1[FORM-GST-RFD-01

[See rule 89(1)]

Application for Refund

(Applicable for casual or non-resident taxable person, tax deductor, tax collector, unregistered person and other registered taxable person)

![]()

Annexure-1 Statement -1 [rule 89(5)]

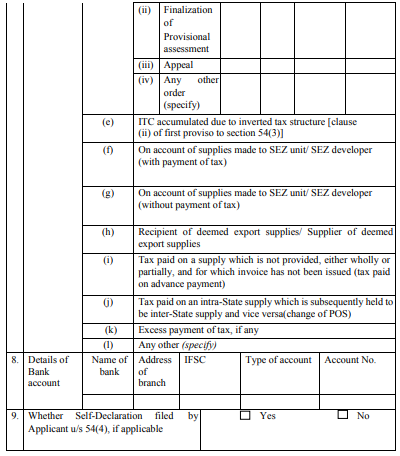

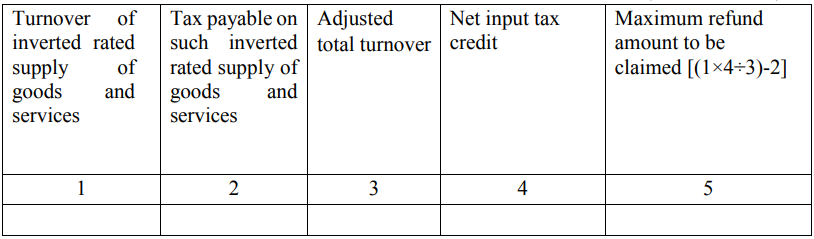

Refund Type: ITC accumulated due to inverted tax structure [clause (ii) of first proviso to section 54(3)]

(Amount in Rs.)

4[Statement 1A [rule 89(2)(h)]

Refund Type: ITC accumulated due to inverted tax structure

[clause (ii) of first proviso to section 54(3)]

5[Statement- 2 [rule 89(2) (c)]

Refund Type: Export of services with payment of tax 6[****]

