses and Online Gaming:

2.1 As recommended by the GST Council in its 42nd meeting held on 5th and 12th October, 2020, a Group of Ministers (GoM) on Casinos, Race courses and Online Gaming was constituted vide Office Memorandum dated 24.05.2021 [Annexure-A] with following Terms of Reference:

a. To examine the issue of valuation of services provided by Casinos, Race courses and online gaming portals and taxability of certain transactions in a casino, with reference to the current legal provisions and orders of Courts on related matters.

b. To examine whether any change is required in the legal provisions to adopt any better means of valuation of these services.

c. To examine the administration of such valuation provisions if an alternative means of valuation is recommended.

d. To examine the impact on other similarly placed services like lottery.

2.2 In the 45th meeting of the GST Council, held on the 17th September, 2021, the Council viewed that the said GoM may examine all contentious issues, including around rates, involved in online gaming, horse racing and casinos.

2.3 On 10th February 2022, GoM has been reconstituted [Annexure-B] with Chief Minister of Meghalaya as Convener with the same Terms of Reference. The reconstituted membership of the GoM is as follows:

Table 1: Members of reconstituted GoM

3. Issues before GoM:

3.1 The Gom observed that the following issues are referred to the GoM for consideration :

i. Valuation, that is, whether the tax should be levied on entire amount charged for betting/gambling/online gaming or only on the commission or earnings of the service provider or platform fee.

ii. Rate of tax that should apply on such activities.

iii. Impact of adopting different valuation methods for taxing casinos, horse racing and online gaming, on other activities, particularly, lottery.

iv. Legal provisions, that is, whether the recommendations of GoM satisfy the legal framework or not?

4. Statutory and legal framework:

4.1 Relevant Acts: The relevant Acts are the Central Goods & Services Act, 2017, Integrated Goods and Services Tax Act, 2017 and the corresponding State/UT GST Acts.

4.2 Statutory provisions relating to Actionable claim:

4.2.1 Actionable claims have been treated as goods in GST. Goods have been defined to include actionable claims:

“Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply. [Section 2(52) of the CGST Act, 2017]

4.2.2 “Actionable claims” have been defined in section 2(1) of the CGST Act/SGST Acts, 2017 as below:

“Actionable claim shall have the same meaning as assigned to it in section 3 of the Transfer of Property Act, 1882;”

[Section 3 of Transfer of Property Act 1882 reads as below:

“actionable claim” means a claim to any debt, other than a debt secured by mortgage of immoveable property or by hypothecation or pledge of moveable property, or to any beneficial interest in moveable property not in the possession, either actual or constructive, of the claimant, which the Civil Courts recognise as affording grounds for relief, whether such debt or beneficial interest be existent, accruing, conditional or contingent;”

4.2.3 Further, Schedule III of the CGST Act, 2017 and respective SGST Acts enlists the activities which are considered neither as a supply of goods nor as a supply of service.

“Schedule III: ACTIVITIES OR TRANSACTIONS WHICH SHALL BE TREATED NEITHR AS A SUPPLY OF GOODS NOR A SUPPLY OF SERVICES

6. Actionable claims, other than lottery, betting and gambling.”

Accordingly, the actionable claim with respect to lottery, betting and gambling is taxable.

4.3 Services involved in these activities:

4.3.1 Besides actionable claim, these activities entail supply of services; say by way of organising, distribution, facilitation, conducting etc. While in activities like horse racing, casino, lottery etc., there is absolute clarity as regards classification of these services, certain doubts remain as regards classification of services involved in online gaming, i.e., heading 9996 vs 9984 of Service Accounting Code (SAC). This classification has bearing to the rates that would apply to the corresponding activities. For example, online gaming supplier sites claim that their services are of operating the portal, and hence online content/information technology classifiable under heading 9984 of S.A.C. (Telecommunications, broadcasting and information supply services). Competing SAC code is 9996, which, inter alia covers recreational and sporting services. The scope of these two SAC codes is given as below:

4.3.2 Explanatory notes to the relevant S.A.C.:

I. Heading 9996: Recreational, cultural and sporting activities

Explanatory Note to 9996:

* 999692: Gambling and betting services including similar online services This service code includes:

i. on-line gambling services

ii. on-line games involving betting/gambling

iii. off-track betting

iv. casino and gambling house services

v. gambling slot machine services

vi. other similar services

* 999694: Lottery services

This service code includes organization, distribution and selling services of lotteries, lottos and other similar items. Thus , sub-heading 999692 includes gambling and betting services including similar online services. Online gaming involving betting services is specifically included in this sub-heading as is evident from Explanatory Notes to SAC.

II. Heading 9984: Telecommunications, broadcasting and information supply services

99843: online content services

998439: Other on-line contents nowhere else classified

Explanatory Notes to SAC 998439: Other on-line content n. e. c.

This service code includes games that are intended to be played on the Internet such as role-playing games (RPGs), strategy games, action games, card games, children’s games; software that is intended to be executed on-line, except game software; mature theme, sexually explicit content published or broadcast over the Internet including graphics, live feeds, interactive performances and virtual activities; content provided on web search portals, i.e. extensive databases of Internet addresses and content in an easily searchable format; statistics or other information, including streamed news; other on-line content not included above such as greeting cards, jokes, cartoons, graphics, maps

Note: Payment may be by subscription, membership fee, pay-per-play or pay-per-view.