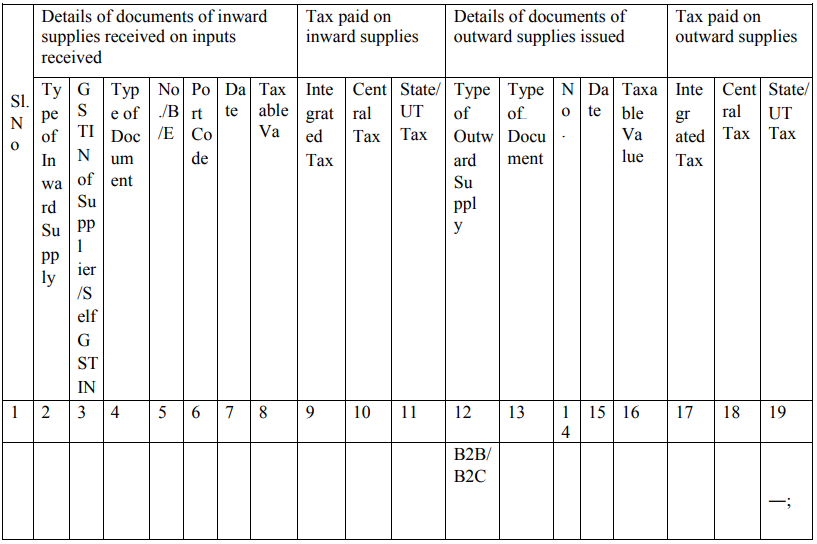

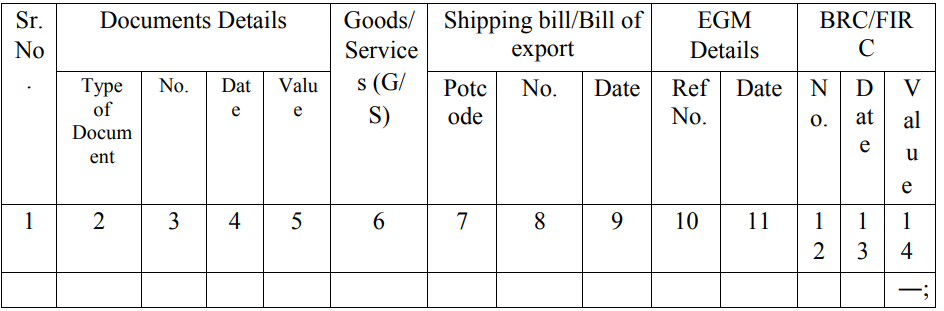

6[Statement- 3 [rule 89(2)(b) and 89(2)(c)]

Refund Type: Export without payment of tax (accumulated ITC)

Statement- 3A [rule 89(4)]

Refund Type: Export without payment of tax (accumulated ITC) – calculation of refund amount

(Amount in Rs.)

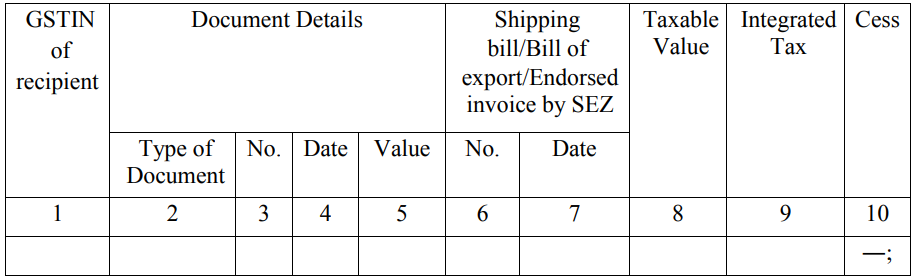

7[Statement-4 [rule 89(2) (d) and 89(2)(e)]

Refund Type: On account of supplies made to SEZ unit or SEZ Developer (on payment of tax)

8[Statement 4A

Refund of SEZ on account of supplies received from DTA-With payment of tax

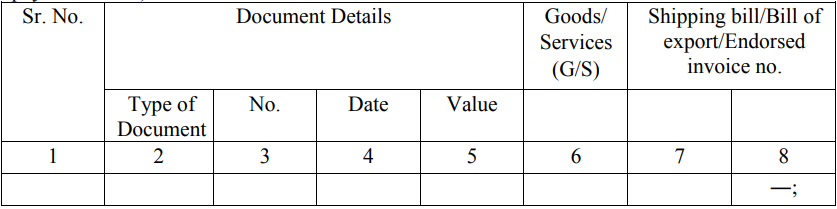

9[Statement-5 [rule 89(2)(d) and 89(2)(e)]

Refund Type: On account of supplies made to SEZ unit or SEZ Developer (without payment of tax)

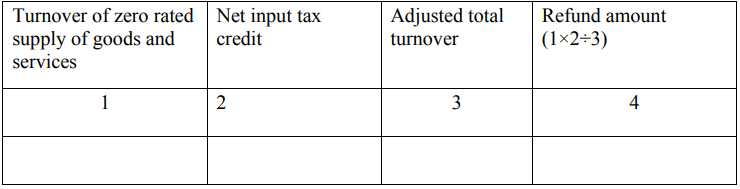

Statement-5A [rule 89(4)]

Refund Type: On account of supplies made to SEZ unit / SEZ developer without payment of tax (accumulated ITC) – calculation of refund amountuntn Rs.)

10[Statement 5B [rule 89(2) (g)]

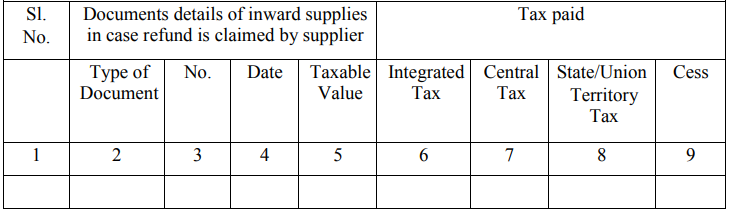

Refund Type: On account of deemed exports claimed by supplier

Statement 5B [rule 89(2)(g)]

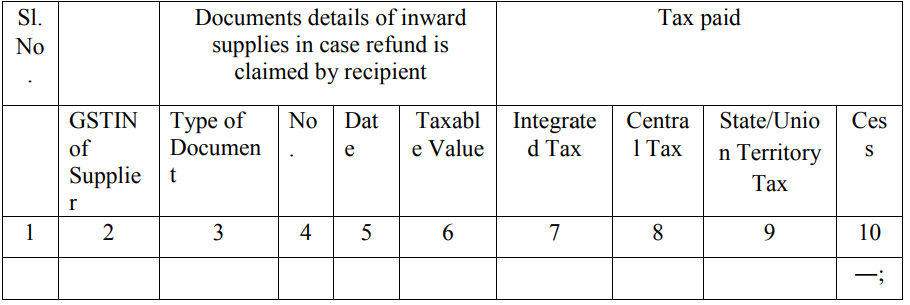

Refund Type: On account of deemed exports claimed by recipient

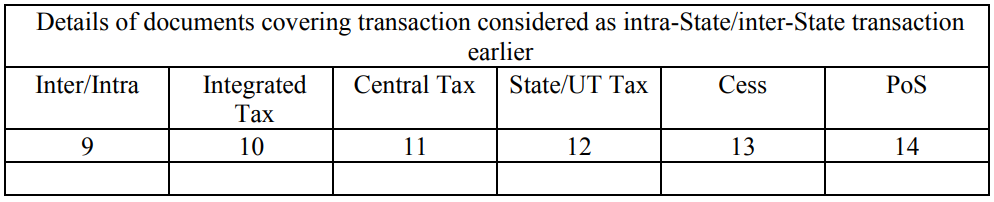

11[Statement-6 [rule 89(2) (j)]

Refund Type: On account of change in POS (inter-State to intra-State and vice versa)

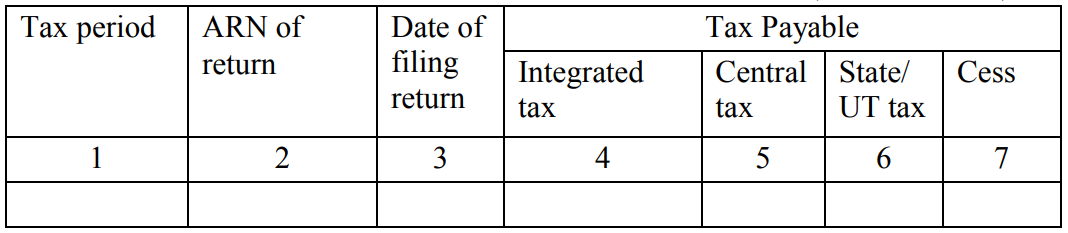

Statement-7 [rule 89(2) (k)]

Refund Type: Excess payment of tax, if any in case of last return filed.

(Amount in Rs.)

Annexure-2

Certificate [rule 89(2)(m)]

This is to certify that in respect of the refund amounting to Rs. <<>> ————- (in words) claimed by M/s————- (Applicant’s Name) GSTIN/ Temporary ID——- for the tax period <—->, the incidence of tax and interest, has not been passed on to any other person.

This certificate is based on the examination of the books of account and other relevant records and returns particulars maintained/furnished by the applicant.