This service code does not include:

-software downloads, cf. 998434

-on-line gambling services, cf. 999692

-adult content in on-line newspapers, periodicals,

books, directories, cf. 998431

4.4 GST Rate structure:

Table 2: Actionable claim (Goods)

Table 3: Services involved in these activities

[Both SACs 9996 and 9984 are discussed below in view of doubts raised regarding classification of services in online gaming]

4.5 Valuation of supplies of these activities:

4.5.1 Valuation of taxable supplies is governed by section 15 of the CGST Act, 2017. As per section 15(1), the valuation of a supply shall be transaction value i. e., price actually paid or payable for the said supply. Relevant provisions are reproduced for ready reference as follows:

“Section 15: Value of Taxable Supply.-

(1) The value of a supply of goods or services or both shall be the transaction value, which is the price actually paid or payable for the said supply of goods or services or both where the supplier and the recipient of the supply are not related and the price is the sole consideration for the supply.

(2) The value of supply shall include-

(a) any taxes, duties, cesses, fees and charges levied under any law for the time being in force other than this Act, the State Goods and Services Tax Act, the Union Territory Goods and Services Tax Act and the Goods and Services Tax (Compensation to States) Act, if charged separately by the supplier:

(b) any amount that the supplier is liable to pay in relation to such supply but which has been incurred by the recipient of the supply and not included in the price actually paid or payable for the goods or services or both;

(c) incidental expenses, including commission and packing, charged by the supplier to the recipient of a supply and any amount charged for anything done by the supplier in respect of the supply of goods or services or both at the time of, or before delivery of goods or supply of services;

(d) interest or late fee or penalty for delayed payment of any consideration for any supply; and

(e) subsidies directly linked to the price excluding subsidies provided by the Central Government and State Governments.

Explanation.- For the purposes of this sub-section, the amount of subsidy shall be included in the value of supply of the supplier who receives the subsidy.

(3) The value of the supply shall not include any discount which is given

(a) Before or at the time of the supply if such discount has been duly recorded in the invoice issued in respect of such supply; and

(b) after the supply has been effected, if-

(i) such discount is established in terms of an agreement entered into at or before the time of such supply and specifically linked to relevant invoices; and

(ii) input tax credit as is attributable to the discount on the basis of document issued by the supplier has been reversed by the recipient of the supply.

(4) where the value of the supply of goods or services or both cannot be determined under sub-section (1), the same shall be determined in such manner as may be prescribed.

(5) Notwithstanding anything contained in sub-section (1) or sub-section (4), the value of such supplies as may be notified by the Government on the recommendations of the Council shall be determined in such manner as may be prescribed.”

4.5.2 Section 15(5) confers power on the Government to provide that value of such supplies as may be notified by the Government on the recommendations of the Council shall be determined in such manner as may be prescribed. Accordingly, in exercise of this power, rule 31A of CGST/SGST Rules has been prescribed as below:

Rule 31A. Value of supply in case of lottery, betting, gambling and horse racing.-

(1) Notwithstanding anything contained in the provisions of this Chapter, the value in respect of supplies specified below shall be determined in the manner provided hereinafter.

(2) The value of supply of lottery shall be deemed to be 100/128 of the face value of ticket or of the price as notified in the Official Gazette by the Organising State, whichever is higher.

Explanation:- For the purposes of this sub-rule, the expression “Organising State” has the same meaning as assigned to it in clause (f) of sub-rule (1) of rule 2 of the Lotteries (Regulation) Rules, 2010.

(3) The value of supply of actionable claim in the form of chance to win in betting gambling or horse racing in a race club shall be 100% of the face value of the bet or the amount paid into the totalisator.

4.6 Earlier clarifications issued in the matter:

4.6.1 Circular 27/01/2018 – GST dated 04.01.2018 has been issued clarifying inter-alia on valuation of services by horse racing club and casinos as follows:

GST at the rate of 28% would apply on entry to casinos as well as on betting/gambling services being provided by casinos on the transaction value of betting, that is, the total bet value in addition to GST levy on any other services being provided by the casinos (such as services by way of supply of food/drinks etc. at the casinos). Betting, in pre-GST regime, was subjected to betting tax, on full bet value.

Further, GST would be leviable on entire bet value, that is, total of face value of any or all bets paid into the totalisator or placed with licensed bookmakers, as the case may be. IIIustration: If entries bet value is Rs 100/-, GST leviable will be Rs. 28/-.

5. Jurisprudence & Court Cases:

5.1 Issues raised in respect of lottery, race course, gambling, betting, online gaming are intertwined. The Courts have examined these issues in detail and certain issues have been finally settled while a few continue to be the subject matter of litigation. Some of the relevant cases are:

Sunrise Associates Vs Govt. of NCT of Delhi & Ors- (2006) 5 SCC 603(SC): In this case, the issue before the Hon’ble Court was -whether the lottery tickets were goods and were liable to sales tax as decided by the Hon’ble High Court considering the aspect that two rights involved in lottery (i) the right to participate in the lottery draw, and (ii) the right to win the prize, are separable rights.

The Constitution bench of the Hon’ble Supreme Court held that