Signature of the Charter Accountant/Cost Accountant:

Name:

Membership Number:

Place:

Date:

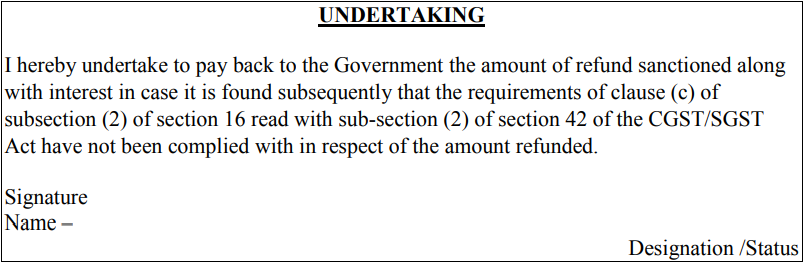

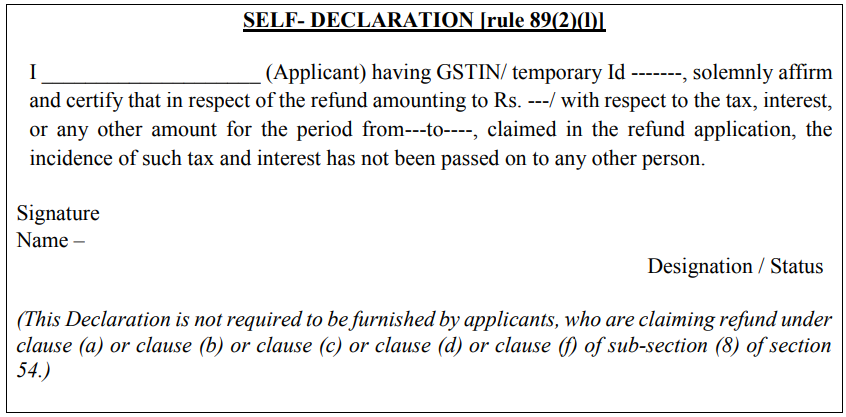

Note – This Certificate is not required to be furnished by the applicant, claiming refund under clause (a) or clause (b) or clause (c) or clause (d) or clause (f) of sub-section (8) of section 54 of the Act.

Instructions –

1. Terms used:

a. B to C: From registered person to unregistered person

b. EGM: Export General Manifest

c. GSTIN: Goods and Services Tax Identification Number

d. IGST: Integrated goods and services tax

e. ITC: Input tax credit

f. POS: Place of Supply (Respective State)

g. SEZ: Special Economic Zone

h. Temporary ID: Temporary Identification Number

i. UIN: Unique Identity Number

2. Refund of excess amount available in electronic cash ledger can also be claimed through return or by filing application.

3. Debit entry shall be made in electronic credit or cash ledger at the time of filing the application.

4. Acknowledgement in FORM GST RFD-02 will be issued if the application is found complete in all respects.

5. Claim of refund on export of goods with payment of IGST shall not be processed through this application.

6. Bank account details should be as per registration data. Any change in bank details shall first be amended in registration particulars before quoting in the application.

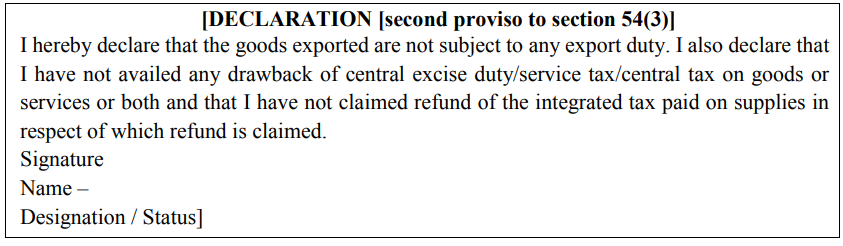

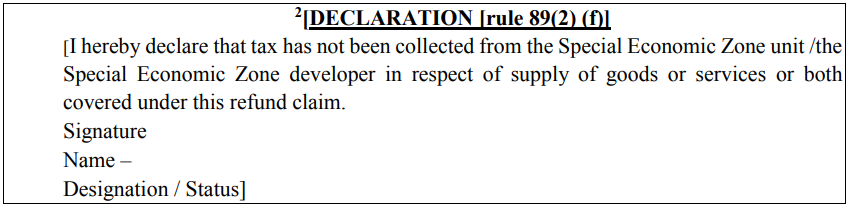

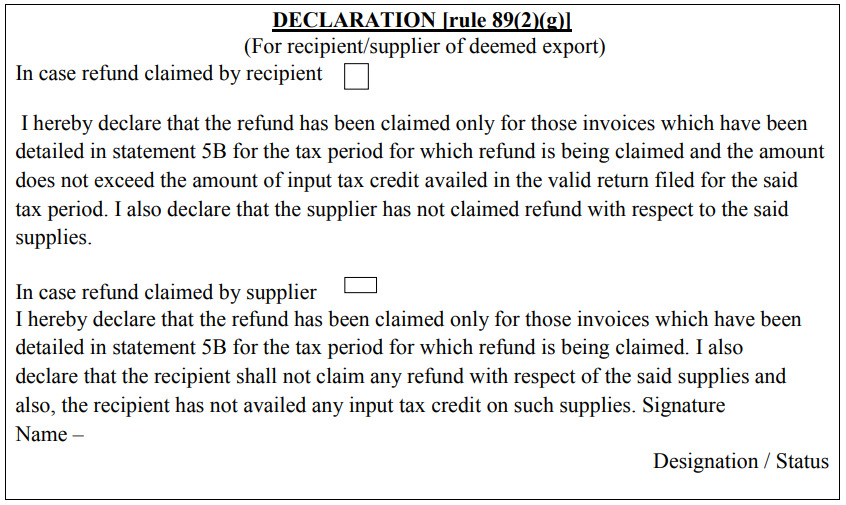

7. Declaration shall be filed in cases wherever required.

8. ‘Net input tax credit’ means input tax credit availed on inputs during the relevant period for the purpose of Statement-1 and will include ITC on input services also for the purpose of Statement-3A and 5A.

9. ‘Adjusted total turnover’ means the turnover in a State or a Union territory, as defined under clause (112) of section 2 excluding the value of exempt supplies other than zero-rated supplies, during the relevant period.

10. For the purpose of Statement-1, refund claim will be based on supplies reported in GSTR -1 and GSTR-2.

11. BRC or FIRC details will be mandatory where refund is claimed against export of services details of shipping bill and EGM will be mandatory to be provided in case of export of goods.

12. Where the invoice details are amended (including export), refund shall be allowed as per the calculation based on amended value.

13. Details of export made without payment of tax shall be reported in Statement-3.

14. Availability of refund to be claimed in case of supplies made to SEZ unit or SEZ developer without payment of tax shall be worked out in accordance with the formula prescribed in rule 89(4).

15. ‘ Turnover of zero rated supply of good and services’ shall have the same meaning as defined in rule89(4).

1. Substituted vide Notification No. 74/2018-CT dated 31.12.2018.

2. Substituted vide Notification No. 03/2019-CT dated 29.01.2019 w. e. f. 01.02.2019. Before substituted it was “I hereby declare that the Special Economic Zone unit/the Special Economic Zone developer has not availed of the input tax credit of the tax paid by the application covered under this refund claim.”

3. Substituted vide Notification No. 16/2020-CT dated 23.03.2020.

4. Substituted vide Notification no. 56/2019-CT dated 14.11.2019.

5. Omitted vide Notification No. 79/2020-CT dated 15.10.2020.

6. Substituted vide Notification No. 56/2019-CT dated 14.11.2019.

7. Substituted vide Notification no. 56/2019-CT dt. 14.11.2019.

8. Inserted vie Notification no. 56/2019-CT dt. 14.11.2019.

9. Substituted vide Notification no. 56/2019-CT dt. 14.07.2019.

10. Substituted vide Notification no. 33/2019-CT dt. 18.07.2019.

11. Substituted vide Notification no. 56/2019-CT dt. 14.11.2019.